/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Back in late 2024, custom chips for AI workloads were the talk of the town. People were coming to terms with the thesis that Nvidia’s (NVDA) state-of-the-art GPUs, no matter how good, weren’t ideal for the repeated high-intensity workloads that large language model training required. This caused stock prices for custom chip makers like Broadcom (AVGO) and Marvell Technology (MRVL) to skyrocket — until first-quarter guidance provided a reality check. Custom chipmakers weren’t able to translate that demand into sustainable revenue and stock prices crashed.

Fast forward to April 2026 and Marvell is trading at about the same share price as in December 2024. This recovery happened after MRVL stock dropped 60% from its December 2024 all-time high. While the current stock price may look familiar to those who were holding shares back then, the bull thesis has completely changed according to Barclays.

Marvell received an upgrade from Barclays analyst Thomas O’Malley on April 9. The analyst upgraded the stock from “Equal Weight” to “Overweight” and raised the firm’s price target from $105 to $150. This upgrade was based on strong growth expectations for the company’s optical business. Barclays expects this segment to grow by around 90% over the next two years.

So, the bull thesis has now changed to Marvell being a networking equipment company rather than a custom chip maker. The pace of AI development is such that it is hard to keep track of the incredible spending on AI infrastructure. Sooner or later, some component’s demand skyrockets. A few months ago, it was memory demand propelling stocks like Micron (MU), SanDisk (SNDK), and Western Digital (WDC) higher. Now it is Marvell, and while the firm is just a $100 billion company today, that could change sooner than some might think.

About Marvell Stock

Based in Wilmington, Delaware, Marvell Technology is a semiconductor company that offers data infrastructure solutions. The company operates across the United States, China, Vietnam, India, Taiwan, and other regions internationally. It delivers a range of products, including custom chips, ethernet controllers, processors, switches, and adapters. Marvell also provides storage and interconnect solutions.

Over the last year, Marvell stock has delivered an impressive performance, more than doubling in value. MRVL stock has surged more than 140% in the past 12 months while the S&P 500 ($SPX) has gained around 30%. That is considerable outperformance of the broader market.

The current valuation was good enough for Nvidia to take a stake in the company. MRVL stock currently trades at a forward price-to-earnings (P/E) of 37.7 times. While Nvidia CEO Jensen Huang doesn’t mind buying at that price, an average investor may not be able to afford to think like that, so here’s some perspective. Marvell is expected to grow its earnings by 40% in fiscal 2027 and 48% in fiscal 2028. These are the same kinds of growth rates seen by Tesla (TSLA) and Palantir (PLTR), yet those companies trade at forward P/E multiples of 241 times and 138 times, respectively. Marvell’s multiple looks cheap in comparison — and it could look even cheaper if optical segment growth materializes.

Data-Center Revenue Dominates Marvell's Earnings

Marvell reported its fourth-quarter fiscal 2026 earnings on March 5, 2026. Revenue for the quarter came in at $2.219 billion, representing a 22% year-over-year (YOY) increase. The data-center segment contributed to 74% of total revenue. Non-GAAP gross margin reached 59% with a non-GAAP operating margin of 35.7%. Non-GAAP EPS came in at $0.80. During the quarter, the company paid $51 million in dividends and spent $200 million on share buybacks.

Driven by strong demand from the data-center segment, Marvell also raised its revenue outlook on the earnings call. The company now expects fiscal 2027 revenue to reach $11 billion, higher than its earlier guidance of $10 billion in December and $9.5 billion in September. For the data-center segment, it expects revenue to grow by around 40% YOY, while the interconnect business is projected to grow by more than 50%. In the short term, Marvell forecasts first-quarter fiscal 2027 revenue of about $2.4 billion and EPS between $0.74 and $0.84.

What Are Analysts Saying About Marvell Stock?

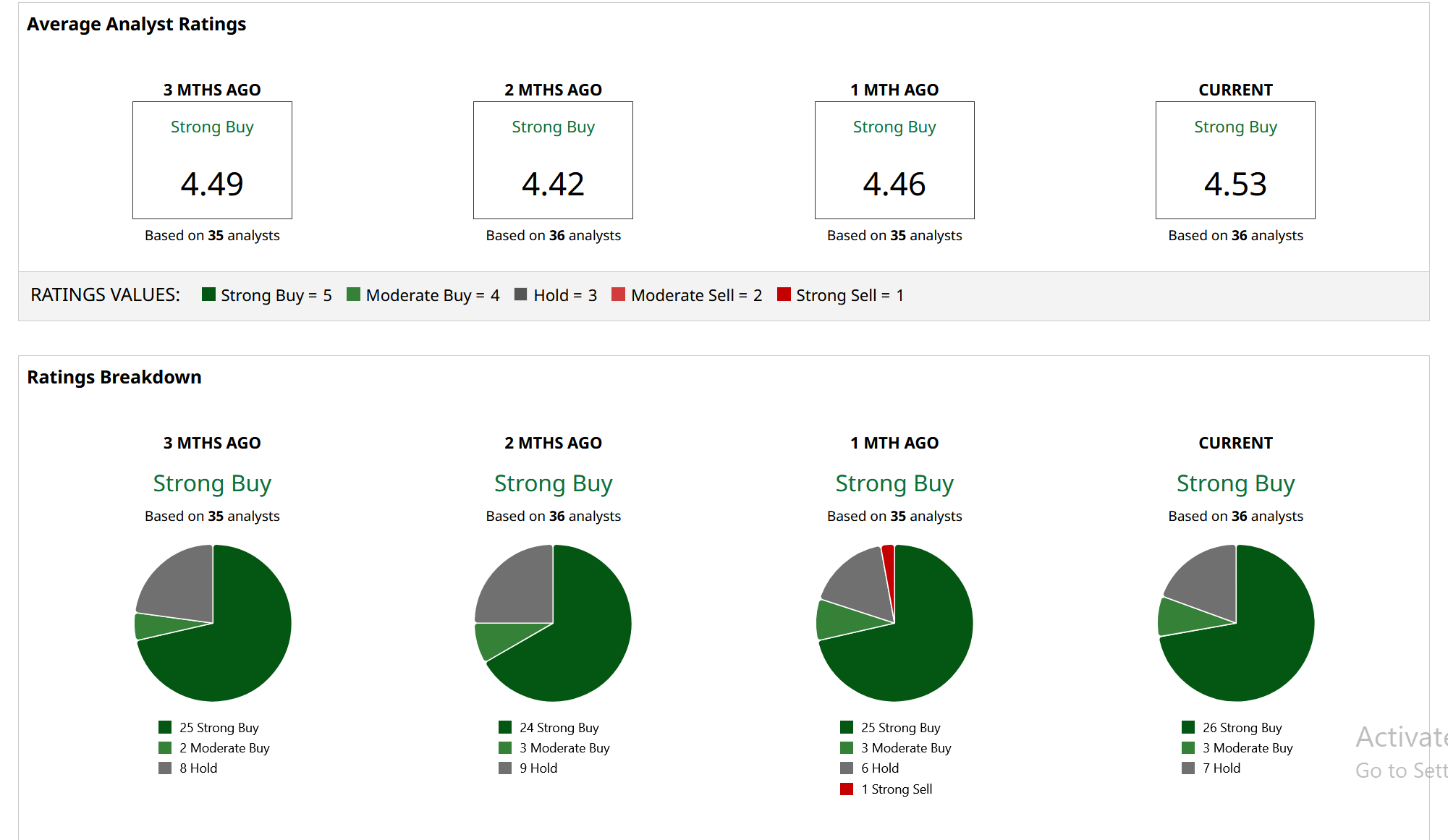

In addition to Barclays, Cantor Fitzgerald also increased its price target for MRVL stock from $100 to $120 while maintaining a “Neutral” rating. Based on 36 analysts covering the stock on Wall Street, Marvell enjoys a consensus “Strong Buy” rating.

The stock has a mean price target of $120.59, which shares have already surpassed. Based on the most bullish estimate, MRVL stock could go as high as $164 per share, implying potential upside of 29% from here.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)