/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

The “Magnificent 7” – NVIDIA Corporation (NVDA), Apple (AAPL), Amazon.com (AMZN), Tesla (TSLA), Meta Platforms (META), Alphabet (GOOGL) (GOOG), and Microsoft Corporation (MSFT) – have long been the market’s growth engine, powered by big bets on artificial intelligence (AI). But lately, the momentum has faltered.

Tech and AI names, which are typically driven by long-term growth and stable outlooks, have felt the pressure. Worries about an AI bubble, along with rising tensions between Iran, the U.S., and Israel, have pushed these stocks into correction territory, with many falling sharply from their highs.

Relief came with a conditional two-week ceasefire that reopened the Strait of Hormuz to shipping, calming markets, and sparking a rebound in tech. Investors, who had been sitting on the sidelines, quickly rotated back into these tech leaders.

Wedbush sees more than just a short-term bounce. The brokerage firm believes the geopolitical overhang had unfairly pushed the Magnificent 7 and broader tech space into oversold territory, setting the stage for a renewed “risk-on” environment. Analysts argue the recent sell-off in software and AI names is overdone, noting that enterprises are embracing AI by integrating it into existing platforms, not replacing them.

Amid this improving backdrop, AI chip giant NVIDIA deserves attention. Despite explosive growth, record results, and strong long-term AI chip demand, the stock has struggled for momentum in 2026 due to geopolitical tensions, inflation concerns, and AI adoption doubts. Still, fundamentals remain strong, backed by a deep backlog and growing ecosystem. With NVDA down by the mid-teen percentage from highs and valuations easing, this dip looks more like an opportunity to buy the top-rated stock now.

About NVIDIA Stock

Founded in 1993, the Santa Clara, California-based NVIDIA has become a pioneer in GPUs and AI-driven computing. From gaming to data centers and automotive tech, its innovations have reshaped industries, powering the AI revolution. Beyond technology, Nvidia champions energy-efficient designs and diversity initiatives, combining cutting-edge innovation with responsibility, cementing its role as a cornerstone of modern high-performance computing.

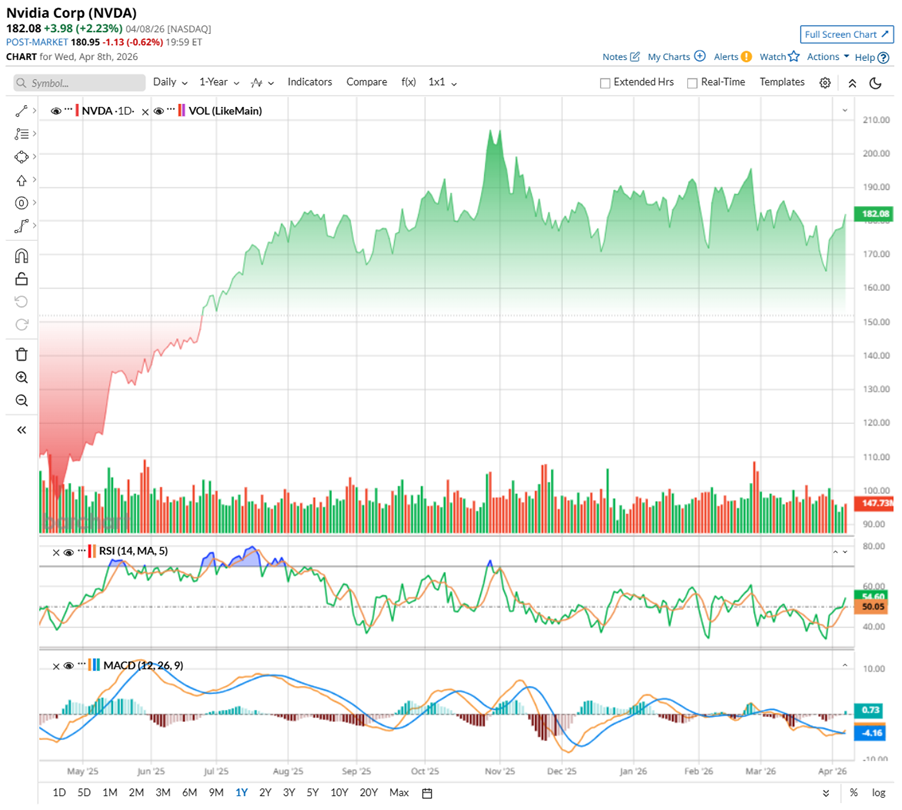

Valued at a market capitalization of $4.4 trillion, shares of the AI chip giant have seen a year of sharp rallies followed by brief pauses, moving in bursts rather than a straight line. NVDA stock has hit fresh highs 42 times in 52 weeks, climbing in waves before cooling off, almost like the market stopping to catch its breath.

After touching a peak of $212.19 in late October, it slipped about 13.8%, reminding investors that even the strongest runs need a reset. Still, the bigger picture holds firm, with NVDA up an impressive 59.1% over the past year.

But 2026 has been a bit more uneven. The stock is down slightly, weighed by growing questions around AI spending sustainability and rising competition from in-house chip efforts by tech giants. Even so, sentiment can shift quickly. Recent geopolitical easing has already sparked a rebound, showing how fast confidence can return.

Technically, the chart is starting to look steady again. The 14-day RSI has climbed back to 54.33, signaling improving momentum, while the MACD oscillator has turned positive with a bullish crossover, often an early sign that buying strength is returning.

Putting it all together, NVDA still feels like a stock in transition, not decline. Short-term noise may persist, but the longer-term trend still leans upward, making dips like these worth watching closely.

From a valuation angle, NVIDIA does not look as stretched as before. It is priced at roughly 23.24 times forward adjusted earnings, which sits below its past averages and even the sector median. If earnings keep rising on strong AI demand, this multiple could ease further, making the stock look more attractive over time. Its price-to-sales ratio, near 11.97 times, has also cooled compared to historical levels.

Also, the company has quietly built a track record of consistent dividends for over a decade. While the payout is not large, it reflects strong cash generation alongside its high-growth journey.

NVIDIA Surges Past Q4 Estimates

NVIDIA’s fiscal fourth-quarter 2026 report, released on Feb. 25, showed that the company is operating at full strength. Revenue surged 73.2% year-over-year (YOY) to $68.1 billion, while adjusted earnings climbed 82% annually to $1.62 per share, comfortably ahead of Wall Street’s expectations and reinforcing its leadership in the AI chip space.

The real momentum came from its data center segment. As companies race to build AI infrastructure, demand for NVIDIA’s chips continues to soar. Data center revenue jumped about 75% annually to $62.3 billion, highlighting its central role in powering this shift. Meanwhile, its gaming business also delivered solid growth, rising 47% YOY to $3.7 billion, supported by new product launches.

Financially, NVIDIA remains in a strong position. It closed the year with $62.6 billion in cash, cash equivalents, and marketable securities, alongside relatively low debt. The company generated $34.9 billion in free cash flow in the quarter, taking the full-year figure close to $96.6 billion.

This strength is translating into shareholder returns. NVIDIA distributed $41.1 billion through buybacks and dividends during fiscal 2026 and still has $58.5 billion authorized for future repurchases.

Looking ahead, management remains confident. At its annual GTC conference, NVIDIA projected up to $1 trillion in cumulative revenue from its Blackwell and Rubin AI platforms between 2025 and 2027. Later this year, it plans to roll out the powerful new Vera Rubin semiconductor platform, combining new GPUs, CPUs, and networking tech. The promise is simple – train AI with fewer chips and cut costs sharply. Lower costs could mean wider AI adoption, and in turn, even stronger demand for NVIDIA’s GPUs.

Additionally, the firm introduced new technologies aimed at advancing agentic AI. With first-quarter fiscal 2027 revenue expected to be around $78 billion, the growth story appears far from slowing.

Meanwhile, analysts project Q1 fiscal year 2027 EPS to increase 120.8% YOY to $1.70, with revenue anticipated to be around $78.7 billion. For fiscal year 2027, the bottom line is expected to surge 69.4% annually to $7.74 per share, before rising by another 31.8% YOY increase in fiscal 2028 to $10.20 per share.

What Do Analysts Expect for Nvidia Stock?

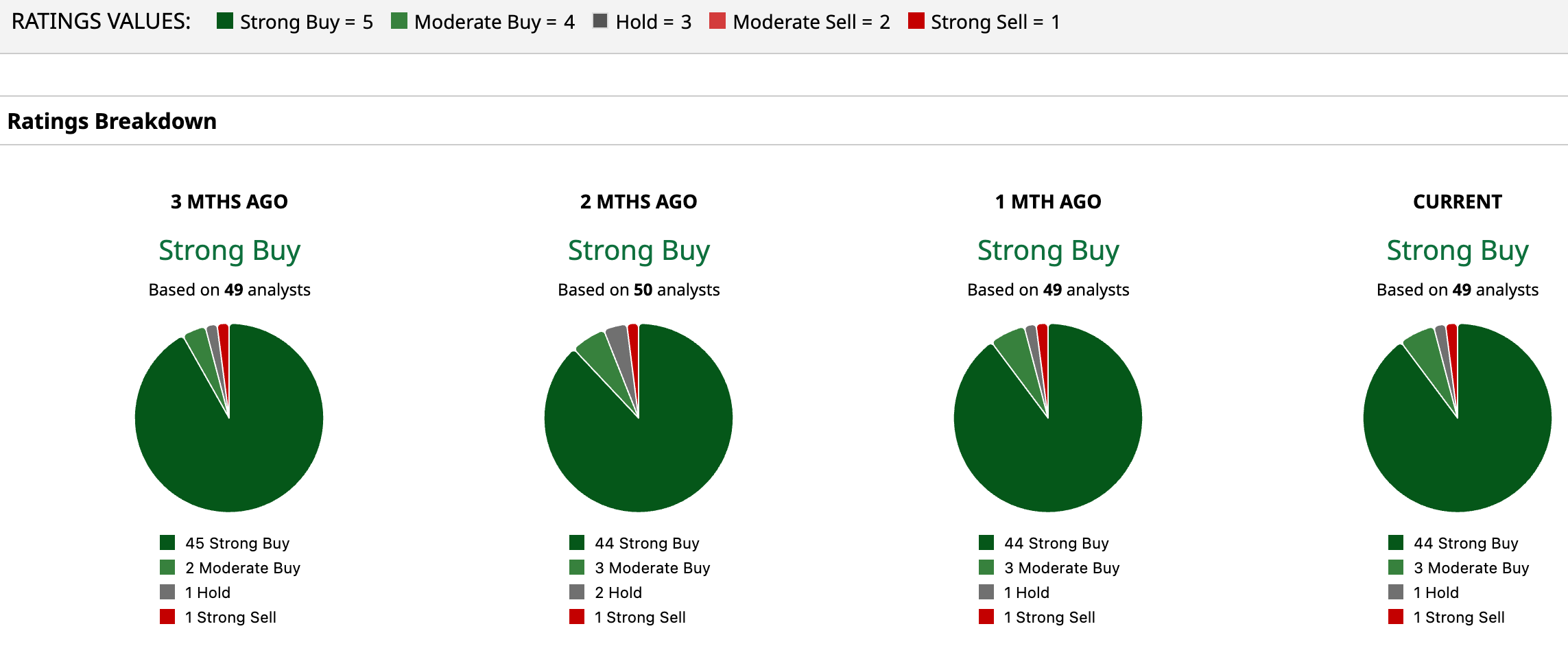

Overall, analysts are optimistic about NVDA’s growth potential, giving the stock a consensus rating of “Strong Buy.” Of the 49 analysts covering the stock, 44 advise a “Strong Buy,” while three suggest “Moderate Buy,” one advises a “Hold,” and only one suggests a “Strong Sell.”

The average analyst price target for NVDA is $268.80, indicating potential upside of 46.8%. The Street-high target price of $380 suggests that the stock could rally as much as 107.5% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)