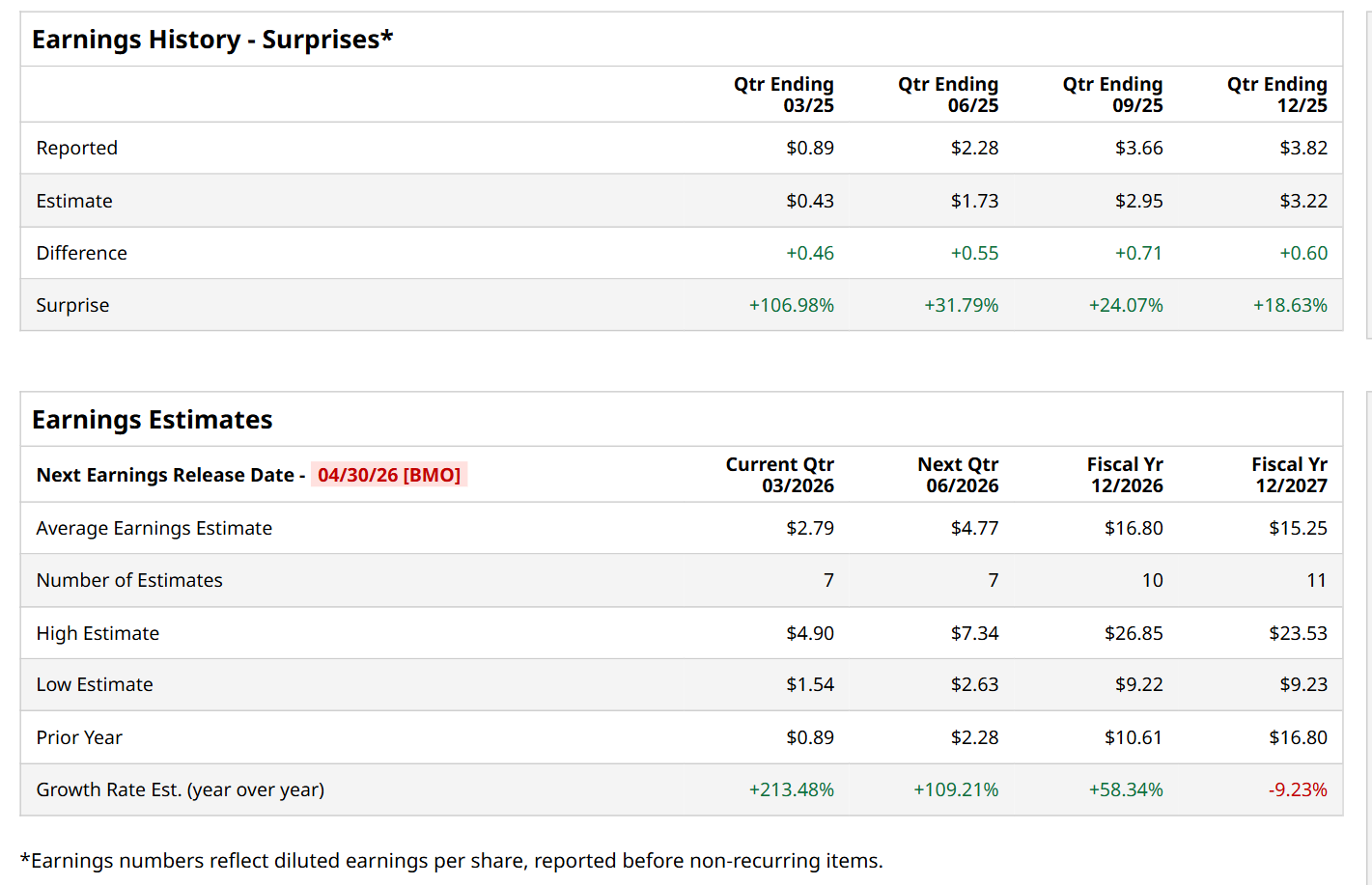

San Antonio, Texas-based Valero Energy Corporation (VLO) manufactures, markets, and sells petroleum-based and low-carbon liquid transportation fuels and petrochemical products. Valued at a market cap of $71.7 billion, the company is expected to announce its fiscal Q1 earnings for 2026 before the market opens on Thursday, Apr. 30.

Before this event, analysts expect this energy company to report a profit of $2.79 per share, up 213.5% from $0.89 per share in the year-ago quarter. The company has topped Wall Street’s bottom-line estimates in each of the last four quarters. Its earnings of $3.82 per share in the previous quarter outpaced the forecasted figure by 18.6%.

For the current fiscal year, ending in December, analysts expect VLO to report a profit of $16.80 per share, representing a 58.3% increase from $10.61 per share in fiscal 2025. However, its EPS is expected to decline 9.2% year-over-year to $15.25 in fiscal 2027.

VLO has rallied 127.8% over the past 52 weeks, significantly outperforming both the S&P 500 Index's ($SPX) 36.1% return and the State Street Energy Select Sector SPDR ETF’s (XLE) 51.9% uptick over the same time frame.

VLO stock’s performance over the past year has stood out, supported by strong refining margins and healthy cash generation, creating a solid earnings base. Valero has repeatedly exceeded expectations while returning capital through dividends and share buybacks, reinforcing investor confidence. Geopolitical tensions have further supported the narrative. Disruptions in the Middle East have tightened refined fuel supply and widened crack spreads, benefiting refiners like Valero as diesel and gasoline prices rise faster than crude. Additionally, Valero’s ability to process heavier crude grades, including discounted barrels from Venezuela, provides a competitive advantage.

Together, resilient margins, geopolitical tailwinds, and consistent shareholder returns have helped keep VLO ahead of the broader market.

Wall Street analysts are moderately optimistic about VLO’s stock, with a "Moderate Buy" rating overall. Among 21 analysts covering the stock, 11 recommend "Strong Buy," one indicates a "Moderate Buy," and nine suggest "Hold." While the company is trading above its mean price target of $235.44, its Street-high price target of $292 suggests a 21.8% potential upside from the current levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)