/Microsoft%20logo%20on%20building%20by%20trazika%20via%20Pixabay.jpg)

With a loss of over 23% as of April 7 closing prices, Microsoft is the worst-performing Magnificent 7 stock this year. The stock is also underperforming its average S&P 500 Index ($SPX) peer this year, something it also did in the previous two years. Notably, while Microsoft was seen as a defensive play given its relatively stable business compared to other Big Tech companies, it failed to live up to that perception this year and has underperformed amid the war in Iran.

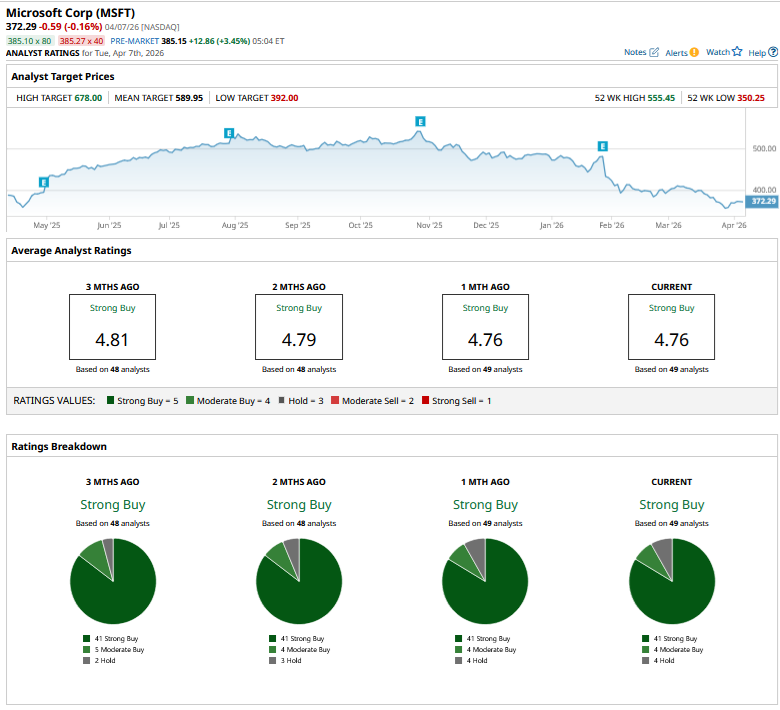

Goldman Sachs Predicts Massive Upside in MSFT Stock

Meanwhile, the markets have been bearish on MSFT stock, but the sell-side analyst community has largely maintained its bullish bias. Most recently, Goldman Sachs reiterated its “Buy” rating on MSFT while reiterating its $600 target price, which is slightly ahead of the stock’s mean target price and represents a potential upside of 61% over the current price levels.

Benchmark analyst Yi Fu Lee also initiated coverage on Microsoft earlier this month with a “Buy” rating and relatively somber target price of $450. The bottom line, however, remains that after the massive crash in MSFT—it is down nearly 33% from its 52-week highs—analysts see significant upside. Incidentally, the only other time MSFT stock dipped by more than 30% from its peak was during the 2022 tech crash. The rest, as we know, is history, and tech stocks, including MSFT, rebounded the next year, with the rally continuing into the next two years.

That said, every crash is different. 2022 was more of a broader-market meltdown amid fears over a U.S. recession and stretched valuations. While there is a market crash angle this time around, many of the concerns are specific to Microsoft.

Why Has Microsoft Stock Underperformed?

Microsoft's stock has underperformed for several reasons. Firstly, contrary to its previous projection, the company has increased its capex to build artificial intelligence (AI) infrastructure.

Also, while other major cloud players are witnessing an acceleration in growth, Azure saw a deceleration in the most recent quarter. The segment reported a 39% growth in the fiscal Q2 2026 revenues, which was below the 40% that it reported in the fiscal first quarter and slightly below Street estimates. The guidance for the March quarter implied a further tapering of growth. While the company has argued that it is capacity-constrained in data center infrastructure and has been balancing in-house needs with external customers, that assertion failed to cut ice with markets.

On a similar note, OpenAI accounts for 45% of Microsoft’s cloud remaining performance obligations (RPOs), which is a major concentration risk for the company, particularly given how the ChatGPT parent’s competitors have been gaining ground, raising concerns over OpenAI’s ability to deliver on its massive commitments.

While OpenAI has listed its reliance on Microsoft as a “risk,” dependence on the Sam Altman-led AI startup is a risk for Microsoft, too. If anything, Microsoft is more dependent on OpenAI, as the latter has been able to arrange financing from other players and earlier this year secured $110 billion in funding in a round involving Amazon (AMZN), Nvidia (NVDA), and SoftBank (SFTBY). It's no secret that relations between OpenAI and Microsoft are not the best in the world, and the two companies are also competing on some fronts. For instance, while Microsoft is developing its own frontier AI models, OpenAI launched its AI-powered search browser ChatGPT Atlas, which would compete with Microsoft Bing.

There are also fears that AI tools can disrupt Microsoft’s enterprise tool business, and over the long term, we might have better open-source rivals to the Office franchise.

Should You Buy MSFT Stock?

Meanwhile, Microsoft’s valuation multiples have contracted, and the stock now trades at a forward price-to-earnings (P/E) multiple of 22.7x, significantly below the average multiples over the last decade as markets have repriced MSFT amid the software sell-off. Also, the company’s free cash flows are taking a beating amid the AI buildout, while it hasn't seen a commensurate rise in growth.

All said, and as I noted in my previous article, the selloff in MSFT stock has gone a bit too far, and it looks like a compelling buy given the tepid valuations. While there are genuine concerns, and MSFT's valuations might not rise to the kind of levels we saw at the peak anytime soon, at these levels, it seems to offer value for long-term investors.

On the date of publication, Mohit Oberoi had a position in: MSFT, AMZN, NVDA. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)