/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

For long-term investors looking for increased exposure to Big Tech, Microsoft (MSFT) stock is worth buying, as the company has already become a huge winner from the AI boom, and there is a good chance that its upcoming AI tools will meaningfully boost its financial results in the medium-to-long term. Moreover, after MSFT stock tumbled in the first quarter, its current valuation is quite attractive.

Finally, the Street's fears about MSFT's capital expenditures and investors' worries about AI undermining the firm's software business are tremendously overdone.

About Microsoft Stock

One of the world's largest tech names, with a market capitalization of $2.6 trillion, MSFT specializes in providing cloud-computing tools, AI infrastructure, the Windows operating system, and the Microsoft 365 suite of productivity software.

In the company's fiscal second quarter that ended in December, its revenue climbed 17% versus the same period a year earlier to $81.3 billion, while its operating income advanced 21% year-over-year (YoY) to $38.3 billion.

The forward price-earnings ratio of MSFT stock is 21.68 times.

MSFT Is Already an AI Winner, and Its New AI Tools Are Very Promising

As one of the leading vendors of AI infrastructure, the tech giant has already gotten a tremendous boost from the proliferation of AI. Specifically, the revenue of its Intelligent Cloud unit, which produces and markets AI infrastructure, jumped 29% YoY to $32.9 billion during the company's quarter that ended in December. That's obviously a fantastic level of growth for a cloud unit that's rather mature at this point.

And much more impressively, MSFT's “remaining performance obligations,” representing signed contracts that have not yet generated revenue, soared 110% YoY to a gigantic total of $625 billion. The fact that OpenAI represents 45% of the latter total has been portrayed by some as a weakness, but, since ChatGPT looks poised to remain a massive player in AI for the foreseeable future, MSFT's alliance with the start-up looks like a huge strength.

Given MSFT's huge backlog and the continued, rapid growth of AI, Microsoft's revenue from selling AI infrastructure is likely to continue to soar for many years, if not decades, to come.

But the company's AI-powered assistant, CoPilot, has been largely unsuccessful, as only “3.3 percent of Microsoft 365 and Office 365 customers are actually paying for it,” CPO Magazine recently reported. But CoPilot's “deep research agent,” Researcher, will utilize multiple models, “including Anthropic and OpenAI,” the company announced on March 30.

Microsoft reported that its "evaluations show that this architecture exceeds traditional single model approaches and delivers best in class deep research quality." A system within Researcher, called Critique, summarizes the findings of each model and uses one model to evaluate the findings of its “peer.” A second tool, known as Council, compares the responses of Anthropic and OpenAI, enabling users to gain insights on discrepancies that need to be researched further.

Logically, using multiple models should produce better results than utilizing a single one. (It reminds me of the famous, age-old expression, “Two brains are better than one.”) And Microsoft is reporting that the system does indeed deliver higher-quality results than all the single, popular tools, based on a widely used benchmark. While I will wait for independent reviewers to assess the system before definitely determining the validity of the claim, I believe that there is a good chance that the demand for CoPilot will surge in the medium-to-long-term following Researcher's upgrade.

In addition to the logic of Microsoft's new approach and the company's upbeat assessment of Researcher following the upgrade, CEO Satya Nadella's strong track record also makes me bullish on CoPilot's outlook. After all, under Nadella, Microsoft became a big winner of both the Cloud Revolution and the AI Revolution. Consequently, I believe that he can also make CoPilot a big winner.

Overdone Fears

Some believe that AI agents will eventually replace Microsoft's software. But Alphabet (GOOG) (GOOGL) has offered tools that are similar to Microsoft's products for many years, and in some cases GOOG has provided them for free. And yet MSFT, by occasionally adding new features and capitalizing on the ubiquity of its Windows operating system on computers, has managed to keep significantly increasing its revenue from software. I expect the latter trend to continue in the face of competition from AI agents.

Further, some are worried about the high capital expenditures that Microsoft is using to expand the amount of AI infrastructure that it can offer. The problem, it seems, is that the Street is not used to tech companies having to spend a great deal on capex, since they typically outsource the production of their offerings to Asian companies.

But history shows that, amid successful technological revolutions, high spending can eventually produce huge stock gains. Consider, for example, that, by 1919, General Motors (GM), amid the Auto Revolution, had built or acquired enough factories to produce 1 million vehicles. That feat undoubtedly required huge investments. And yet between August 1921 and the end of 1928, GM stock had soared from $9.63 to nearly $98. With most businesses and consumers embracing AI, much as society was beginning to embrace autos in the early 20th century, investments in building infrastructure for the technology look poised to pay off handsomely in the longer term.

Valuation and the Bottom Line on MSFT Stock

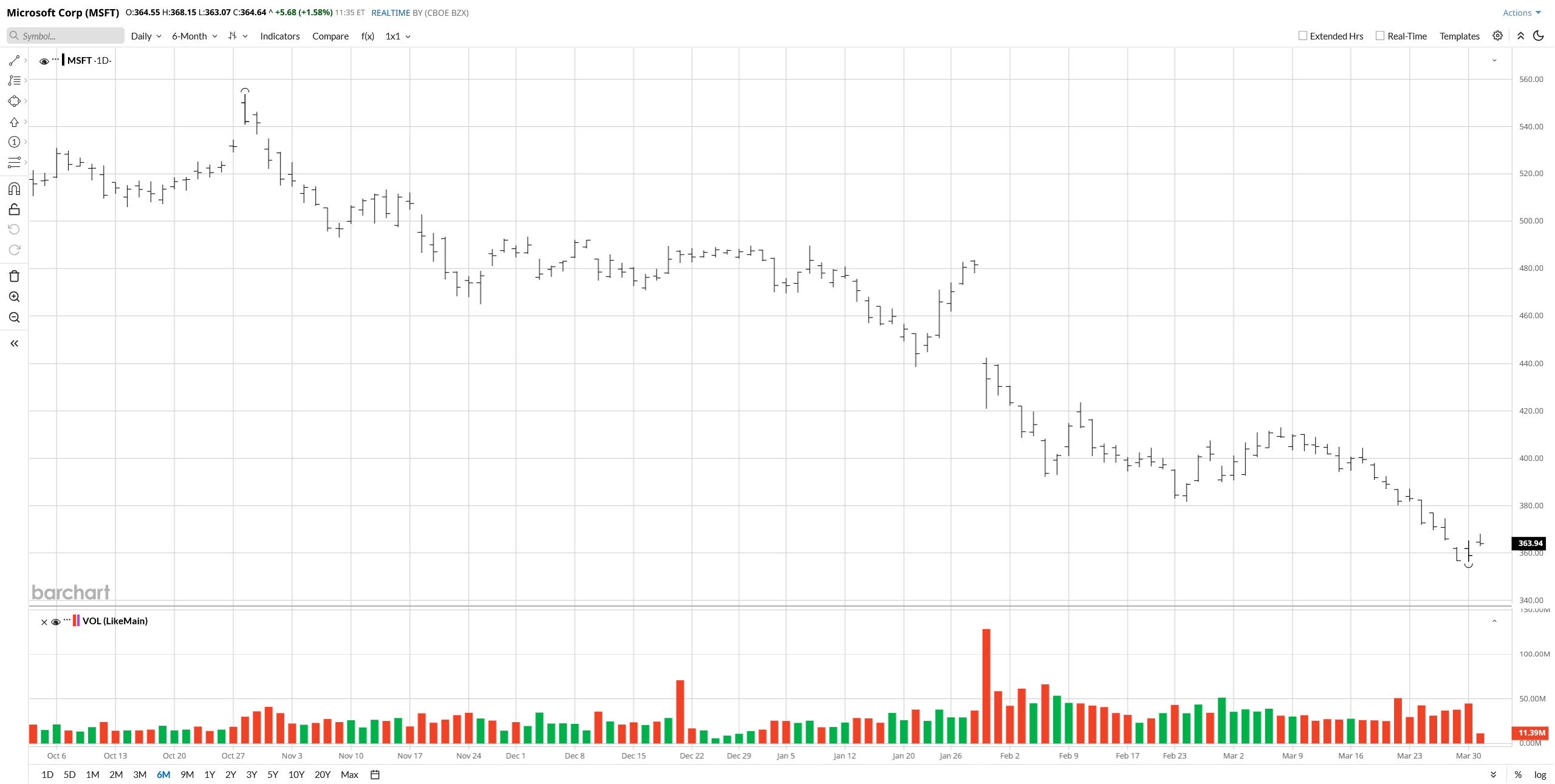

After MSFT stock had sunk 25% in the first quarter as of March 27, the shares' price-earnings ratio had reached its lowest level since June 2016.

Given the company's success in the AI era and its tremendous opportunities, along with the vastly overdone fears that triggered its declines, this weakness has created an excellent buying opportunity for long-term investors looking for increased exposure to Big Tech.

On the date of publication, Larry Ramer did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)