President Donald Trump recently gave Micron Technology (MU) a rare public endorsement, calling it one of the "hottest" stocks in the U.S. following a White House meeting with CEO Sanjay Mehrotra. For investors, that kind of presidential praise is difficult to ignore.

But here's the thing: MU stock has been falling even as it reported stellar numbers in the recent quarter.

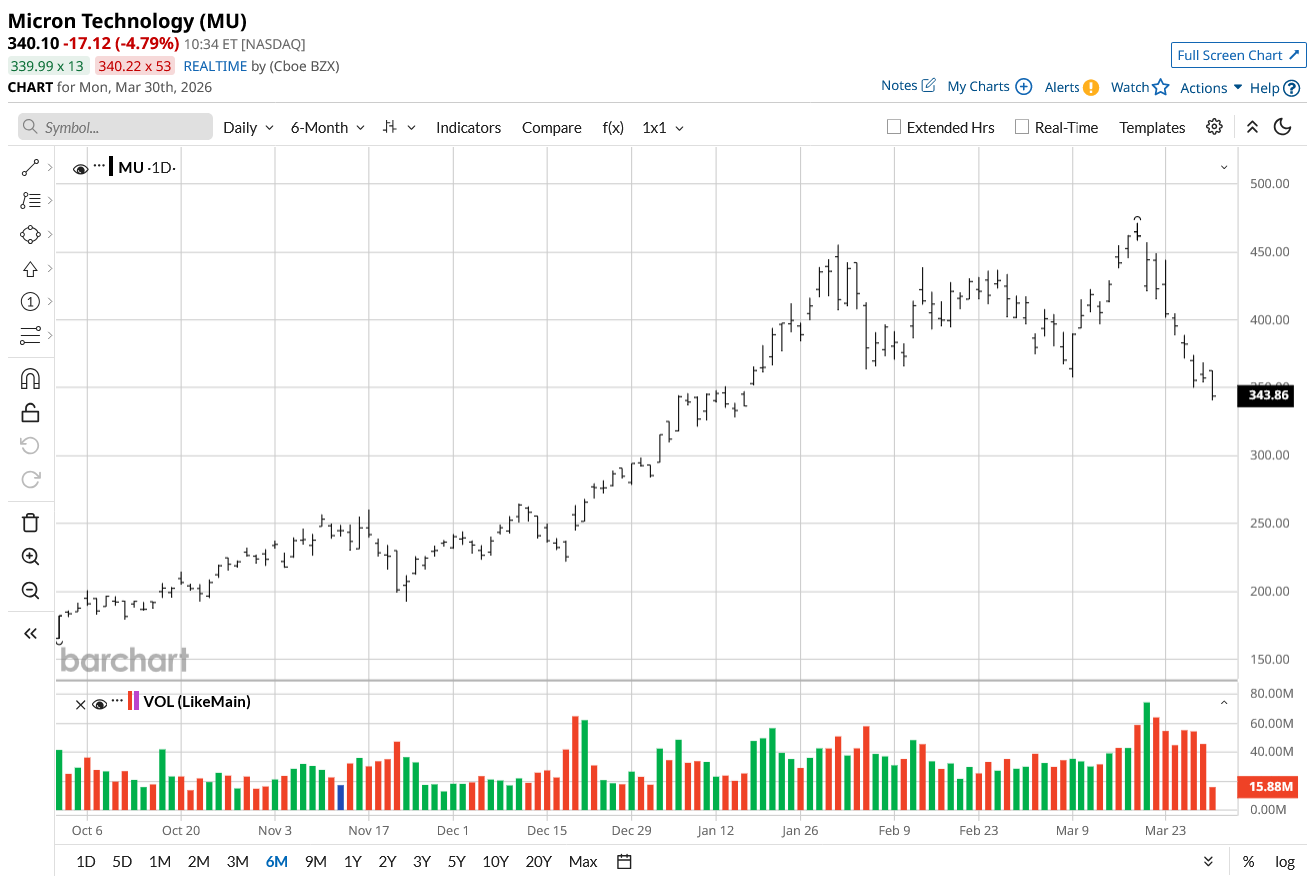

Despite record-breaking earnings and glowing analyst upgrades, MU stock is down 27% from 52-week highs. That raises a fair question: is this a buying opportunity, or is something more serious going on?

Micron’s Solid Q2 Numbers

Micron makes the memory chips that power artificial intelligence systems. In fiscal Q2 of 2026, Micron reported revenue of $23.86 billion, up from $8.05 billion in the year-ago period. It also estimates gross margins to exceed 80% in fiscal Q3.

Micron is benefiting from a tight memory supply environment. On Micron's post-earnings analyst call, Chief Business Officer Sumit Sadana put it plainly: "Our supply is nowhere close to being able to meet the demand that we see for the foreseeable future."

The supply crunch spans both DRAM (used in AI servers and PCs) and NAND (used in storage). Sadana noted that Micron is the first company globally to have a next-generation Gen6 SSD on the market, one that works especially well with Nvidia (NVDA) systems, and that demand for it far exceeds what the company can ship.

Why Is MU Stock Falling?

A few things are working against the semiconductor giant.

- First, valuation concerns. Micron has surged more than 280% over the past year and is among the few tech stocks to report year-to-date (YTD) gains. Elevated fiscal 2027 capital expenditure plans and peak gross margin concerns likely triggered some selling after the stock's strong run into the report.

- Second, big spending is raising eyebrows. Micron raised its fiscal 2026 capital expenditure outlook to over $25 billion, up from the $20 billion it had guided previously, according to Chief Financial Officer Mark Murphy. Some of that increase reflects the acquisition of a new fab in Taiwan and the expansion of U.S. construction. Investors worry that heavy spending could compress future returns.

- Third, competitive threats are creeping in. Reports of a potential memory-compression breakthrough from Google (GOOG) (GOOGL) rattled the market, raising questions about whether AI companies could eventually need less memory per system.

What Is the Micron Stock Price Target?

The bull case is straightforward. Memory demand is growing faster than supply can keep up with. New demand drivers, from AI agents and longer-context AI models to robotics, are only adding fuel.

Micron's cleanroom expansion won't meaningfully boost capacity until the second half of 2028, per Manish Bhatia, Micron's EVP of Global Operations. That means tight conditions could persist for years.

The bear case? Micron's stock has priced in a lot of good news. Any slowdown in AI spending or a surprise from a competitor like SK Hynix or Samsung could quickly shake confidence.

For long-term investors, the pullback may look like an entry point. For those already sitting on big gains, the near-term picture is murkier.

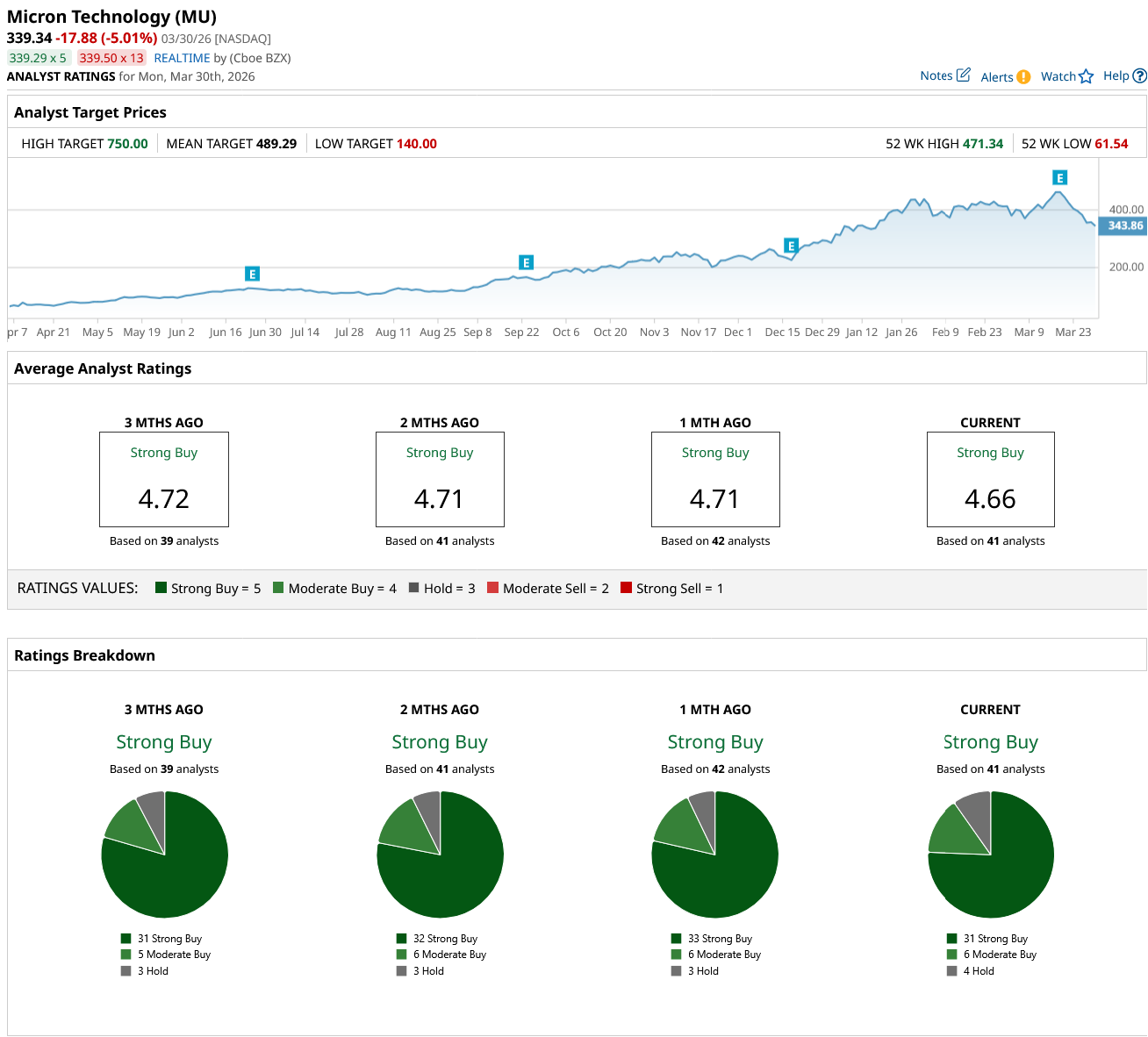

Out of the 41 analysts covering MU stock, 31 recommend “Strong Buy,” six recommend “Moderate Buy,” and four recommend “Hold.” The average Micron stock price target is $489.29, above the current price of $339.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)