/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

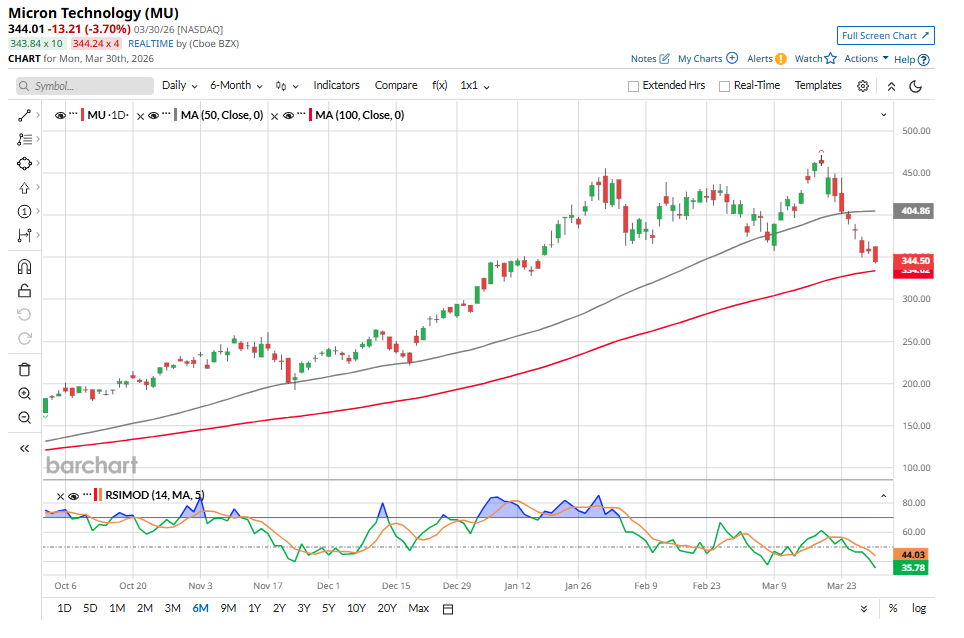

After a powerful rally over the past year, Micron (MU) stock has recently lost some momentum, declining 32% from its 52-week high of $471.34. The pullback reflects profit-taking by investors following the strong run-up, as well as emerging concerns about potential shifts in demand in the memory market.

The recent uncertainty stems from developments in the artificial intelligence (AI) ecosystem. Alphabet (GOOGL) recently introduced TurboQuant, which lowers the memory requirements of AI models. Since memory and storage capacity are critical building blocks of AI infrastructure, innovations that improve efficiency can raise questions about whether demand for memory hardware might eventually grow more slowly than previously expected. For companies like Micron, which supply memory components used in data centers and AI systems, such developments naturally put pressure on the stock price.

Nonetheless, the broader outlook for MU stock remains constructive. Micron remains a critical supplier of memory and storage technologies for data-intensive applications, particularly those related to AI and high-performance computing. As AI models grow more sophisticated and computational workloads expand, demand for advanced memory solutions is still expected to remain strong over the long term.

Looking ahead, Micron appears well-positioned to benefit from these trends in 2026 and beyond. At the same time, the recent decline in Micron’s share price has significantly reduced its valuation. With MU stock trading well below its recent peak, the pullback in Micron has made its valuation too cheap to ignore.

AI Demand to Power Micron’s Earnings

Rising demand for AI infrastructure and ongoing supply constraints across the memory industry are expected to continue supporting Micron’s earnings growth in the coming quarters. The company delivered exceptionally strong results in the fiscal second quarter, reflecting both improving pricing dynamics and robust demand across its core memory segments.

Micron reported total fiscal Q2 revenue of $23.9 billion, a 75% sequential increase and a 196% year-over-year (YOY) rise. The biggest contributor was Micron’s DRAM segment, which delivered a record $18.8 billion in revenue and accounted for roughly 79% of the company’s total sales. Revenue in the segment rose 74% compared with the previous quarter and 207% YOY. While shipment volumes increased at a modest pace, pricing provided the primary lift. Average selling prices climbed in the mid-60% range, reflecting ongoing supply constraints and a shift toward higher-value memory products used in advanced computing systems.

Micron’s NAND flash business also posted record performance. Revenue from the segment reached $5 billion, representing an 82% sequential increase and a 169% rise from a year earlier. Similar to DRAM, shipments grew slightly while pricing rose sharply.

Micron’s profitability improved substantially alongside the revenue growth. Consolidated gross margin for the quarter reached 75%, an increase of 18 percentage points from the prior quarter. The margin expansion was driven primarily by higher pricing, supported by a favorable product mix and continued cost efficiencies.

Looking ahead, the current momentum is expected to continue as demand for AI infrastructure drives further growth in memory consumption. AI workloads are expanding the total addressable market for both DRAM and NAND in data centers. Traditional server demand also remains strong, supported by workloads from emerging agentic AI applications and a broad cycle of server upgrades.

Beyond the data-center market, Micron is also benefiting from improving pricing trends across automotive, industrial, and embedded segments. At the same time, the emergence of on-device AI capabilities is expected to increase memory requirements in personal computers and smartphones, creating an additional long-term growth driver for the company.

Reflecting these favorable industry conditions, analysts expect earnings to increase sharply in the coming years. Consensus estimates project EPS of $57.70 for fiscal 2026, representing YOY growth of more than 651%. This is expected to be followed by additional EPS expansion of more than 67% in fiscal 2027 to $96.55.

Micron Stock Is Too Cheap to Ignore

Micron’s recent pullback has created an attractive buying opportunity for investors. Despite the decline, Micron’s underlying growth outlook remains strong, making the current valuation compelling.

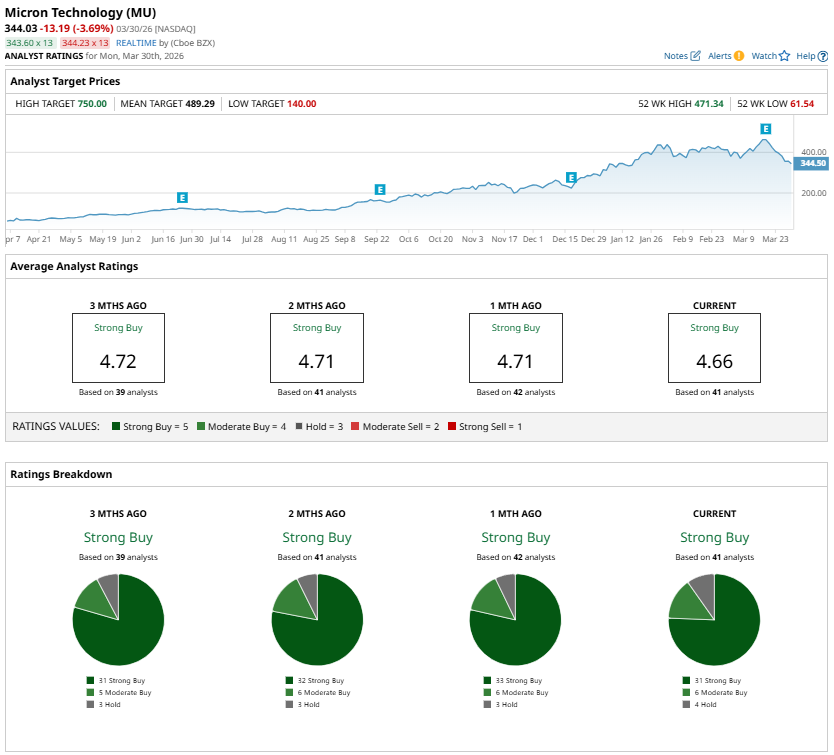

At present, Micron is trading at a forward price-to-earnings (P/E) ratio of approximately 6.2 times. This multiple appears notably low relative to the company’s earnings growth prospects, suggesting MU stock is undervalued.

Wall Street sentiment toward Micron remains positive. Analysts maintain a “Strong Buy” consensus rating for the stock.

Taken together, Micron's solid growth outlook, low forward earnings multiple, and favorable analyst sentiment suggest that MU stock is too cheap to ignore.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)