/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

After a mixed tech market recently, Microsoft (MSFT) is back in the spotlight. Other “Magnificent 7” stocks have pulled back in 2026 as investors rotate into value. But Microsoft’s AI story remains a beacon. At the start of April 2026, Benchmark analyst Yi Fu Lee kicked off coverage on MSFT with a “Buy” rating and a $450 price target.

He calls Microsoft “a central player in AI,” with unmatched data advantages from its Office, Teams, LinkedIn, and Azure platforms. Benchmark views the stock’s recent pullback as a chance to buy. Microsoft still sits at the center of the AI trade, and analysts think that makes recent weakness more of an opportunity than a warning sign.

The AI Moat Nobody Else Can Replicate

Everyone talks about AI models. But models without data are engines without fuel. Microsoft sits on a treasure trove of 1 billion Windows users, 300 million Office seats, LinkedIn’s professional graph, GitHub’s developer ecosystem, and Azure’s enterprise footprint. No competitor, not Amazon (AMZN), not Alphabet (GOOG) (GOOGL), nor OpenAI itself, can match this distribution. CEO Satya Nadella put it bluntly last quarter: “We are only at the beginning phases of AI diffusion, and already Microsoft has built an AI business larger than some of our biggest franchises.”

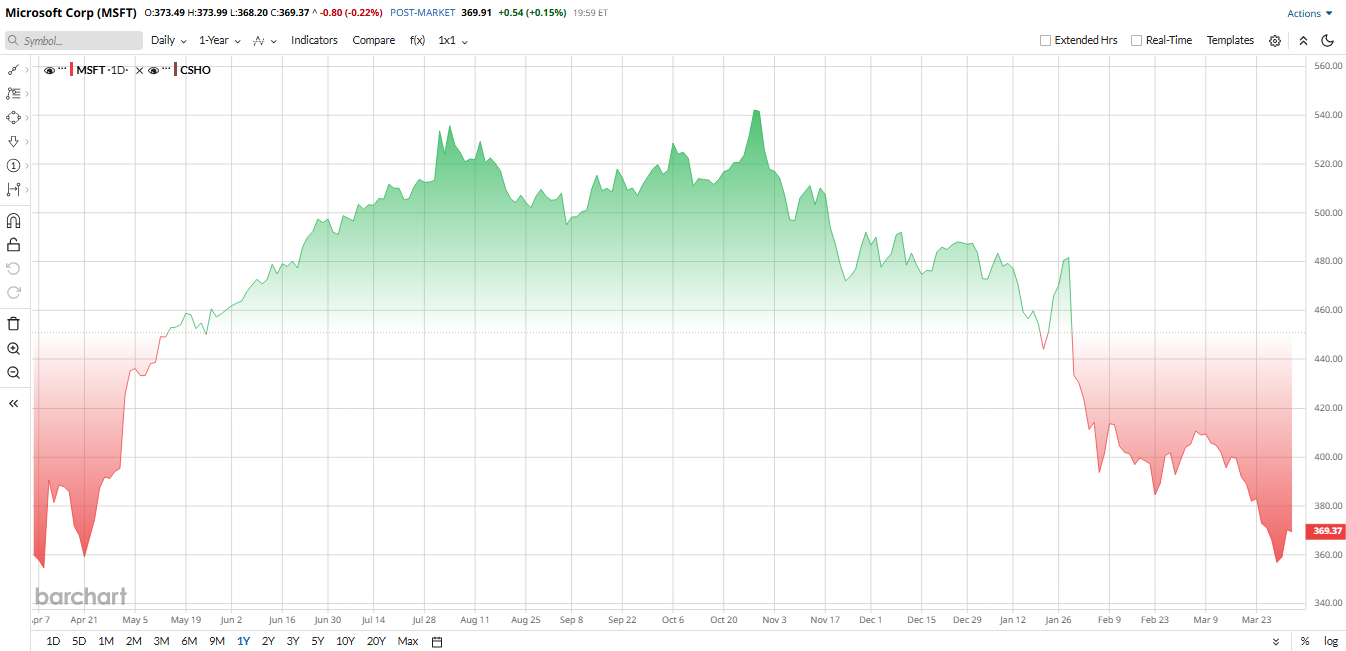

MSFT’s stock performance has been relatively choppy. It peaked above $550 in late 2025 but is around $370 now, which translates to about a 23% loss in 2026 year-to-date (YTD). Moreover, Analysts note it fell below its 50-day moving average after the profit-taking, though it’s still above long-term support.

That said, Microsoft’s forward P/E of 22× is now one of the lowest among big tech; many of its peers trade above 40×, making it look cheaper by comparison. The consensus 2026 growth outlook also justifies this valuation: Wall Street expects 15% to 18% revenue growth through FY26, Azure 25% to 30%, and Office steady.

Benchmarks Bullish Call

Benchmark’s latest note has stirred interest. Yi Fu Lee sees Microsoft’s dip as a buying opportunity. He flags Microsoft’s massive data ecosystem, e.g., 1 billion Windows users, 300 million Office seats, LinkedIn, and GitHub, as a moat. The $450 target implies about 25% upside from today’s price. More importantly, investors seem to have taken a second look at Microsoft’s pipeline. For example, Bank of America said Microsoft’s “dual advantage” in owning both AI infrastructure and end-user apps should sustain 15% to 17% growth.

Short-term, the bull case is that fears over endless capex and rivals are overdone. Microsoft spent heavily on data centers, with capex of $30 billion in Q2, and faces short-term margin pressure. But analysts like BoA and Goldman argue this is needed to cash in on a huge $625 billion cloud backlog.

If the AI economy stays robust, MSFT could easily break higher. For now, the new coverage is giving fans more confidence.

Microsoft Beats Q2 Earnings Estimate

Microsoft’s most recent quarter, Q2, was very strong. Total revenue was $81.3 billion, up 17% year-over-year (YoY), plus it topped analyst estimates by more than $1 billion

Profitability was excellent. Net income landed at $38.5 billion, up 60%, giving EPS $5.16. Adjusted EPS, which excludes a massive one-time $7.6 billion OpenAI gain, was $4.14, up 24%. Both beat Wall Street forecasts. Even with heavy R&D spending up 5% and investments in AI chips, the company delivered $35.8 billion in operating cash flow, up 60% YoY. Free cash flow was $5.9 billion, down a bit due to capex. Microsoft returned $12.7 billion to shareholders in Q2 dividends plus buybacks, 32% more than a year ago.

CEO Satya Nadella framed the results as proof of Microsoft’s AI leadership. He said, “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business larger than some of our biggest franchises.” CFO Amy Hood noted, “Microsoft Cloud revenue crossed $50 billion this quarter,” and added that every measure “exceeded expectations.”

Looking ahead, Microsoft guided Q3 revenue to roughly $80.7 to $81.8 billion, up about 15 to 17%. They expect Intelligent Cloud to grow roughly 27% to 29%, with Azure around 38%. Analysts have similar estimates: consensus is for full-year 2026 revenue near $324 billion and EPS around $16.46 versus last year’s $14.06. In essence, Microsoft is forecasting continued mid-teens topline growth.

What Analysts Are Saying About MSFT Stock?

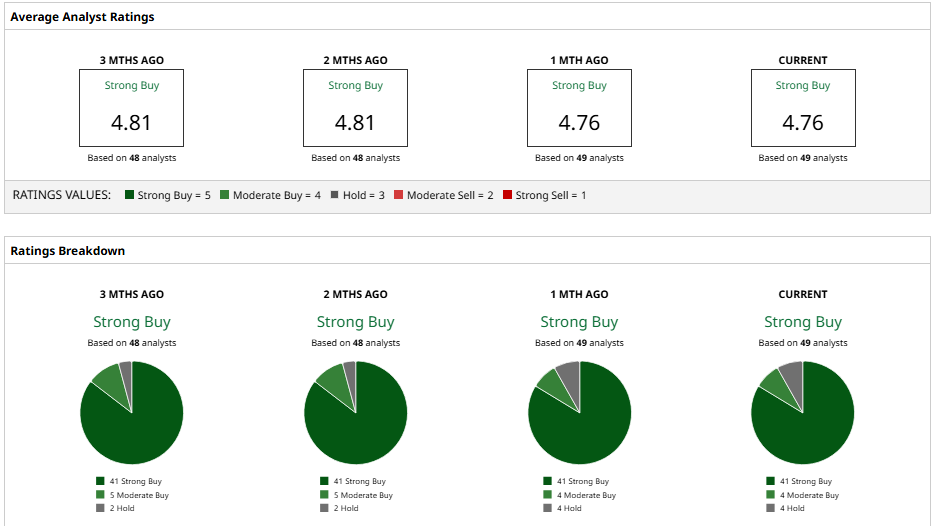

Wall Street’s consensus is strongly positive. Currently, 49 analysts cover MSFT with an average rating of “Strong Buy” and a mean target of $589.95. This gives a potential of almost 60% from the current price.

Key recent calls include Goldman Sachs kicking off in Jan 2026 at a “Buy” rating with $655, saying Microsoft has “discovery value” in AI and could reach $35 EPS by 2030. Jefferies reaffirmed a “Buy” at $675, citing continued cloud momentum. Bank of America also just reinstated coverage with a “Buy” and $500 target, highlighting Microsoft’s “dual advantage” of owning both AI infrastructure and the apps that use it

By contrast, a few cautious firms have lower targets. Morgan Stanley and UBS typically have “Overweight” ratings but around $550 to $600 targets.

As BofA’s Tal Liani put it, Microsoft’s ability to bundle AI into both Azure and Office gives it a unique “moat.” Even with heavy spending, analysts say the AI contracts backlog and cash flow support the long-term case. In short, most analysts love MSFT, as evidenced by the fact that they’ve raised estimates by low double-digits, and their price targets all sit far above today’s levels.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

/Quantum%20Computing/A%20concept%20image%20of%20a%20green%20and%20yellow%20motherboard_%20Image%20by%20Gorodenkoff%20via%20Shutterstock_.jpg)

/Broadcom%20Inc%20HQ%20photo-by%20Sundry%20Photogrpahy%20via%20iStock.jpg)