/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)

San Jose, California-based Western Digital Corporation (WDC) develops, manufactures, and sells data storage devices and solutions based on hard disk drive (HDD) technology. Valued at a market cap of $105.8 billion, the company is expected to announce its fiscal Q3 earnings for 2026 in the near future.

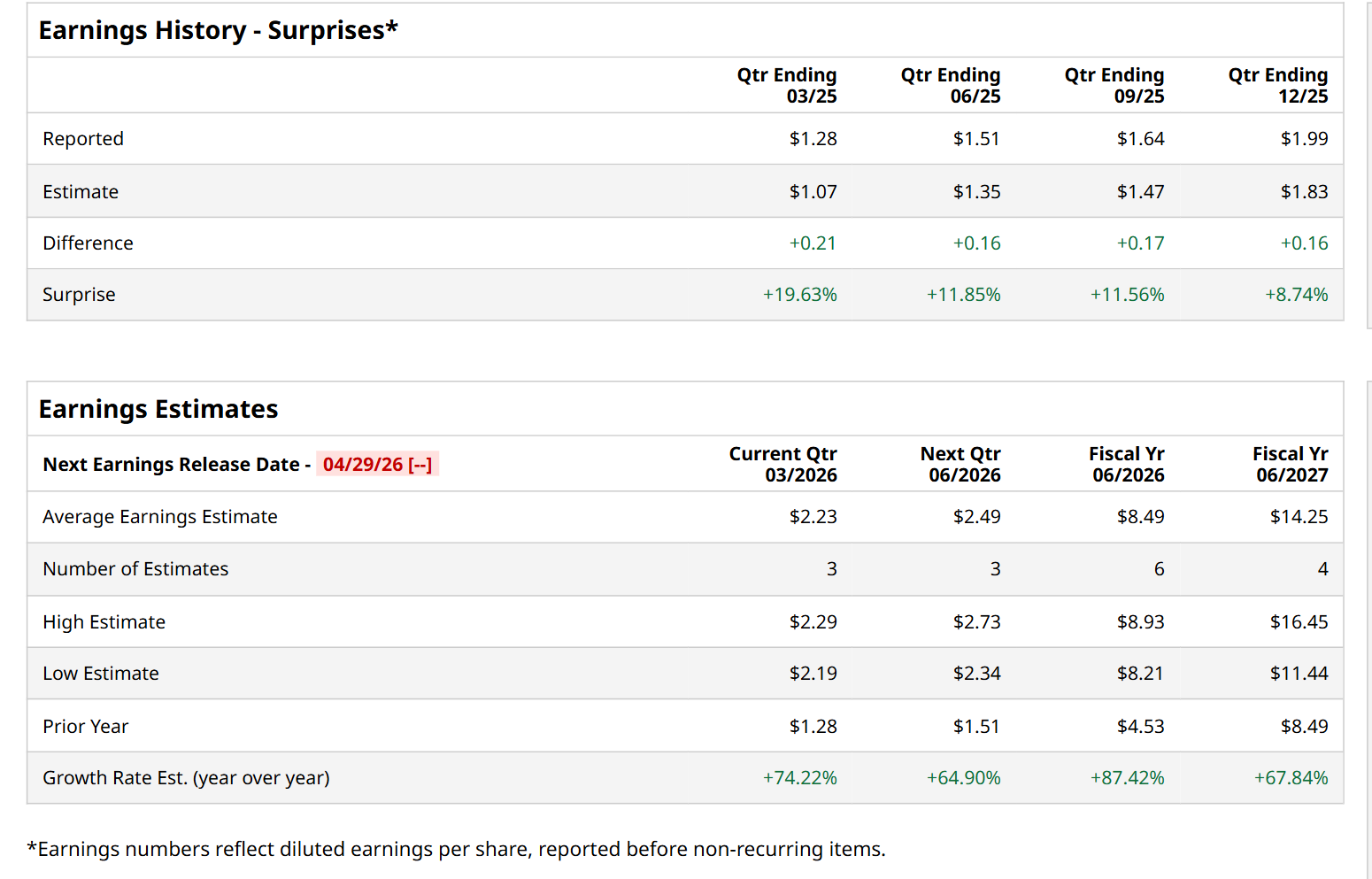

Before this event, analysts expect this tech company to report a profit of $2.23 per share, up 74.2% from $1.28 per share in the year-ago quarter. The company has topped Wall Street’s bottom-line estimates in each of the last four quarters. Its earnings of $1.99 per share in the previous quarter outpaced the forecasted figure by 8.7%.

For the current fiscal year, ending in June, analysts expect WDC to report a profit of $8.49 per share, representing an 87.4% increase from $4.53 per share in fiscal 2025. Furthermore, its EPS is expected to grow 67.8% year-over-year to $14.25 in fiscal 2027.

WDC has skyrocketed 960.4% over the past 52 weeks, significantly outperforming both the S&P 500 Index's ($SPX) 30.7% return and the State Street Technology Select Sector SPDR ETF’s (XLK) 49.8% uptick over the same time period.

On Apr. 6, WDC shares surged 3.1% after Morgan Stanley (MS) raised its price target on the stock to $380 from $368 while keeping its Overweight rating, citing robust demand for hard disk drives (HDDs).

Wall Street analysts are highly optimistic about WDC’s stock, with a "Strong Buy" rating overall. Among 25 analysts covering the stock, 20 recommend "Strong Buy," one advises a "Moderate Buy,” and four suggest "Hold." While the company is trading above its mean price target of $327, its Street-high price target of $440 suggests a 29.2% potential upside from the current levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Image%20of%20server%20racks%20in%20modern%20server%20room%20data%20center%20by%20Sashkin%20via%20Shutterstock.jpg)

/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)