/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

The world’s most important chipmaker is set to announce its earnings on April 16. Taiwan Semiconductor Manufacturing Company (TSM) manufactures chips for companies like Nvidia (NVDA) and Apple (AAPL), in addition to hyperscalers investing heavily in AI. For years, the company’s core business revolved around iPhones, tablets, and PCs. Since the emergence of AI, things have changed, and people are only now starting to see how much of an impact AI is having on companies’ business models.

Taiwan Semi's business can currently be separated into two segments. The AI part of the business manufactures chips at cutting-edge nodes (5nm, 3nm) using advanced packaging techniques. This is a high-margin business, which is currently capacity-constrained. Then there is the part that serves smartphones and PCs and involves legacy nodes like 28nm and 16nm, among others. This legacy business isn’t firing on all cylinders like the AI one, and this could soon become very relevant.

The earnings call on April 16 is important because it might finally force the company to utilize the capacity that is currently serving legacy nodes to improve the supply situation in AI chip manufacturing. We’ve seen memory companies like Micron (MU) and Samsung (SMSN.L.EB) divert their resources to serve high-bandwidth memory requirements. A similar situation could soon arise for TSM, but we’ll only find out on the day of the earnings.

About Taiwan Semi Stock

Taiwan Semiconductor Manufacturing Company is a manufacturer, packager, seller, and tester of integrated circuits and other semiconductor devices. The company operates across the United States, the Middle East, Taiwan, Japan, Europe, Africa, China, and more. It is also engaged in mask manufacturing, offering customer & engineering support services, investing in technology start-up companies, and other investment activities.

Taiwan Semi’s share price surged over 130% in the past year, representing a solid annual performance. The stock outperformed the broader S&P 500 Index ($SPX), which posted a return of about 30% during that time.

The chipmaker is expected to grow its earnings at a rate of 36.3% by the end of this year and by 23.5% by December 2027. A forward P/E of 24.15x seems reasonable considering the five-year average forward P/E is 22.26x. However, investors know very well that any geopolitical crisis involving Taiwan would make TSM a political issue, if not a bargaining chip in the race to AI dominance. Many investors continue to avoid the stock for that reason, irrespective of valuation.

Taiwan Semi used to be a consistent dividend payer with a decent yield. The emergence of the unprecedented AI demand and the resulting boom in business have stretched the valuation high enough for the yield to reduce by 35%. It must be said, though, that for a company that is central to advancements in AI, a 1.03% dividend yield is still not bad!

Taiwan Semi Beats Wall Street Expectations

On Jan. 15, Taiwan Semiconductor Manufacturing Company posted its Q4 FY 2025 results, beating both revenue and earnings estimates. Revenue for the quarter came in at $33.73 billion, surpassing the consensus estimate by $1 billion. Total revenue grew by 25.5% year-over-year (YoY). Its Non-GAAP EPS was recorded at $3.14, $0.16 above forecasts.

The company is scheduled to post its first-quarter fiscal 2026 earnings on April 16. According to the management, Q1 revenue is projected to be in the range of $34.6 billion to $35.8 billion. This is a 4% increase from the last quarter and a 38% rise YoY at the midpoint. The company expects its capital expenditure to range from $52 billion to $56 billion in 2026, up from $40.9 billion in 2025.

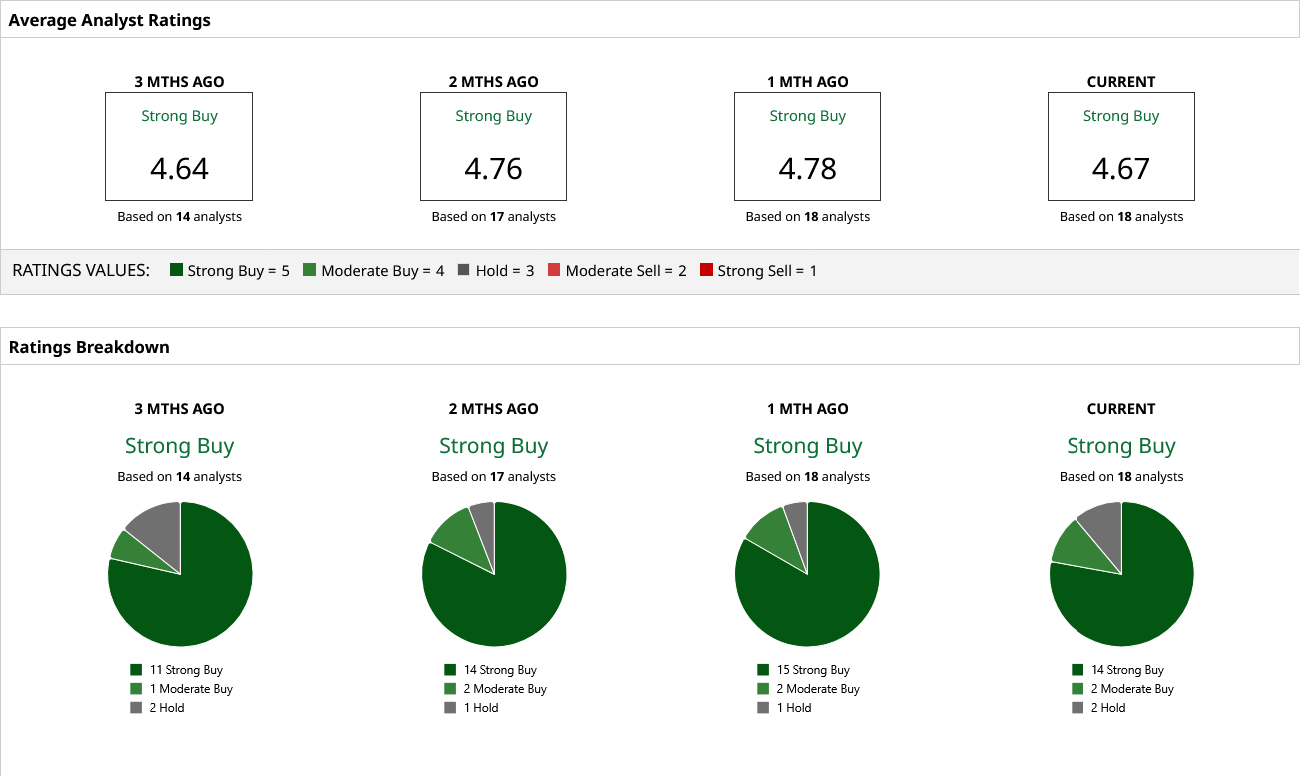

What Are Analysts Saying About TSM Stock?

Since the earnings report in January, three analysts have issued updates on the company’s share price forecast. Barclays, Bank of America, and D.A. Davidson updated their price targets on the stock to $450, $470, and $450, respectively.

TSM stock enjoys a consensus “Strong Buy” rating from the 18 analysts covering it on Wall Street, reflecting confidence in its growth potential. Based on analyst forecasts, the stock has a mean price target of $419.38, implying an additional 22.7% upside from the current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)