/AI%20(artificial%20intelligence)/Businessman%20touching%20the%20brain%20working%20of%20Artificial%20Intelligence%20(AI)%20Automation%20by%20Suttiphong%20Chandaeng%20via%20Shutterstock.jpg)

Nebius Group (NBIS) is a relatively new entrant in the artificial intelligence (AI) space that has scaled at an extraordinary pace. In just about a year and a half, the company has built what it describes as a global AI cloud platform, quickly establishing itself as a major provider of AI computing infrastructure. While the stock has climbed “just” 35% so far in 2026, Nebius shares are up 453% over the past year, wildly outperforming the S&P 500 Index’s ($SPX) 30% gain.

Is this a hidden AI gem or too risky to touch now?

Hypergrowth That Demands Attention

Nebius is an AI infrastructure and cloud computing company whose goal is to deliver high-performance, flexible AI cloud capacity to enterprises and fast-growing AI startups that require large processing power. Nebius’ business model has attracted a diverse customer base ranging from start-ups to large tech giants like Microsoft (MSFT) and Meta Platforms (META). This demand has led to growth that has been nothing but staggering. In the most recent fourth quarter, total revenue increased by 547% year-over-year (YoY) to $228 million, while annualized run-rate revenue (ARR) reached $1.2 billion. Its core AI cloud business grew 830% YoY. Despite this explosive revenue growth, Nebius is still unprofitable. But it achieved a positive adjusted EBITDA margin of 24%, which improved from 19% in the third quarter. The company also generated $834 million in operating cash flow in Q4 alone, largely from upfront payments tied to long-term contracts.

The demand for AI compute from enterprises and AI-native companies is skyrocketing, but supply remains scarce. Nebius is clearly benefiting from this imbalance, giving it strong pricing power and visibility into future revenue. This has been the company's most significant achievement, as it has consistently sold out its capacity, not only in the second half of 2025 but also in the first half of 2026.

To capitalize on this opportunity, Nebius is scaling aggressively, with plans to build nine new data centers globally and significantly increase its contracted power capacity. It has already secured over 2 gigawatts and plans to exceed 3 gigawatts by 2026. On the product side, in order to build a broader AI ecosystem, Nebius has launched Token Factory and acquired Tavily, adding agentic search and access to around 700,000 developers.

Furthermore, its big tech partnerships validate its technology and execution capabilities. It has fully delivered capacity for Meta and is actively deploying infrastructure for Microsoft as part of the multi-year agreement.

Ambitious Targets With Heavy Investment

Looking ahead, Nebius has ambitious goals, which will require enormous investments. The company targets $3 billion to $3.4 billion in revenue in 2026. It even plans to reach an annualized run-rate revenue of $7 billion to $9 billion by the end of 2026. To reach these goals, the company is targeting capital expenditures between $16 billion and $20 billion in 2026 alone. It has already secured 60% of this funding through its current cash balance. However, it is also exploring debt financing, asset-backed funding, and potentially equity issuance, which could increase dilution risk.

Nebius also holds strategic stakes in businesses like ClickHouse, recently valued at $15 billion, and other assets such as Avride. These holdings could serve as future funding sources or unlock additional shareholder value over time.

The Bear Case for Nebius Stock

Nebius’ staggering growth and bold goals make you wonder if this is a hidden AI gem worth grabbing today. However, the risks are equally significant. The business model is extremely capital-intensive, which could lead to potential share dilution. It also faces fierce competition from giants like Amazon (AMZN), Alphabet (GOOG) (GOOGL), and Microsoft. Thus, there is an execution risk in scaling infrastructure globally. Furthermore, the company’s growth is heavily reliant on continued AI demand, so any slowdown in AI spending or misstep in expansion could hit the stock hard.

Investors willing to take the risk should note that while the upside could be massive, so could the downside if the AI boom slows or capital markets tighten. All in all, Nebius is a classic high-risk, high-reward opportunity.

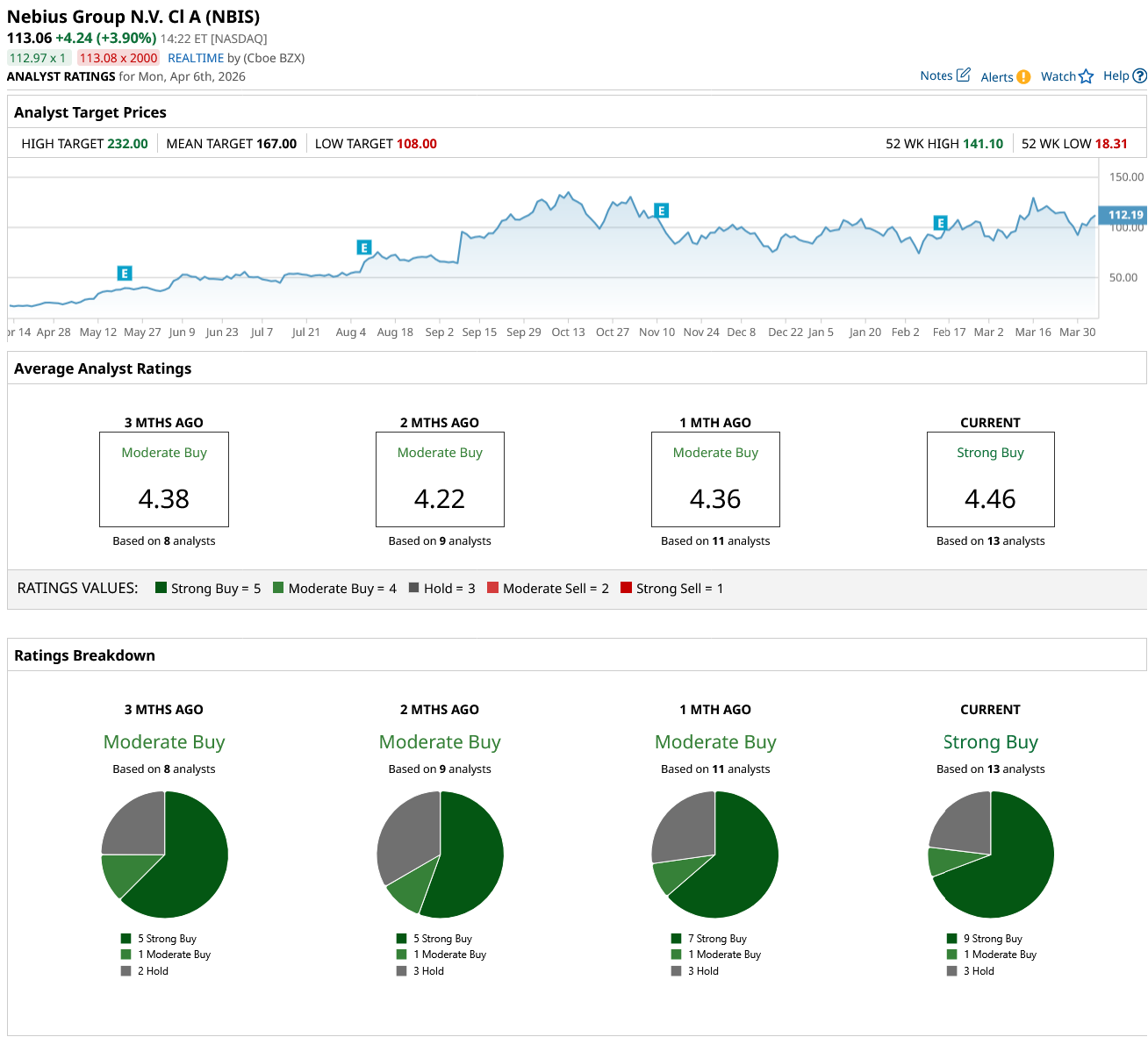

What Does Wall Street Say About NBIS Stock?

Overall, NBIS stock has earned a “Strong Buy” rating on the Street from a “Moderate Buy” rating a month ago. Out of the 13 analysts covering the stock, nine have a “Strong Buy” recommendation, one rates it a “Moderate Buy,” and three rate it a “Hold.” Wall Street sees a potential upside of 48% from current levels based on its average target price of $167. Plus, the high price estimate of $232 implies an upside potential of 105% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)