/Facebook-you've%20been%20Zucked%20by%20Annie%20Spratt%20via%20Unsplash.jpg)

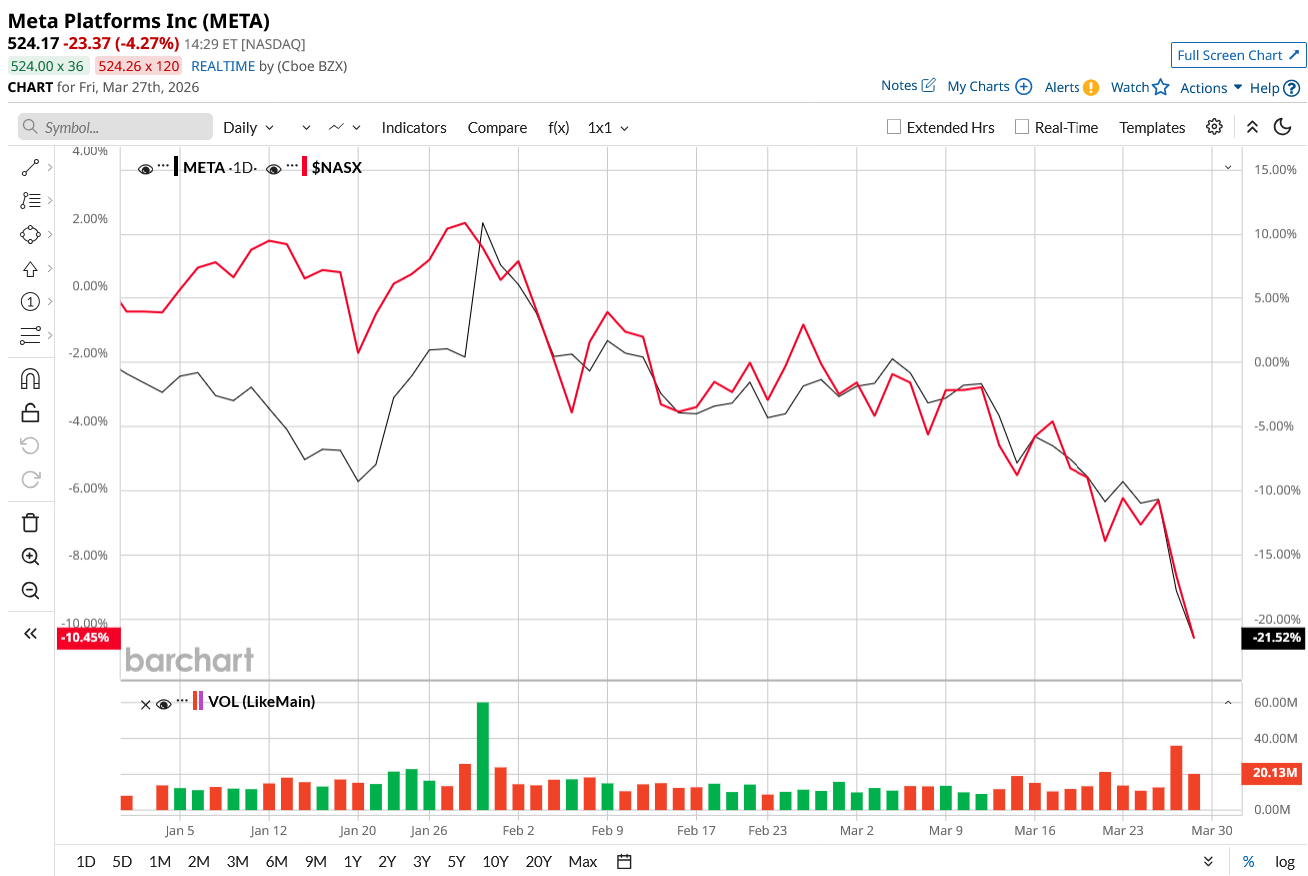

Meta Platforms (META) has entered one of its most turbulent phases in recent years. The stock is now down roughly 30% from its 52-week high of $796.25, wiping off more than $100 billion in market value. But this selloff isn’t triggered by one issue alone. A wave of legal setbacks, layoffs, and aggressive artificial intelligence (AI) spending has rattled investor confidence. While Meta navigates a complex transition from a high-margin social media business to a capital-intensive AI company, investors are wondering whether to buy, hold, or sell the stock right now.

Legal Risk Looms Over Meta’s Head

Meta’s legal setbacks have caught the market’s attention. According to Reuters, the Los Angeles jury found the company accountable for addictive platform design, while a separate New Mexico ruling levied a $375 million penalty over child safety violations. While the minimal fines won’t put a dent in Meta’s financials, the biggest concern is these decisions could open the floodgates to thousands of similar lawsuits. META stock dipped sharply by almost 8% on March 26 and is down 21% year-to-date (YTD), compared to the tech-led Nasdaq Composite Index ($NASX) fall of 9.7%.

Besides this, Meta continues to face long-standing regulatory scrutiny on whether it has built an illegal monopoly through acquisitions like Instagram and WhatsApp.

At the same time, Meta has announced an aggressive restructuring plan that includes laying off 700 to 1,000 employees. But these layoffs are happening while the company pays massive executive compensation packages, which Meta is being criticized for. While the legal issues add uncertainty, Meta’s business fundamentals remain robust. Meta generated $200.1 billion in revenue in 2025 with $60.4 billion in net income. At the end of 2025, it held $81.6 billion in cash balance along with $43.6 billion in free cash flow. Its debt-to-equity ratio remains low at 0.27. The social media giant’s underlying business model remains strong, with more than 3.5 billion daily users across its platforms.

However, the biggest concern for investors now is that Meta’s cost of AI ambition is exploding.

The Cost of AI Ambition Is Exploding

Meta’s AI spending is exploding, with plans to spend as much as $162 billion to $169 billion in 2026, largely driven by AI investments. It is also ramping up infrastructure spending dramatically, including a new AI data center project in Texas that might cost up to $10 billion. Additionally, it is offering massive compensation packages to attract top AI talent to build its own chips in the AI arms race against rivals Microsoft (MSFT), Alphabet (GOOG) (GOOGL), and Amazon (AMZN). These investments will pay off in the long run, but investors are concerned about short-term margin pressure. A classic example of this is Meta’s Reality Labs (RL) segment. Meta has been heavily investing in the metaverse segment, expecting it to eventually generate profits.

Nonetheless, the RL segment continues to lose money, accounting for an operating loss of $19.1 million in 2025. Meta anticipates losses to be similar this year, although it is shuttering the company's namesake Metaverse app as part of its shift to AI. Thanks to its social media apps, it compensates for the significant losses in the RL segment. The Family of Apps generated $198.7 million in revenue in 2025, a 22.4% increase year over year (YoY).

With AI costs rising and Reality Labs still operating at a loss, the legal issues have added to the uncertainty, unsettling investors.

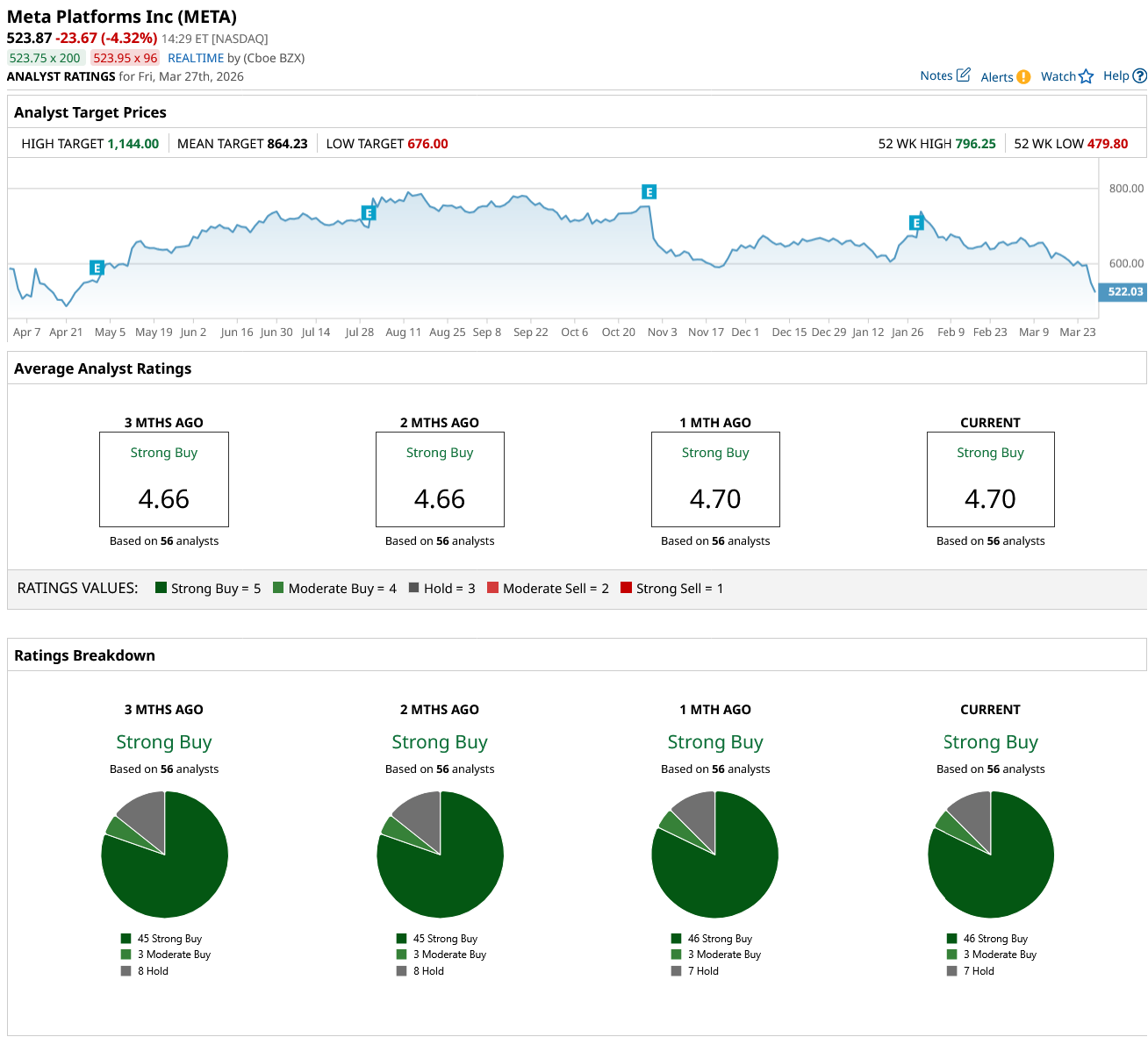

Nonetheless, Wall Street remains hopeful about Meta's AI vision. The consensus on META stock is a “Strong Buy” with an average target price of $864.23, which implies an upside potential of 65% from current levels. Of the 56 analysts tracking the stock, 46 rate it as a "Strong Buy," three as a "Moderate Buy," and seven as a "Hold." META's high price target of $1,144 implies that the stock could go up 118% from its current levels.

The Final Verdict: Buy, Hold, or Sell META Stock?

Meta is scaling its core business while investing heavily in the infrastructure, products, and processes essential for an AI-driven future. The bear case says this transition phase, along with legal risks, could compress margins and limit upside in the near term. The bull case says Meta remains a dominant digital advertising platform with billions of users, with strong fundamentals and long-term AI upside.

It could take a while before Meta’s AI investments translate into sustained earnings growth and platform dominance. For long-term investors, I believe this is more of a "hold with caution" moment than a buy or sell.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)