/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

The so-called “Magnificent Seven” stocks once dominated the market, driving most of the gains and becoming the go-to names for investors seeking high growth. But recently, the AI momentum has cooled off. Nonetheless, Microsoft (MSFT) continues to show strong underlying growth, suggesting that while the broader group may be slowing, this tech giant still has plenty of strength left. Even Jefferies and Piper Sandler analysts have chosen Microsoft as their top AI pick, citing the stock's reasonable valuation when compared to its long-term profitability potential.

While MSFT is down 26% year-to-date (YTD), compared to the tech-heavy Nasdaq Composite Index ($NASX) fall of 9%, its fundamentals suggest it could rebound by 89% from current levels.

The Core Story Is Being Overlooked

While the market remains fixated on the ongoing U.S.-Iran war news, high-growth stocks like Microsoft are quietly laying the groundwork for their next leg higher. In its fiscal Q2 2026, Microsoft’s cloud segment surpassed $50 billion in revenue for the first time, growing 26% year-over-year (YoY). Management emphasized that AI adoption is still in its early stages, with significant expansion expected across the entire technology stack.

Financially, the company remains very strong. Revenue increased 17% YoY to $81.3 billion in Q2, while earnings per share increased 24% to $41.14. At the same time, heavy investment in AI infrastructure pushed capital expenditures to $37.5 billion, owing to investments in GPUs, CPUs, and data centers. This weighed slightly on margins, with gross margin dipping to 68%. Demand continues to outpace supply, particularly in Azure. Remaining performance obligations, or RPO, reached $625 billion, providing strong visibility into future revenue. What stands out is while Microsoft spent decades building its legacy products, the AI business alone has reached an unimaginable scale in a relatively short period of time.

At the core of Microsoft’s growth story is its massive investment in infrastructure. Microsoft is optimizing efficiency through what it calls “tokens per watt per dollar,” which focuses on lowering costs while scaling performance. The company is also diversifying its hardware stack by combining chips from Nvidia (NVDA) and AMD (AMD) with its own custom silicon, like the Maya and Cobalt series, improving both performance and cost efficiency.

Beyond infrastructure, Microsoft is investing in what it sees as the next generation of software, AI agents. Its Foundry platform is already gaining traction, with a quick increase in high-spending customers. Meanwhile, its Fabric data platform has grown to a $2 billion run rate with significant momentum. Furthermore, Copilot has become a real monetization engine by quickly becoming a core productivity tool for both consumers and enterprises. In software development, GitHub Copilot has grown rapidly, while in cybersecurity, AI tools are significantly reducing manual workloads.

Looking ahead, management expects Azure to grow 37% to 38%, even if overall cloud margins may compress slightly due to ongoing AI investments. But total revenue is expected to rise by 15.8% to a range of $80.65 to $81.75 billion next quarter. Despite the heavy investments, Microsoft generated $5.9 billion in free cash flow and returned $12.7 billion to shareholders via dividends and share repurchases.

For the full fiscal year 2026, analysts expect Microsoft’s revenue to increase by 16.4% to $327.8 billion, followed by a 22% increase in earnings to $16.73 per share. Many analysts believe Microsoft is a cheap AI stock and that its long-term earnings potential has not been recognized yet. This is probably why the stock is trading at 19 times forward 2027 earnings, which are expected to increase by 12.6%.

Is This a Bottom or Just a Pause Before the Next Leg Higher?

The market’s recent hesitation around mega-cap tech stocks is largely tied to concerns over valuation and rising AI spending. Yet Microsoft still appears attractively valued relative to its long-term AI-driven growth potential.

Despite being an established tech titan with a wide array of legacy products, the company has remained resilient in different economic cycles. And it is still growing, with cloud demand accelerating and adoption deepening, supported by a full-stack AI ecosystem spanning infrastructure, platforms, and applications. While capital spending is massive, these investments reflect the cost of building a dominant position in what could be the most important technology shift in decades.

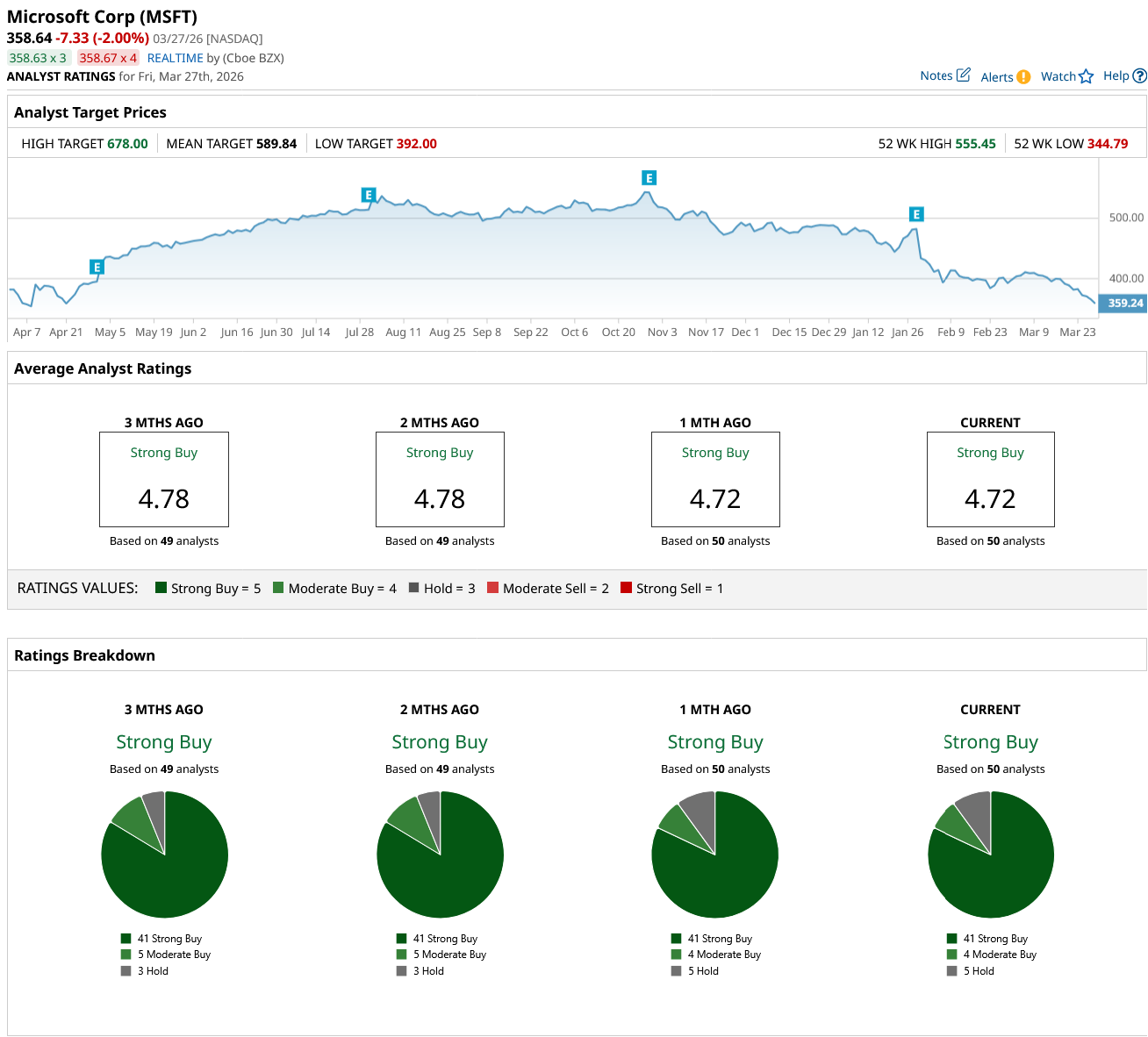

This explains why analysts' stance on Microsoft's stock hasn’t changed over the last three months, despite the market’s reaction. Overall, MSFT stock has a consensus “Strong Buy” rating. Of the 50 analysts covering the stock, 41 rate it a “Strong Buy,” four rate it a “Moderate Buy,” and five rate it a “Hold.”

MSFT stock is trading 35% below its 52-week high of $555.45. This pullback could be an opportunity for investors to buy this tech titan on the dip, as the average target price suggests the stock could surge 64% from current levels. Plus, its high price estimate of $678 implies the stock could rally 89% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)