/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

Jefferies believes Microsoft (MSFT) stock remains attractively valued, even as the company strengthens its leadership in artificial intelligence (AI). While many newer AI-focused companies have captured headlines, legacy players like Microsoft may ultimately prove more resilient.

Why Is Jefferies So Optimistic?

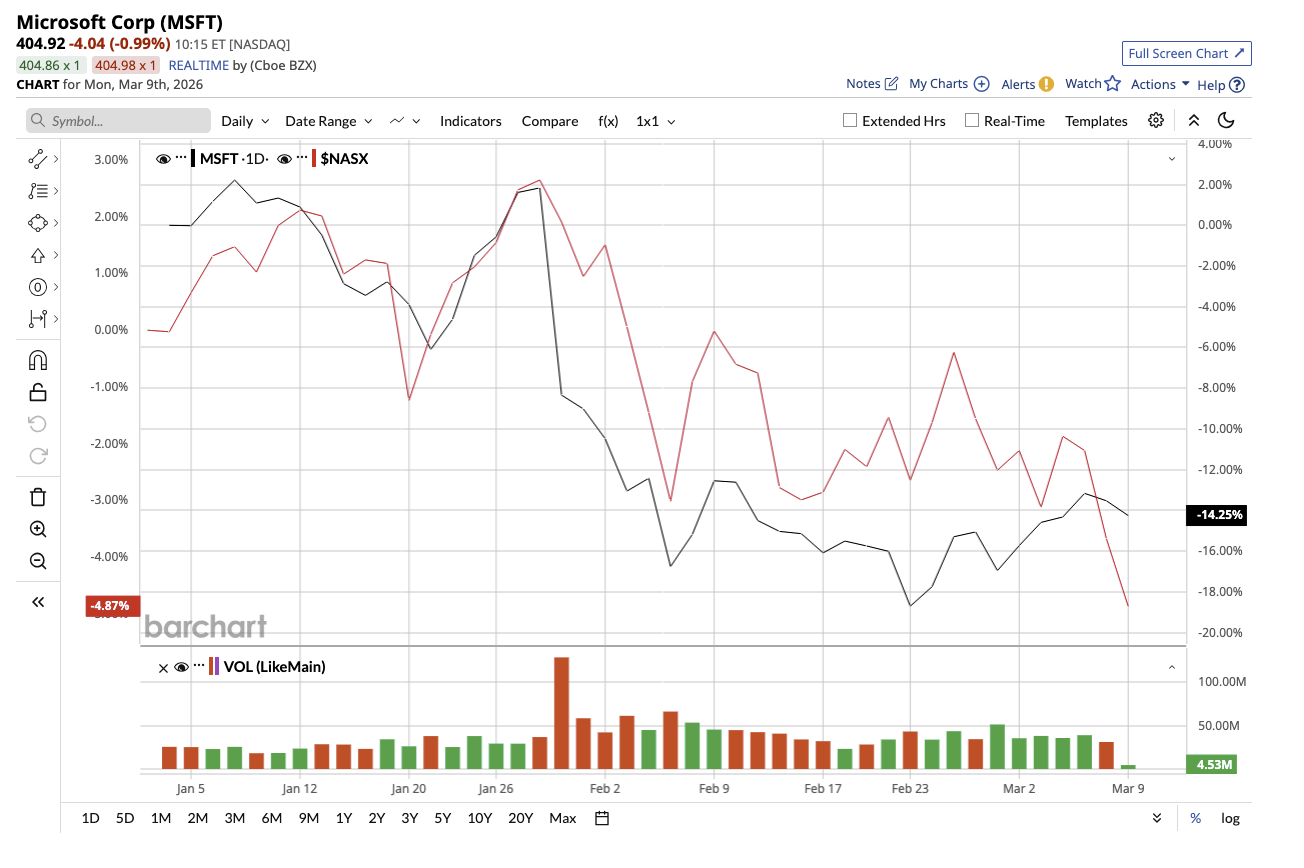

Recently, Jefferies reiterated its “Buy” rating and maintained a $675 price target for MSFT stock, following a meeting with Microsoft’s head of investor relations. MSFT stock is down 16% so far this year, compared to the tech-heavy Nasdaq Composite Index’s ($NASX) dip of 2%. The firm's target price implies the stock has potential upside of 67% from current levels.

Despite Microsoft’s strong positioning in AI infrastructure, cloud, and enterprise software, Jefferies argues that the stock does not fully reflect the company’s long-term earnings potential. What's more, Microsoft just proved the same in its second quarter of fiscal 2026 why it is still a must-own stock.

In Q2, revenue surged 17% year-over-year (YOY) to $81.3 billion, while EPS climbed 24% to $4.14. The company’s cloud business generated more than $50 billion in quarterly revenue for the first time, an increase of 26% YOY. Within the cloud business, Intelligent Cloud revenue rose 29% to $32.9 billion, while Azure and other cloud services surged 39%.

Management stated that cloud demand continues to exceed supply, owing to AI workloads. Remaining performance obligations reached $625 billion, highlighting the durability of enterprise AI spending flowing through Microsoft’s ecosystem.

Positioned for Long-Term AI Leadership

Jefferies noted that AI margins appear to be growing faster than Azure margins at a comparable level. Despite spending $37.5 billion on capital expenditures, with about two-thirds going to GPUs and CPUs, operating margins increased to 47%. The company also paid out $12.7 billion to shareholders in a single quarter. Jefferies' bullish stance stems from the fact that Microsoft has the ability to scale infrastructure aggressively while maintaining profitability and returning capital to shareholders.

Another point Jefferies emphasized is that the long-term value of AI may eventually be concentrated on the application layer, where AI agents operate within business workflows. Microsoft’s accelerating Copilot and platform adoption strengthens this argument. In Q2, Microsoft 365 Copilot had 15 million paid seats, a 160% increase over the previous year. Meanwhile, GitHub Copilot surpassed 4.7 million paid subscribers, a 75% YOY increase. Management also noted that the count of customers spending over $1 million per quarter on Foundry climbed roughly 80%, and more than 250 clients are expected to process upwards of 1 trillion tokens this year.

Microsoft's Valuation Appears Reasonable

Despite these growth drivers, Jefferies argues that Microsoft’s valuation remains reasonable. Currently, Microsoft is trading at 25 times forward earnings. Analysts predict earnings to increase by 22.6% in fiscal 2026, followed by 12.6% growth in 2027. Jefferies also noted that Microsoft's 10-year average multiple is 23.5 times.

Aside from Jefferies, Piper Sandler named Microsoft its top AI pick, even though the firm is "pessimistic" about software companies right now. The firm has a “Overweight” rating for MSFT stock with a price target of $600.

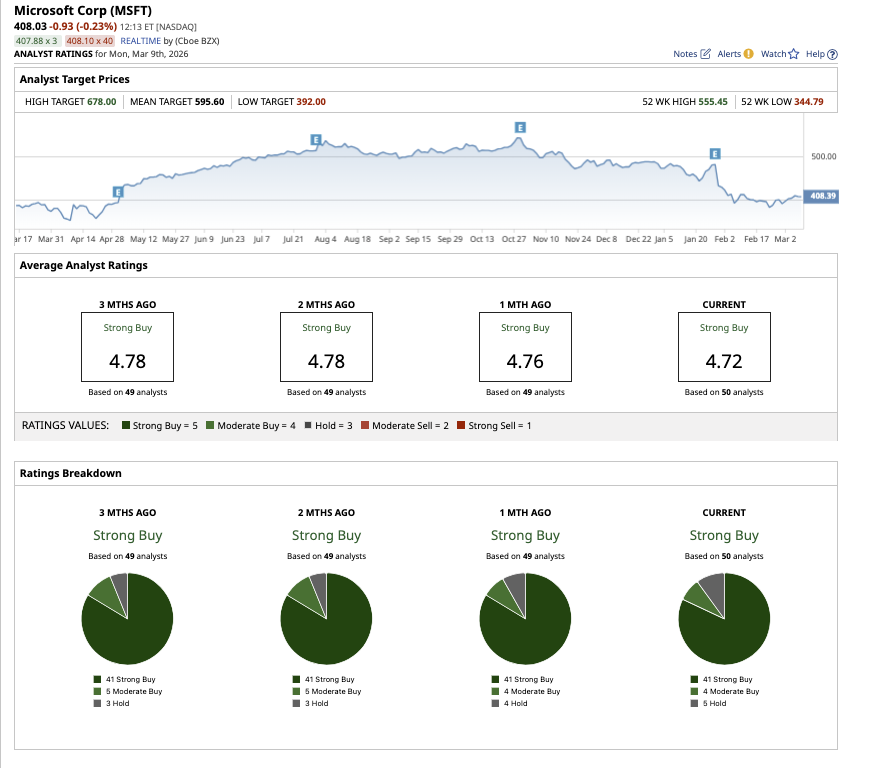

Wall Street is also optimistic about Microsoft’s long-term AI prospects, assigning it a consensus “Strong Buy” rating. Of the 50 analysts covering MSFT stock, 41 have a “Strong Buy” recommendation, four suggest a “Moderate Buy,” and five rate the stock as a “Hold.” MSFT stock has a high price target of $678, a low target of $392, and a mean price target of $595.60.

Microsoft offers a rare combination of scale, AI leadership, legacy products, and margin strength with an attractive valuation. Investors who can ignore the short-term noise might find this dip an attractive opportunity to buy or increase exposure to the stock.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.