Geopolitics has a way of quietly slipping into commodity charts, and this time, the shockwave came from Iran. Fresh strikes across the Gulf have rattled key Aluminum Jun '26 (ALM26) hubs, hitting giants like Emirates Global Aluminium, and the Aluminium Bahrain, which is the world’s largest single-site smelter. With the Strait of Hormuz effectively choked and nearly 9% of global supply disrupted, the market did not wait to react. Prices on the London Metal Exchange (LME) spiked to near four-year highs, reminding everyone how fragile supply chains can be when conflict sits at the center.

But this is not just about war-driven panic. Aluminum sits at the heart of modern industry, powering everything from electric vehicles (EVs) and renewable infrastructure to aerospace and construction. Plus, with demand rising, especially in China, the market has very little cushion left. So, when supply gets hit, the impact spreads fast. Meanwhile, we are already seeing cracks, with industries like metal packaging starting to explore alternatives as the pressure builds.

Rio Tinto Group (RIO), one of the world’s largest producers of aluminum and its raw materials, is suddenly back in focus, with its stock catching momentum as prices climb impressively. The market seems to be pricing in more than just a short-term spike.

But once the dust settles and supply normalizes, does this mining giant’s stock still have a long-term bull case, or is this rally just riding a geopolitical wave? Let’s take a closer look.

About Rio Tinto Stock

Rio Tinto is one of those old-world giants that has kept pace with a new-world economy. Founded in 1873 and based in London, the company has built a massive global footprint, spanning iron ore, copper, aluminum, and a growing push into critical minerals like lithium. It does not just mine, but controls the entire chain, from extraction to refining to shipping, which gives it scale and staying power through commodity cycles. With a market cap of around $117.07 billion, Rio remains a heavyweight in the resource world.

Where things have gotten more interesting recently is the aluminum business. Rio operates a fully integrated setup, from bauxite and alumina to finished aluminum, keeping quality tight and supply steady. Its Canadian smelters, powered by renewable hydropower, sit among the lowest-cost and lowest-emission producers globally. Through its ELYSIS partnership with Alcoa (AA) and support from Apple (AAPL), Rio is pushing a breakthrough – aluminum made with near-zero emissions, already making its way into modern products.

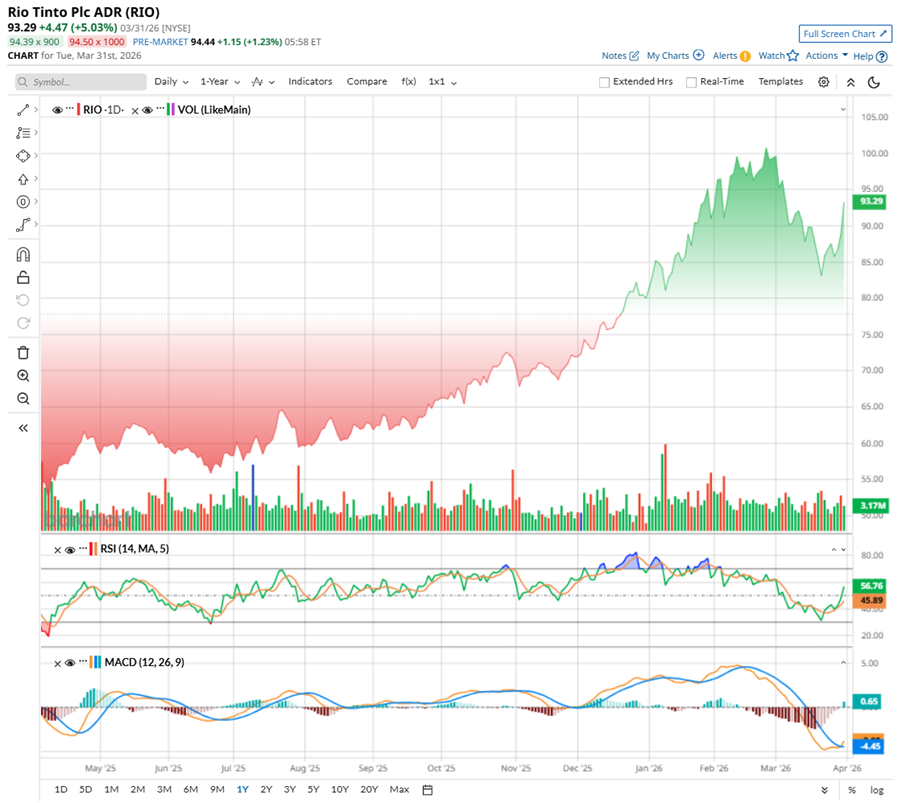

Rio Tinto has been on a steady climb, and the chart tells a story of momentum that’s hard to ignore. Over the past 52 weeks, the stock has rallied 57.4%, riding a wave of improving sentiment and stronger commodity prices. It touched a high of $101.53 in late February before cooling off slightly, slipping around 7% - more like a breather than a breakdown.

Zooming in, the pace feels even sharper. In just six months, RIO has surged over 43%, and three months into the year, it is already up 18.8%. A 8.3% jump in the past five days alone shows that rising aluminum prices are adding fuel to the fire.

Technically, the signals are lining up. Volumes have been picking up, hinting at growing participation. The 14-day RSI, which dipped near oversold levels in March, has now climbed back to 59.35, suggesting momentum is rebuilding without being overheated. Meanwhile, the MACD has just crossed above its signal line, often seen as an early sign of a bullish shift.

Putting it all together, and RIO’s price action feels less like a short spike and more like a trend trying to find its next leg higher.

Even after the recent run-up, Rio Tinto does not look stretched. The stock is priced at around 10.54 times forward adjusted earnings, still sitting comfortably below many peers in the mining space. The PEG ratio of 1.29 suggests growth is fairly aligned with valuation – not overheated, not lagging. In simple terms, the market is not overpaying yet. And if aluminum prices keep firm or push higher, there is still room for this story to run a bit more.

Meanwhile, Rio Tinto has not lost sight of its income investors. Rather, it has been quietly rewarding patience year after year. The miner sticks to its semiannual dividend rhythm, almost like clockwork. Its latest payout of $2.54 per share, due in April, brings the annual total to $4.02, offering a solid 4.31% yield. That’s comfortably ahead of what one would get from the broader SPDR S&P 500 ETF Trust (SPY), making RIO not just a growth play, but a steady income story too, especially when markets feel anything but steady.

A Closer Look at Rio’s Stellar Q4 Report

Rio Tinto exited 2025 with resilience. Revenue climbed to $57.6 billion, up 7% year-over-year (YOY), comfortably beating expectations. Earnings held firm, too, with EPS at 6.69, while operating profit came in at $14.9 billion. Cash kept flowing, with operating cash flow rising 8% annually to $16.8 billion and EBITDA touching $25.4 billion, proof that execution stayed tight even as markets shifted.

But beneath the headline numbers, the real story was in the mix. Aluminum and copper stepped up, carrying more weight in the portfolio. And Rio did not just earn, it returned. A $6.5 billion dividend, sticking to its 60% payout discipline, marked the tenth straight year at the top end, all while funding future growth and keeping the balance sheet clean.

Operationally, momentum came back strong. Iron ore rebounded with record output from Pilbara in Q4. Simandou shipped its first ore - no small feat - and a signal that big projects are moving on schedule. Copper surged, powered by Oyu Tolgoi’s underground ramp-up. Lithium and bauxite also hit new highs, quietly building Rio’s future-facing edge.

Now, zoom into aluminum, production rose 3% annually to 3,380 kt, with underlying return on capital employed at a solid 13%. But it was not just volume, but was control. Rio increased its stake in Boyne and fully took over Tiwai Point, tightening its grip on key assets. New Zealand Aluminium Smelter returned to full capacity in Q4, while Kitimat held steady despite constraints. In a volatile supply environment, stability became strength.

Looking ahead, Rio Tinto is keeping things steady, targeting around 3% annual growth in copper-equivalent output through the decade. For 2026, growth looks more measured, with volumes rising about 3%, partly offset by closures at Arvida and Darvik, a mid-year slowdown at Yarwun, and softer grades at Escondida. On the aluminum front, production is expected to land between 3.25 million tons and 3.45 million tons – steady, but not explosive.

Analysts tracking Rio Tinto expect fiscal 2026 EPS to rise about 27% YOY to $8.43, before growing by another 8.7% annually to $9.16 in fiscal 2027.

What Do Analysts Expect for Rio Tinto Stock?

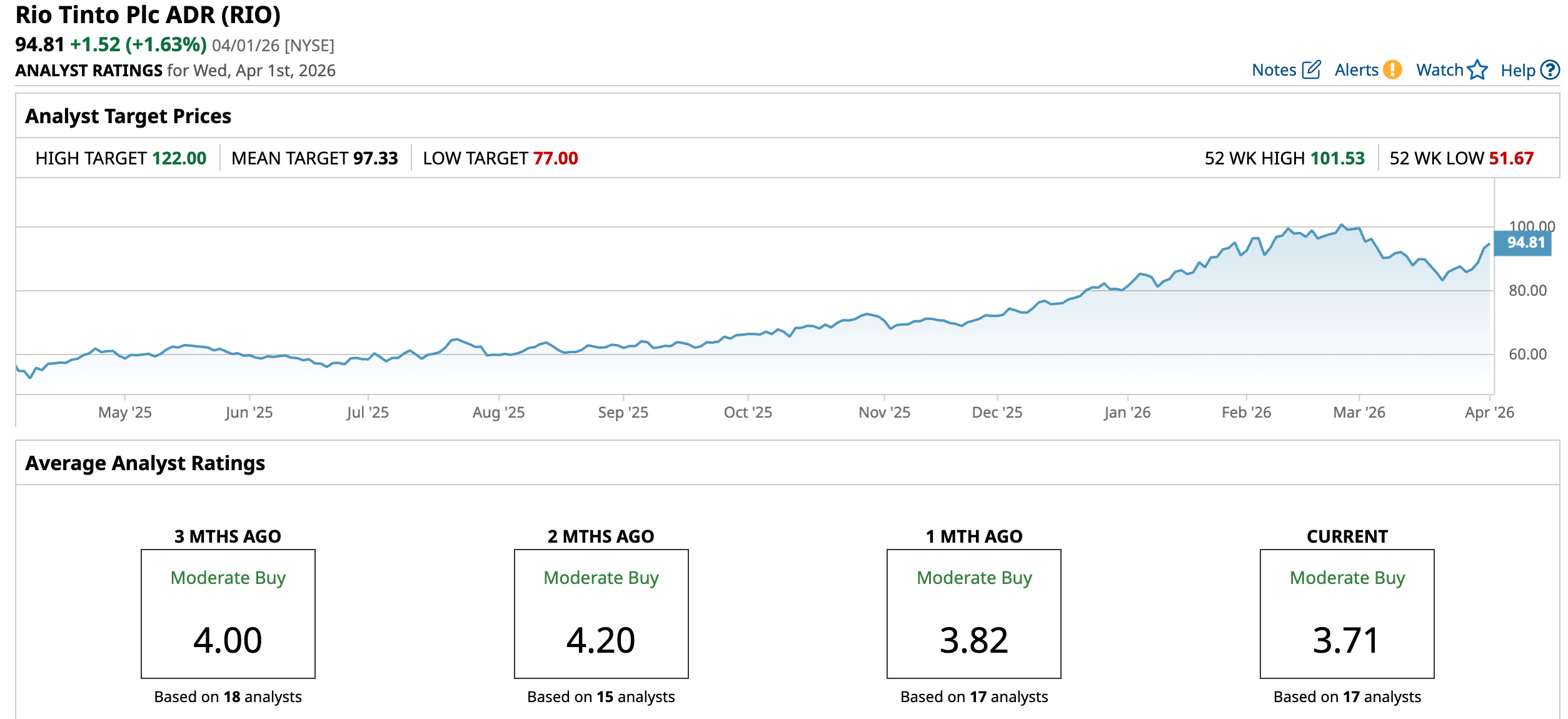

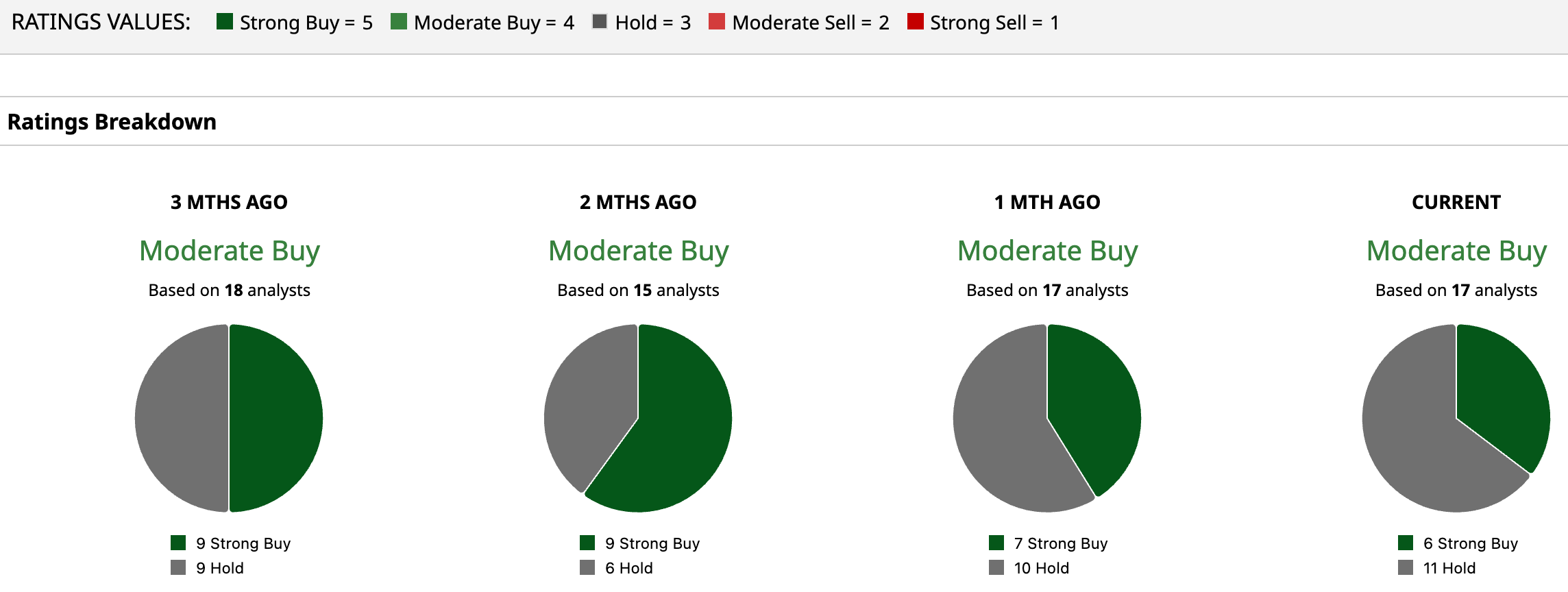

Analysts monitoring RIO are optimistic, with a consensus rating of “Moderate Buy.” Out of 17 analysts, six recommend a “Strong Buy,” and the remaining 11 are on the sidelines, giving it a “Hold” rating.

Its average price target of $97.33 implies upside potential of 2.7%. Meanwhile, the Street-high target of $122 suggests RIO stock could rise as much as 28.7% from the current price levels.

Final Thoughts on RIO Stock

The Middle East tensions may have lit the spark, but the story around Rio Tinto runs deeper. Aluminum demand, driven by EVs and clean energy, is steadily building, and Rio’s integrated, low-cost operations position it well to ride that wave.

The recent rally may have started with supply disruption, but strong fundamentals, disciplined capital returns, and steady growth plans suggest there is more beneath the surface. Still, with commodities, cycles matter. If prices cool, momentum could fade. But if demand holds firm, Rio’s long-term case stays very much alive.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)