Macro risks are rising amid ongoing Iran war tensions. Investors are growing more cautious about stretched valuations and uncertain growth outlooks. Smart money is quietly rotating toward businesses with rising demand and long-term structural tailwinds. As risks climb and investors become more selective, Western Digital (WDC) and Seagate Technology (STX) appear to be intriguing long-term buy-and-hold stocks.

Let's take a closer look.

Market Darling Stock #1: Western Digital (WDC)

Western Digital is a global technology company that designs, manufactures, and sells data storage solutions. Even though the market is fatigued with AI stocks, the AI explosion is far from over. Every stage of artificial intelligence, from training and deployment to ongoing inference, is largely reliant on the efficient storage of and access to massive volumes of data. This creates a significant and long-lasting demand cycle for storage infrastructure companies like Western Digital.

Valued at $93.3 billion by market capitalization, WDC stock has soared 46% year-to-date (YTD) while the S&P 500 Index ($SPX) has fallen more than 7%. The company’s second-quarter performance and strong outlook are most likely what has boosted investor confidence in WDC stock.

The rapid growth of AI is also leading to continued growth in cloud computing, with Western Digital seeing a 25% increase in revenue to $3.02 billion and a 78% increase in EPS to $2.13 in Q2 2026. Gross margin expanded to 46.1% compared to 38.4% in the prior-year period, owing to higher-capacity drives and disciplined cost management. Cloud revenue accounted for 89% of total revenue, reaching $2.7 billion, an increase of 28% year-over-year (YOY). Meanwhile, the client segment generated $176 million in revenue, up 26% YOY, while the consumer segment contributed $168 million, declining slightly by 3% YOY.

The company generated $653 million in free cash flow, returned $615 million through share repurchases, and distributed $48 million in dividends. Western Digital has $2 billion in cash on its balance sheet as of Q2. To keep ahead of the demand curve, the company is speeding the development of next-generation high-capacity drives like HAMR and ePMR, which are gaining traction. It supplied approximately 3.5 million units of its newest ePMR systems, which have capacities of up to 26 terabytes for CMR and 32 terabytes for UltraSMR technology.

With AI adoption still in its early stages and data generation accelerating, the demand for storage is likely to rise significantly. The company is also strengthening its relationships with hyperscale customers. It has secured definite purchase orders from its top seven customers through calendar year 2026. Western Digital has also signed long-term deals with three of its top five customers, extending visibility beyond 2027 and even 2028. These long-term partnerships reduce earnings volatility, which is critical in the cyclical hardware business.

For Q3, the company expects 40% revenue growth with a 69% increase in adjusted EPS to $2.30. Analysts forecast earnings to increase by 80% in fiscal 2026, followed by 52% growth in fiscal 2027. For the level of growth expected, WDC stock still remains under-the-radar and underappreciated.

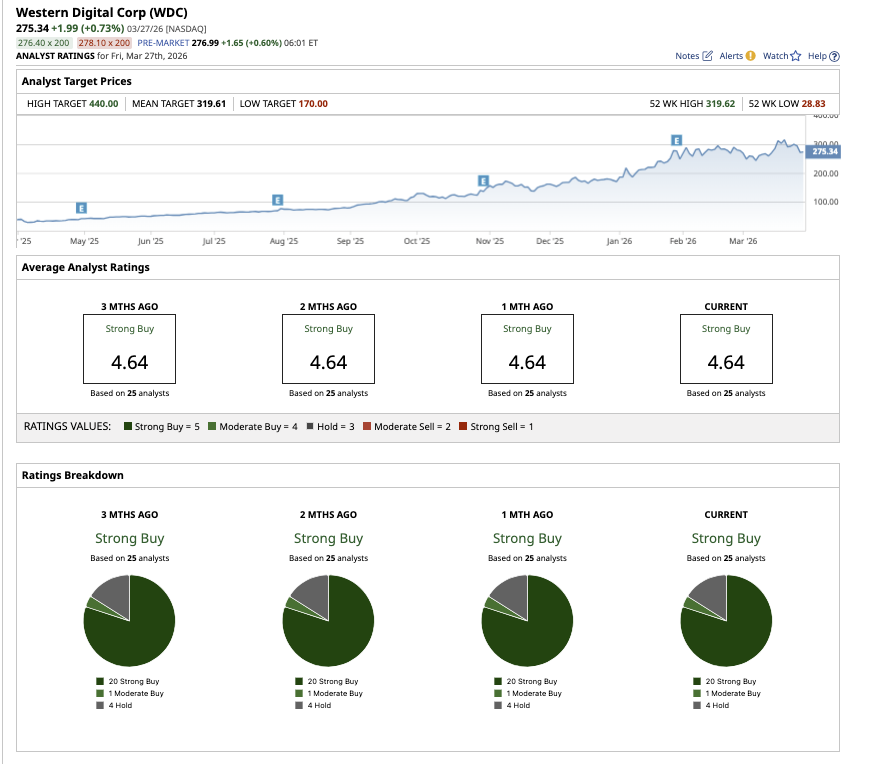

Western Digital is benefiting from two of the most powerful trends now, cloud and AI, which is why it has turned into a market favorite. Overall, the consensus on WDC stock is a "Strong Buy" rating. Out of 25 analysts with coverage, 20 have a “Strong Buy" rating, one suggests a “Moderate Buy,” and four have a “Hold.” The average target price of $319.61 suggests 27% potential upside from current levels, while the high price estimate of $440 implies 75% potential upside.

Market Darling Stock #2: Seagate Technology (STX)

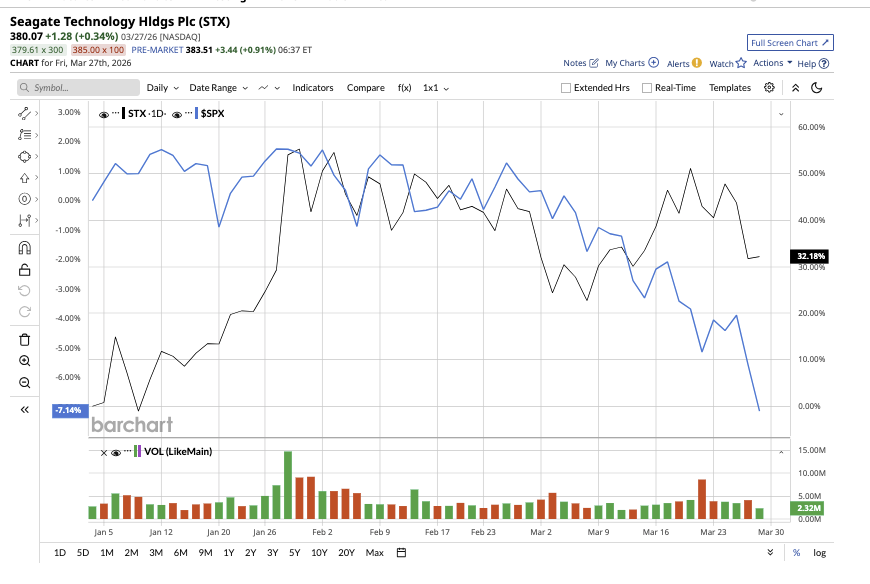

Valued at $82.8 billion by market cap, Seagate’s core business is quite similar to Western Digital. It is also a global data storage company that focuses on designing and manufacturing storage hardware, particularly for large-scale data demands. Like Western Digital, Seagate is heavily tied to cloud infrastructure and AI data storage demand. That explains the 30% surge in STX stock so far this year, outperforming the broader market.

The demand for large-scale data storage is growing rapidly, particularly in cloud systems. Hard drives also play an important role in managing data across cloud and edge environments, making Seagate's core business crucial. In Q2 2026, revenue increased by 22% YOY to $2.83 billion. The company shipped 190 exabytes during the quarter, a 26% increase from the prior year.

Notably, data centers accounted for 87% of shipment volume, generating $2.2 billion in revenue, an increase of 28% YOY. Within this segment, cloud nearline capacity reached almost 26 terabytes per drive and is expected to grow further with the ramp of HAMR products.

At the start of 2025, the company began shipping its star product — Mozaic-based HAMR drives with 3 terabytes per disc — to its first cloud service provider customer. By year-end, management noted that quarterly HAMR shipments exceeded 1.5 million units and continue to ramp.

Meanwhile, second-generation Mozaic devices with 4 terabytes per disc are scheduled to become available soon. Looking ahead, Seagate plans to increase the capacity of each disc to 10 terabytes over the next decade, giving the company a competitive advantage by allowing each drive to hold more data in the same space while charging less.

The bottom line rose alongside the top line in Q2, with adjusted EPS up 53% YOY to $3.11. During the quarter, free cash flow reached $607 million, allowing the company to pay down $500 million of debt and repay $154 million to shareholders in dividends.

For Q3, management expects data center demand to drive 34% growth in revenue and a 79% increase in adjusted earnings. Analysts forecast earnings to increase by 61% in fiscal 2026, followed by 52% growth in fiscal 2027. For the level of growth expected, STX stock appears to be an undervalued play. Given its strong demand visibility, advancing technology leadership in HAMR, expanding margins, and disciplined capital allocation, it’s no surprise that Seagate has become a market darling.

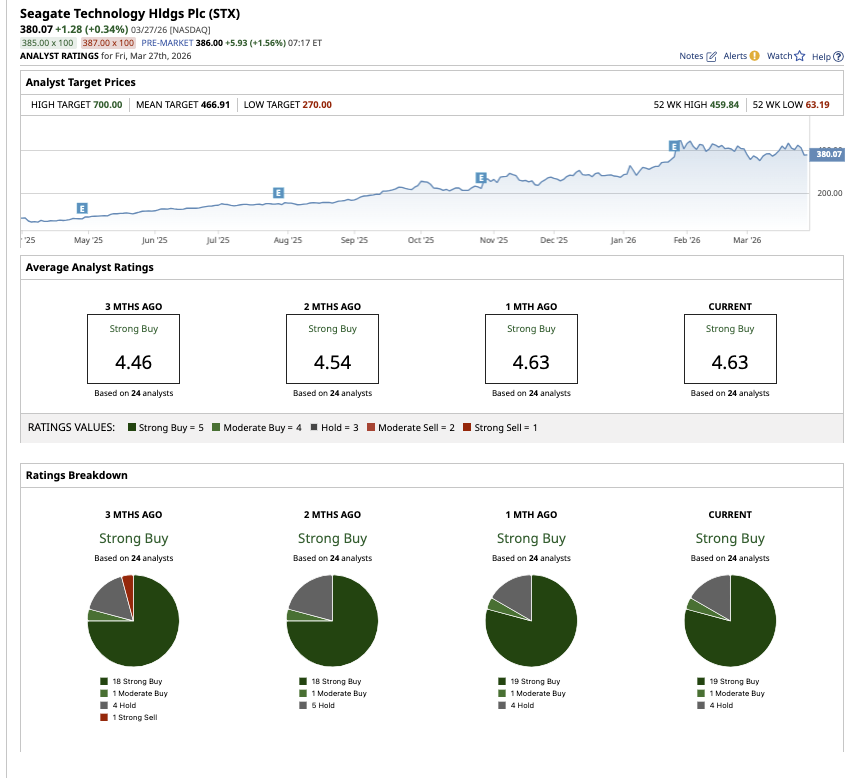

Overall, the consensus on STX stock is a "Strong Buy" rating. Out of 24 analysts with coverage, 19 have a “Strong Buy,” one suggests a “Moderate Buy,” and four have a “Hold" rating. The average target price of $466.91 is 29% above current levels, while the high price estimate of $700 implies 93% potential upside.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)