While the broader markets sank on Friday, March 27, Peloton (PTON) rose nearly 9% and bucked the trend after Eric Jackson, founder of EMJ Capital, said that he is long on the stock at $4. For the uninitiated, Jackson was instrumental in fueling the rally in Opendoor Technologies (OPEN) last year. Jackson has set a base-case target price of $8 on PTON, while the bull-case target is $16.

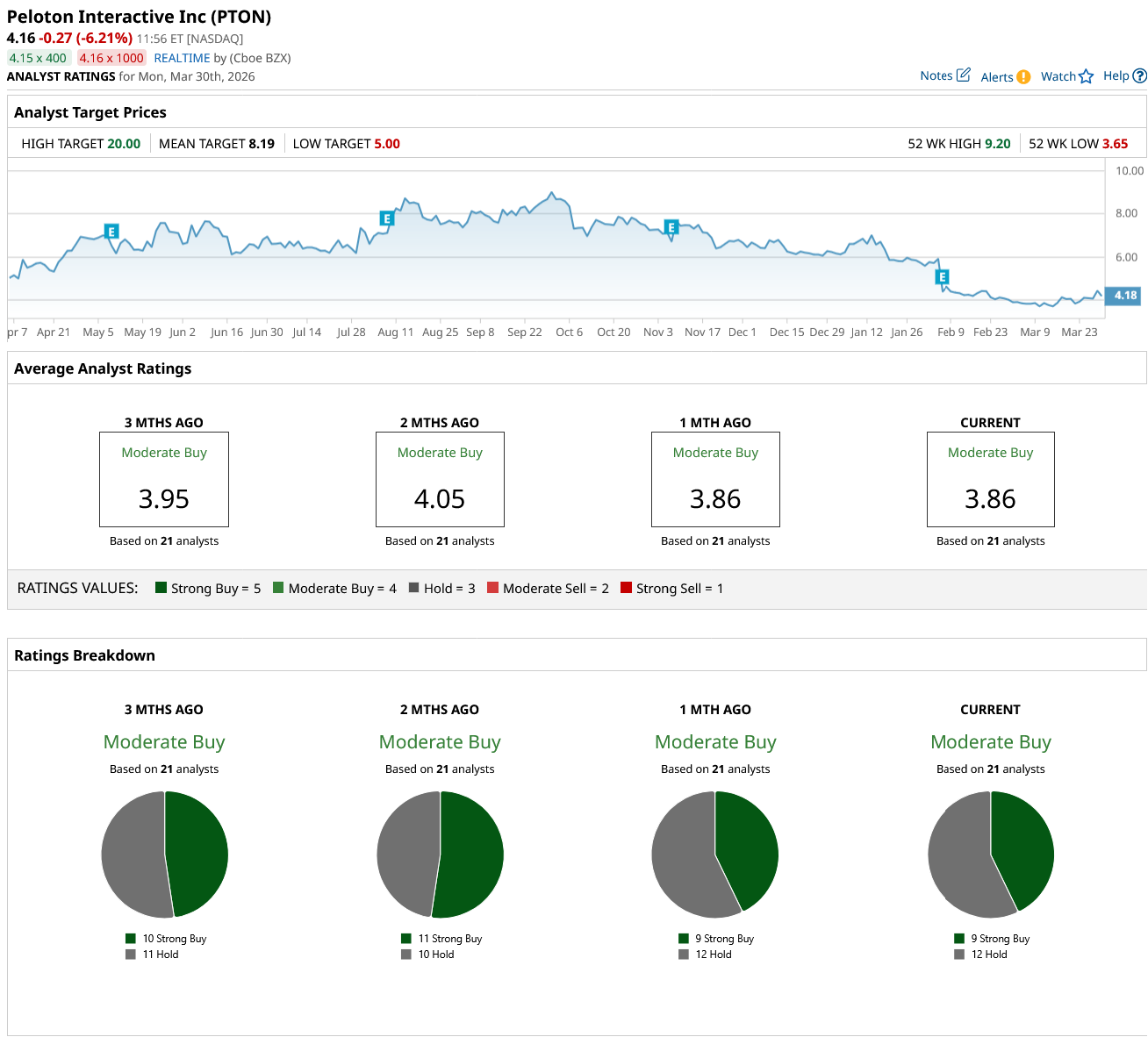

Notably, in February, hedge fund manager David Einhorn, who sold the bulk of his Peloton holdings last year, said that he is buying the dip in the stock. PTON has a consensus rating of “Moderate Buy” from the 21 analysts polled by Barchart, and its mean target price of $8.19 is similar to Jackson's base-case target. But could PTON stock rise above $8 in 2026? Let’s look at both the bearish and bullish arguments.

The Bearish Argument: What’s Been Pulling Down PTON Stock?

Far from reporting triple-digit revenue growth that helped its market capitalization top $50 billion at its peak, Peloton is now struggling to grow. The stay-at-home fitness industry has been on shaky ground ever since gyms reopened after the Covid-19 pandemic. Peloton’s subscription base and revenues have been falling, and in fiscal Q2 2026, its revenues fell 3% year-over-year (YoY) to $656.5 million. For context, in the corresponding period in fiscal year 2022, the company reported revenues of $1.13 billion. Its equipment sales have particularly sagged, and while subscription revenues have fared relatively better, they haven’t been able to offset the sharp decline in hardware sales.

Meanwhile, the subscription business has also been plagued by a decline in members. Peloton’s members fell to 5.8 million in the most recent quarter after having previously peaked at 7 million in fiscal Q3 2022. The paid connected fitness subscriber base has also been falling, with the churn rate rising to 1.9% in the most recent quarter.

The Bull Case for PTON Stock

It's not all doom for PTON, though, as while its topline has been shrinking, the company has made a remarkable turnaround on the bottom line and posted adjusted earnings before interest, tax, depreciation, and amortization (EBITDA) of $81 million in fiscal Q2 2026. Peloton expects its revenues to fall YoY in the current quarter but projects adjusted EBITDA to rise to between $120 million and $135 million, a YoY increase of 43% at the midpoint. It also raised its annual EBITDA guidance to between $450 million and $500 million.

While loss-making on the net profit level, Peloton is generating healthy cash flows and expects to generate at least $275 million in free cash flows this fiscal year despite a $45 million hit from tariffs. Peloton’s balance sheet is in much better shape, and the company has cut its net debt by over half in the last year, with the metric standing at $319 million at the end of January.

Peloton Is Working To Revive Growth and Turn Profitable

Peloton has been on a cost-cutting spree, and apart from layoffs, it has rationalized its store footprint by shutting down some stores. The company has instead been focusing on smaller micro stores, which it said are driving 8x the sales of the legacy stores on a per square foot basis. The management is optimistic about achieving positive operating income this fiscal year, which would be a key milestone for the company.

Peloton’s Commercial business has been another glimmer of hope, and it reported a 10% increase in sales in the recent quarter. The company is now selling its hardware to gyms, or as CEO Peter Stern put it, “Peloton is going to the gym.”

That said, while Peloton previously took several steps to spur growth, many of the initiatives failed to have the desired impact. For instance, the pivot to third-party sales, including selling its products on Amazon (AMZN), hasn’t been the kind of growth driver that it was expected to be.

PTON Stock Forecast

I have been long on PTON stock and added to my positions this year to capitalize on the crash. The company has been working on profitability and has sacrificed topline growth in that pursuit.

The stock's valuations are quite reasonable, and it trades at a forward price-to-sales multiple below 1x. While we don’t have a price-to-earnings (P/E) multiple since Peloton is currently posting losses, the forward price-to-free cash flow multiple is in single digits, which looks attractive.

Bullish commentary from Jackson, who was behind the sharp rally in Opendoor stock last year, has helped buoy sentiments. While I usually refrain from participating in sentiment-driven rallies and meme stocks, I find Peloton attractive from a valuation perspective and would continue to hold my shares.

On the date of publication, Mohit Oberoi had a position in: PTON, AMZN. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)