The market has been obsessed with AI stocks, but with the ongoing U.S.-Iran war, energy and oil names have quietly taken the lead. Looking beyond the noise, the most durable investment opportunities are often companies with strong fundamentals, recurring revenue, and long-term industry tailwinds. At the same time, not every tech stock is a great long-term buy.

One stock stands out with years of growth ahead, while another looks significantly less appealing in the current market.

The Stock to Buy: Intuitive Surgical (ISRG)

Just 31 years in the business, and Intuitive Surgical (ISRG) has already dominated the robotic surgery market. At the heart of Intuitive’s success is its da Vinci robotic surgery ecosystem, which is constantly expanding its competitive moat.

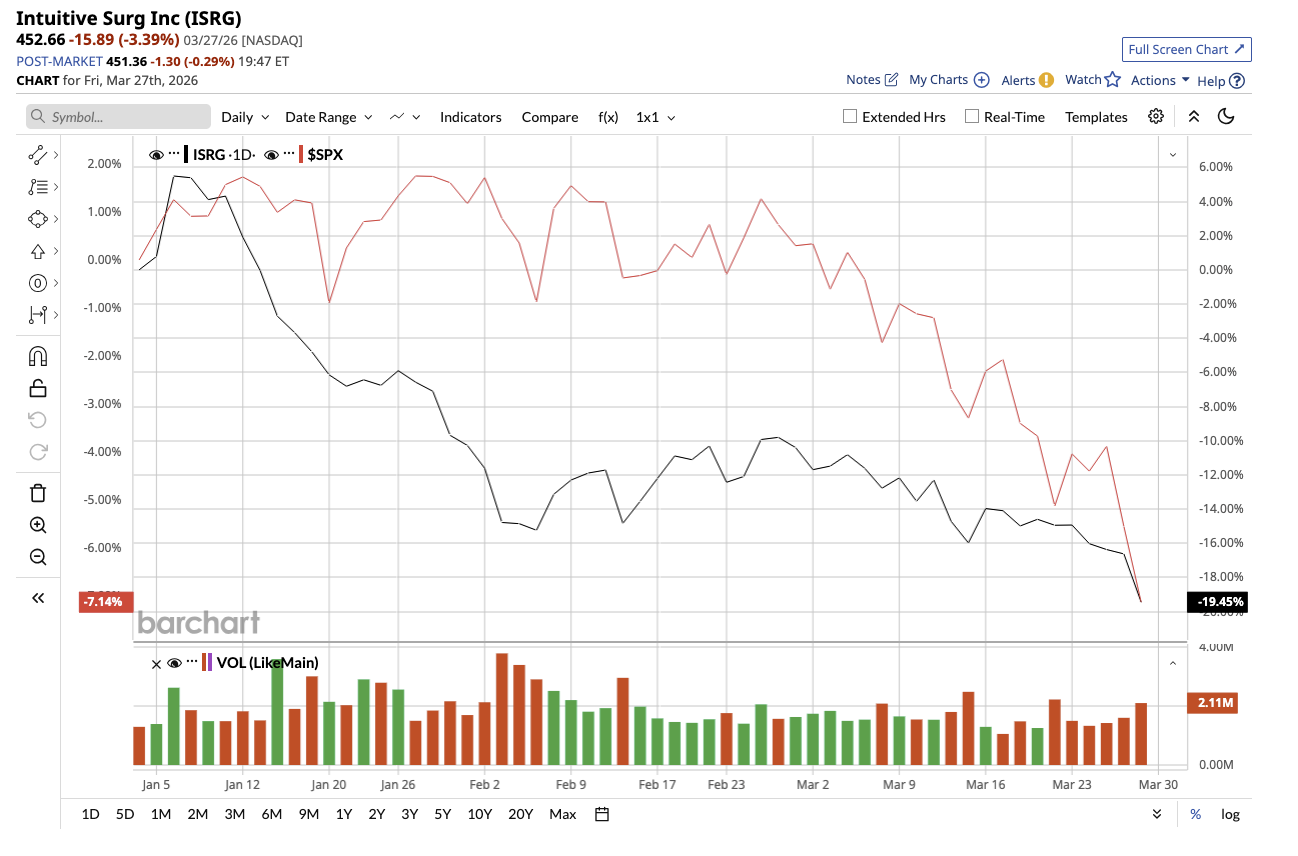

Valued at $160.7 billion, ISRG stock is down 19.5% so far this year, compared to the S&P 500 Index’s ($SPX) dip of 7.1%.

The da Vinci system is a robot-assisted surgical platform that allows doctors to perform minimally invasive surgeries (MIS) with greater precision, control, and minimal invasiveness. Complex procedures are done through tiny incisions instead of large open cuts. This leads to less pain and faster recovery for patients.

In 2025, Intuitive’s revenue climbed 21% year-over-year (YoY) to $10.06 billion, driven by a 19% increase in procedures across geographies, platforms, and specialties. Net income rose 22.6% for the full year. The company now has 11,106 da Vinci surgical systems installed in 2025, compared to 9,902 in 2024. Notably, over 3.1 million procedures were performed using Intuitive systems in 2025, bringing the company’s lifetime total to 20 million.

Besides the sale of the systems, the company also sells instruments, accessories, and services tied to procedures, leading to a recurring revenue stream. In Q4 alone, recurring revenue made up 81% of overall revenue. As procedure volume increases, so does high-margin recurring revenue. The newly launched da Vinci 5 will be driving the company’s next growth cycle. Management emphasized that surgeons are impressed by its increased efficiency, improved visualization, and force feedback capabilities. These updates will have a direct influence on surgical results and workflow efficiency, resulting in higher utilization. Management expects da Vinci procedures to grow by 13% to 15% in 2026, driven by general surgery in the U.S. and expanding use cases internationally.

Hospitals are also upgrading existing systems, which means sustained revenue growth for years for the company. This is one of the main reasons why Intuitive has a competitive advantage. Hospitals spend a lot of money on buying these systems and training surgeons on them. So, each time a new system is installed, a long-term relationship is built. The high switching costs keep Intuitive's revenue safe even if a cheaper product comes into the market. There are still risks to watch, including macroeconomic pressures in Europe, competitive dynamics in China, and potential policy changes in the U.S. healthcare system.

Even after three decades of innovation, the minimally invasive robotic surgery market is still in its early innings. That leaves a long runway for growth for 2026 and beyond. With a recurring revenue model, expanding global footprint, and continuous innovation pipeline, it offers a rare combination of stability and growth. At the current dip, ISRG stock makes for a strong candidate for investors seeking durable growth over the next decade.

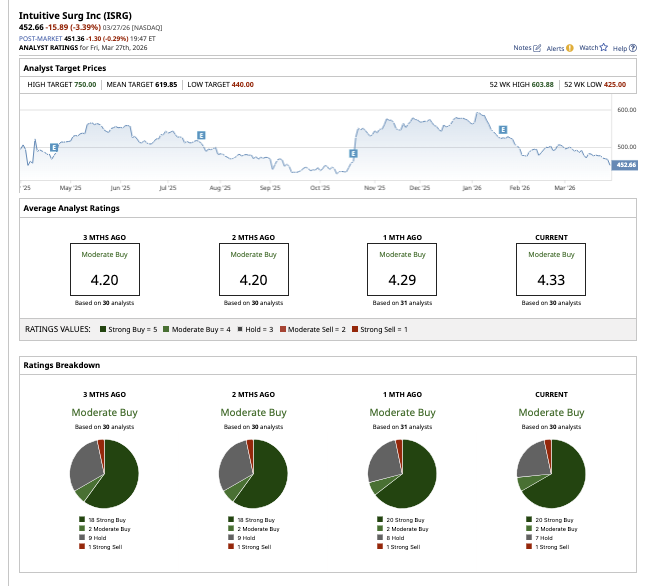

Overall, the consensus on ISRG stock is a consensus “Moderate Buy.” Out of the 30 analysts who cover the stock, 20 rate it a “Strong Buy,” two suggest a “Moderate Buy,” seven rate it a “Hold,” and one says it is a “Strong Sell.” The average target price of $619.85 is 37% above current levels. The high price estimate of $750 implies 65.7% upside over the next 12 months.

The Stock to Stay Away From: DocuSign (DOCU)

DocuSign (DOCU) became a pandemic-era darling as e-signatures and online agreement solutions had to replace paper processes. It made transactions faster, more secure, and more efficient. However, in recent years, its core business of electronic signatures has matured significantly, and growth is no longer as compelling as it was during the pandemic.

Valued at $8.9 billion, DOCU stock is down 32% YTD, compared to the broader market dip. It has also sunk 51% from its 52-week high.

While its fundamentals are stable, it is no longer in a high-growth phase. In fiscal 2026, revenue increased 8% YoY to $3.2 billion, while adjusted earnings rose 8% to $3.8 per share. Management expects similar growth levels in fiscal 2027. Additionally, annual recurring revenue (ARR) rose 8% to roughly $3.3 billion, maintaining the same pace as the previous year. DocuSign’s growth trajectory remains largely unchanged even with new product initiatives and AI integration.

DocuSign has been aggressively pushing its new AI-native system, Intelligent Agreement Management (IAM). IAM helps manage agreements across organizations, connecting workflows between departments and extracting insights from contract data. It reached over $350 million in ARR within just 18 months and now accounts for around 11% of total ARR. The company expects it to grow to around 18% in fiscal 2027. Even then, IAM accounts for a relatively tiny fraction of the entire business.

DocuSign generates strong cash flow, maintains high margins, and continues to serve a large global customer base. Its balance sheet is healthy, with over $1 billion in cash and no debt. However, most of the business is mature, and growth remains modest. With slowing growth, DocuSign faces a more challenging path. It may not be the kind of stock that outperforms in the years ahead, and therefore investors should steer clear of it.

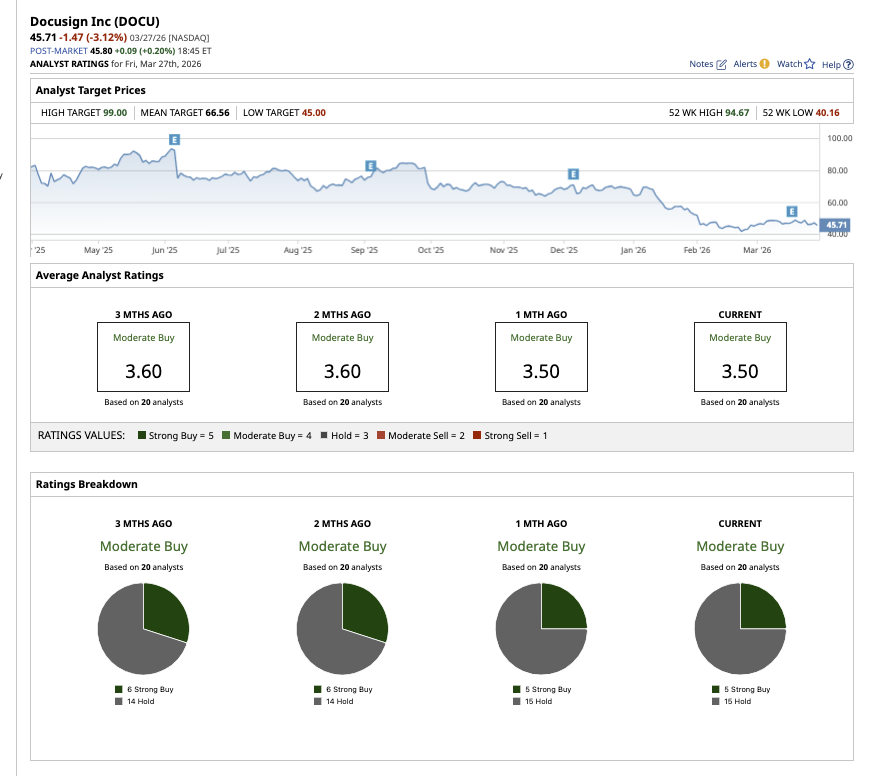

Overall, Wall Street rates DOCU stock as a consensus “Moderate Buy.” Out of the 20 analysts covering the stock, five rate it a “Strong Buy,” and 15 rate it a “Hold.” Based on its average target price of $66.56, the stock has upside potential of 46% from current levels. Plus, its high price estimate of $99 suggests the stock could rally as much as 116.6% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)