The market has taken a surprising turn in 2026. After dominating headlines for nearly two years, AI stocks are beginning to show signs of fatigue. Meanwhile, escalating conflict in Iran and supply disruptions across the Strait of Hormuz have pushed oil prices higher, tightening global markets and boosting profitability for producers.

One small-cap energy company, Kosmos Energy (KOS), has emerged as an unlikely winner in this scenario. KOS stock has gained a staggering 215% year-to-date (YTD), without any connection to the AI boom and outperforming the broader market.

A Transitional 2025 That Set the Stage for a Breakout

While investors grow wary of AI stocks due to stretched valuations and aggressive capital spending, energy stocks have taken the lead. The energy sector, as tracked by the Energy Select Sector SPDR ETF (XLE), is up 40% so far this year. Valued at $1.7 billion, Kosmos Energy is a small-cap, independent oil and gas exploration and production company. It finds, develops, and produces oil and natural gas, then sells it in global energy markets.

Kosmos has a strong presence in:

- Ghana-Jubilee and the Tweneboa, Enyenra, and Ntomme (TEN) oil fields (its major production assets)

- Mauritania & Senegal-GTA LNG project (a large offshore gas development)

- U.S. Gulf of Mexico—its offshore oil projects

Since it is a pure-play upstream energy company, its earnings are heavily tied to oil and gas prices. Kosmos entered 2026 after what management called a “challenging transitional year” in 2025. It laid all the critical groundwork for a lower-cost and more sustainable business model. It even secured long-term license extensions in Ghana through 2040. Total revenue declined to $276 million from $397 million in the year-ago quarter, with an adjusted net loss of $0.16 per share. Management noted that realized prices were lower in Q4 due to weaker commodity markets. However, now the company expects a rebound in Q1 2026 as prices move higher, indicating that strong earnings are related to oil prices.

Additionally, Kosmos is ramping up production across its key assets. Notably, Jubilee is already producing over 70,000 barrels per day, with new wells adding around 13,000 barrels per day, while GTA LNG output is running at roughly 2.9 million tons per annum. The company expects five additional wells to come online this year. Overall, the company is targeting 15% production growth in 2026, mostly from its core Jubilee and GTA assets. Higher prices along with rising volumes may boost revenue in the coming quarters.

Kosmos also holds a robust reserve base that supports long-term sustainability. The reserve stands at approximately 500 million barrels of oil equivalent in 2P reserves, representing around 20 years of reserve life, along with a 10-year 1P reserve life. This allows for continued conversion of resources into production. Beyond its core operations, the company is actively building a pipeline of future opportunities. In the Gulf of Mexico, it is advancing development projects and exploration initiatives in partnership with major industry players. These projects could provide meaningful upside potential as part of the company’s long-term strategy.

The Spotlight Is on Aggressive Cost Reduction and Balance Sheet Repair

Cost discipline and strengthening its balance sheet are the company’s top priorities now. In 2025, it reduced capital expenditures by nearly 70% to $290 million. The company expects to maintain similar levels in 2026 while also reducing over $100 million in operating costs in 2026. The sale of Equatorial Guinea assets could result in potential savings of approximately $250 million. Recently, it issued a $350 million bond to refinance near-term obligations, using the proceeds to repay existing debt and reduce exposure to its reserve-based lending facility. This year, the company plans to reduce net debt by at least 10%, supported by asset sales, free cash flow generation, and improved profitability.

Investors should note that Kosmos is a commodity-driven business, which is sensitive to changes in oil prices. However, the company manages this risk through hedging (locking in prices for future sales). It has hedged 8.5 million barrels of oil for 2026 and 2 million barrels for 2027, ensuring downside protection and greater earnings visibility. However, as a penny stock, it is not completely free of volatility.

Not Just Hype, but Strength in Fundamentals

Kosmos Energy’s 215% rally this year is not just based on hype but on measurable improvements such as higher production, lower costs, and a stronger balance sheet. For now, the current oil rally is very favorable for Kosmos. Higher prices also improve the effectiveness of its hedging strategy and speed up its goal of reducing net debt by at least 10% in 2026. If Kosmos continues to focus on growth and efficiency, there will be much more upside, as Wall Street anticipates.

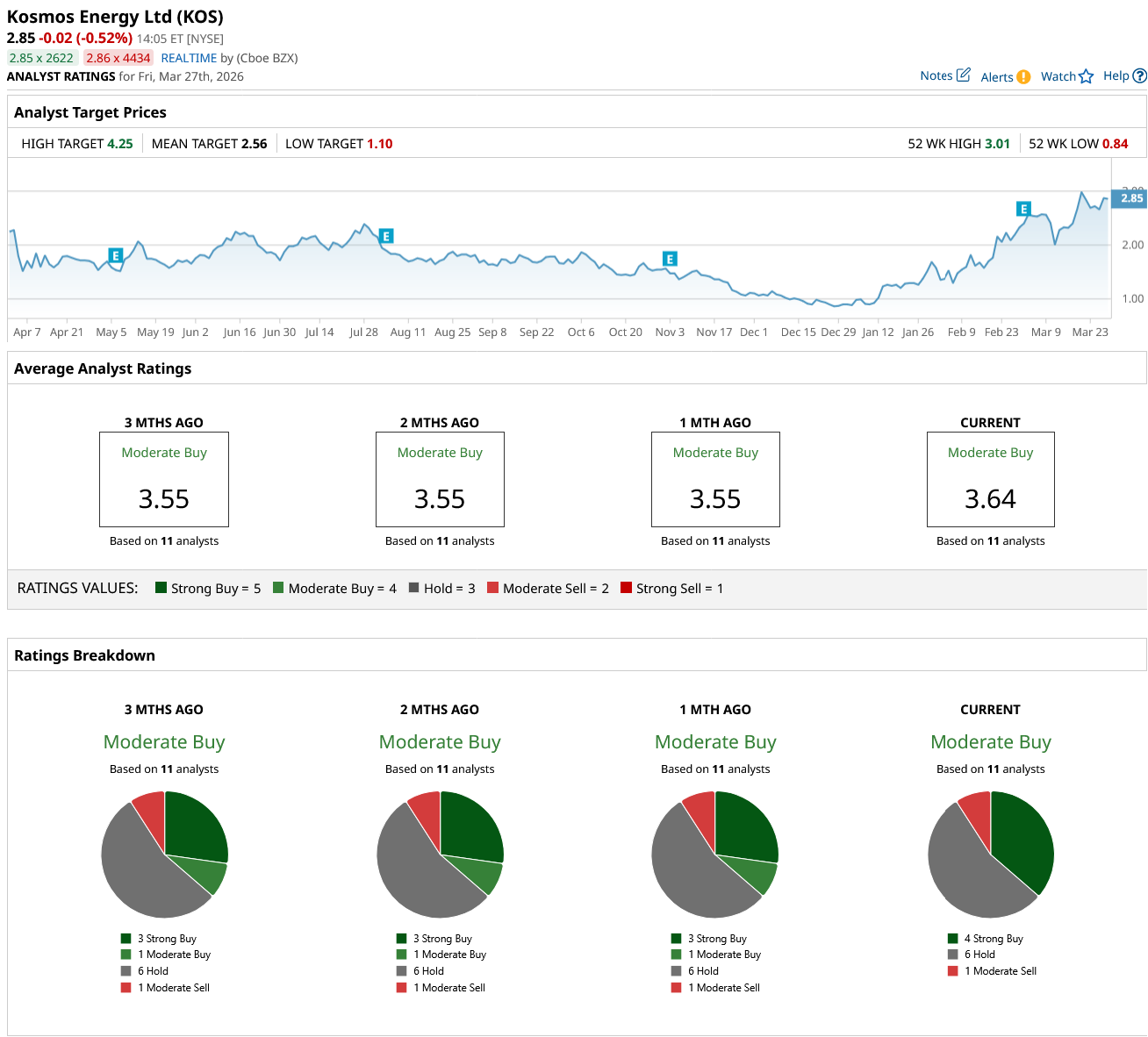

Analysts believe KOS stock can rally another 49% from current levels, based on its high price estimate of $4.25. Overall, the consensus on Kosmos stock is a “Moderate Buy.” Of the 11 analysts who cover the stock, four rate it a “Strong Buy,” six say it is a “Hold,” and one says it is a “Moderate Sell.”

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)