The global oil market has been thrown into turmoil as the ongoing U.S.-Iran war has disrupted the most critical supply route, the Strait of Hormuz, and damaged key energy infrastructure. Fears of prolonged supply shocks have sent crude prices to above $100 per barrel, marking one of the sharpest spikes in years. As a result, energy stocks have skyrocketed, with investors rushing to buy shares of companies that stand to benefit from elevated prices.

These three energy stocks seem best positioned to benefit from a prolonged oil shock.

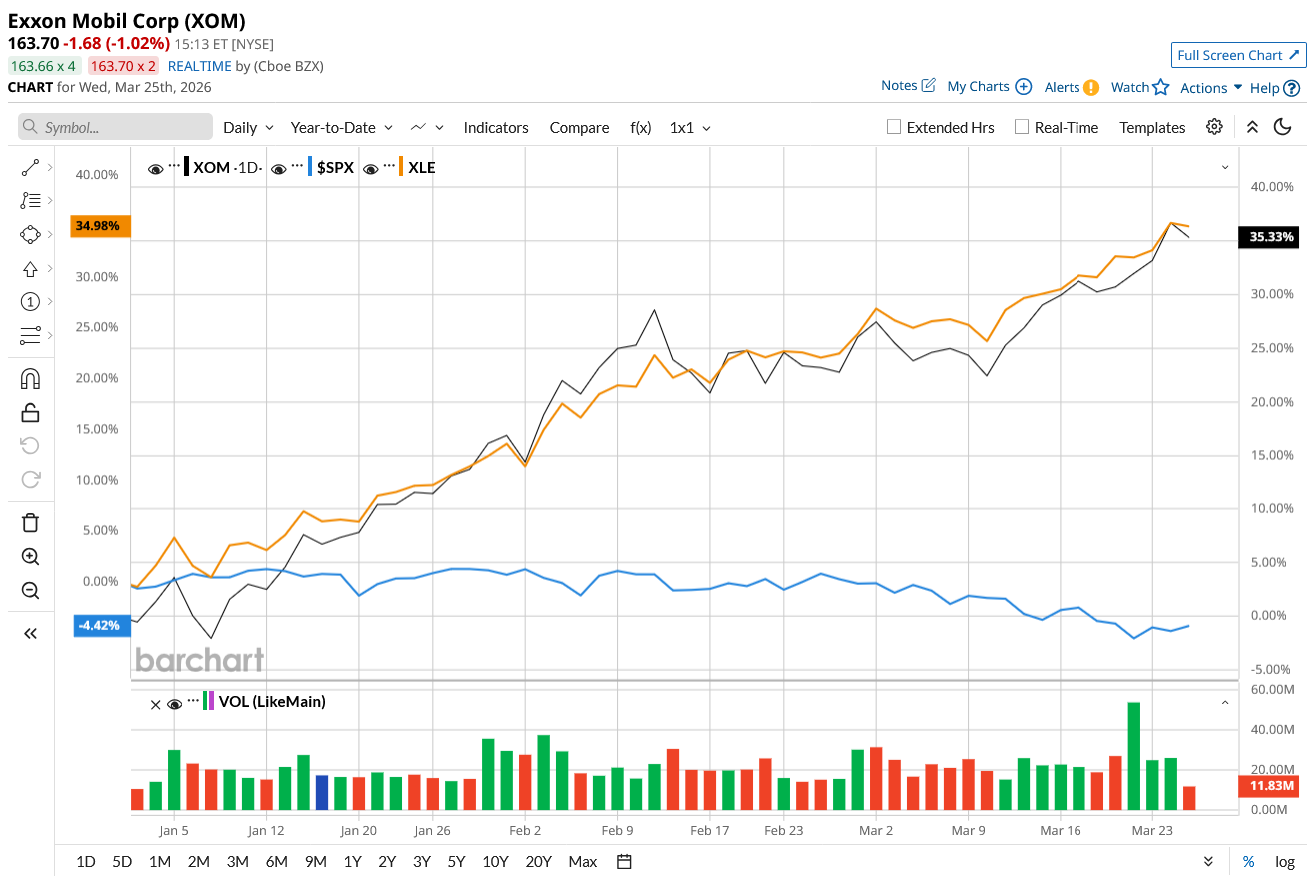

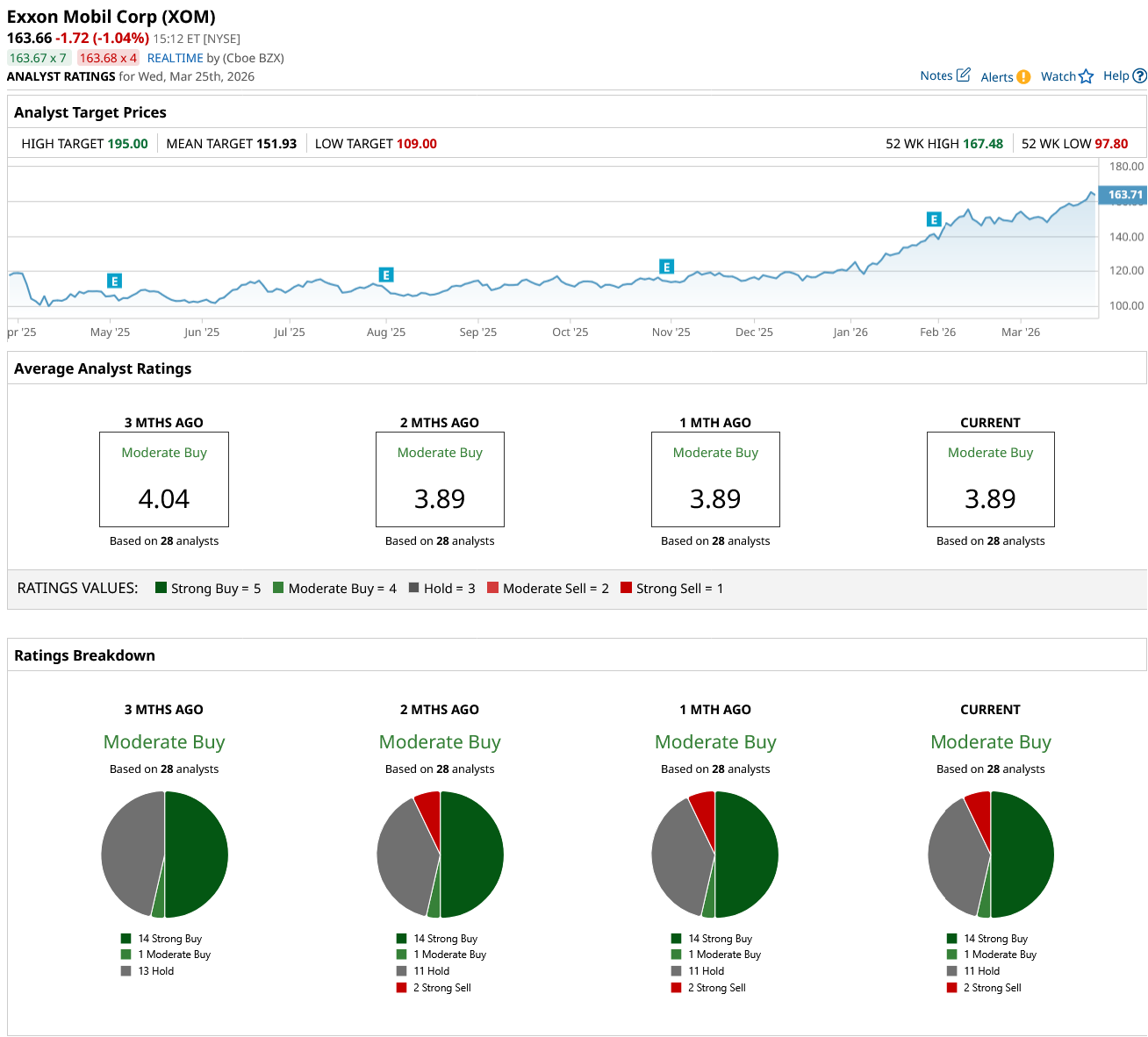

Energy Stock #1: Exxon Mobil (XOM)

Exxon Mobil (XOM) has emerged as one of the biggest beneficiaries of the recent oil spike, thanks to its massive global production footprint and integrated business model. Exxon shares have surged 36% year-to-date (YTD), outperforming the energy sector and the S&P 500 Index ($SPX), which has dipped 3.5%.

In fact, the energy sector, as tracked by the Energy Select Sector SPDR ETF (XLE), has already become one of the market’s top performers, gaining 33.3% so far in 2026.

Valued at $689.1 billion, Exxon is one of the world’s largest energy companies, operating across oil and gas production, refining, and chemicals. As crude prices rise, Exxon’s upstream operations generate strong profits, while refining and chemical businesses provide steady cash flow. This diversification makes Exxon more resilient during volatile periods, such as the current geopolitical crisis.

Furthermore, Exxon is a dividend stock. It offers a forward yield of 2.6% and has increased dividends for 43 consecutive years, earning the title of “Dividend Aristocrat.” With low breakeven costs, Exxon generates healthy cash flows and continues investing in future growth projects like LNG and offshore drilling, even when oil prices fall. This makes its business resilient beyond just short-term oil spikes. Backed by a strong balance sheet, with a cash balance of $10.7 billion and a debt-to-equity ratio of 0.13, it remains financially robust. Even if the war ends any time soon, Exxon remains a strong long-term investment due to its diversification, resilience, and reliable payouts.

Overall, analysts rate XOM stock a “Moderate Buy.” Exxon stock has surpassed its average target price of $151.93. But its highest target price of $195 suggests a potential 20% upside over the next 12 months.

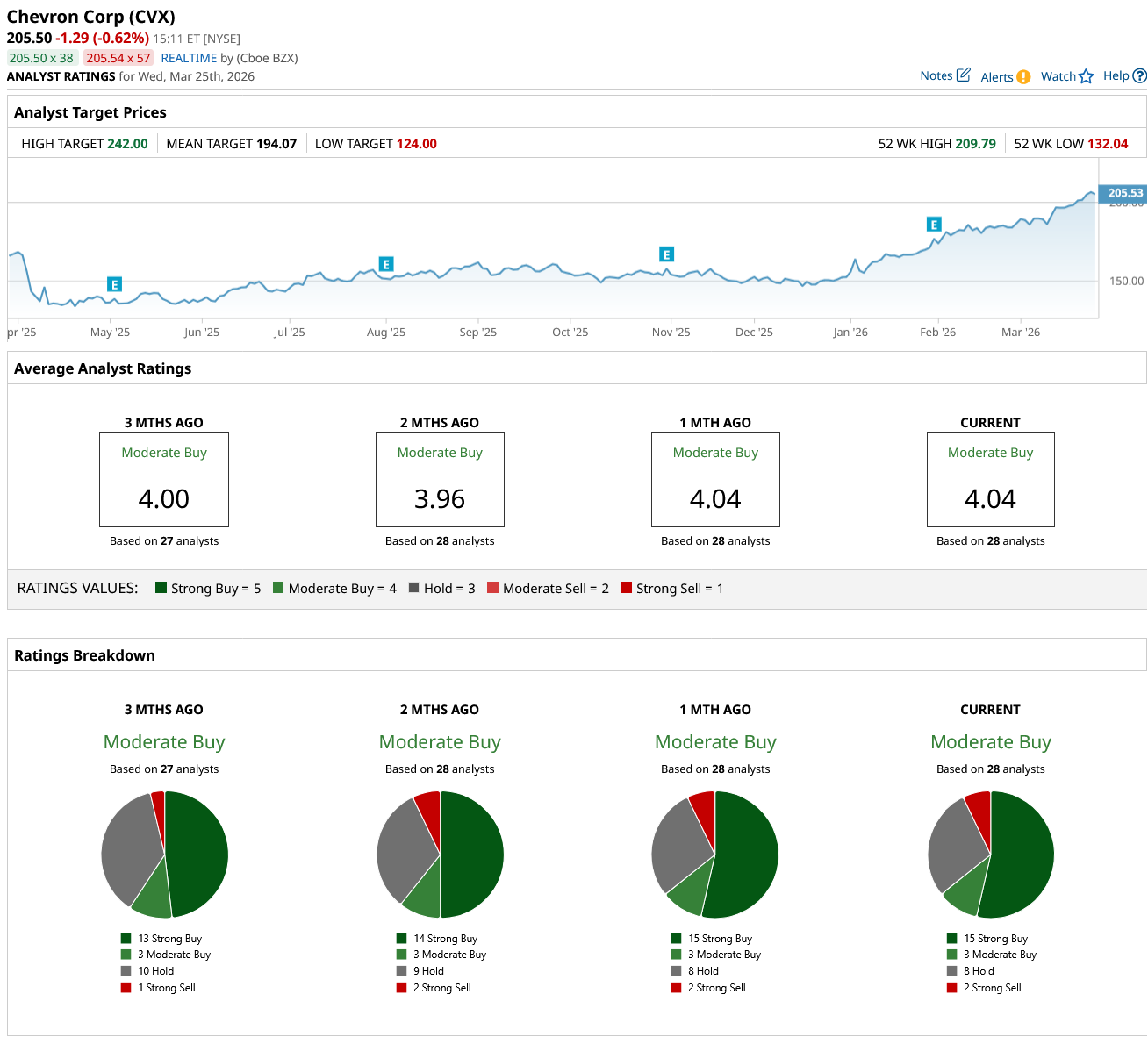

Energy Stock #2: Chevron (CVX)

Chevron (CVX) has also seen strong upside from the oil rally, benefiting from higher realized prices and steady production growth. Chevron shares are up 35% YTD, outpacing the overall market.

Valued at $412.6 billion, Chevron is a global energy company that explores, produces, refines, and sells oil and natural gas. Like Exxon, its diversified portfolio helps cushion earnings during downturns, making it a favorite among income-focused investors.

Chevron is also a Dividend Aristocrat, with a track record of 39 years of consecutive dividend hikes, even during weaker oil cycles. This makes it particularly attractive for investors looking for consistent income rather than just growth. It recently increased its dividend by 4% to $1.78 per share per quarter. It offers a forward yield of 3.5%. At the end of 2025, it had an adjusted free cash flow balance of $4.2 billion, cash and equivalents of $6.3 billion, and a debt-to-equity ratio of 0.21.

Backed by solid cash flows, a healthy balance sheet, and efficient operations, Chevron remains financially stable despite being slightly more sensitive to oil price swings than Exxon. Even in a post-war world, Chevron remains a reliable long-term investment due to its stability, strong cash flow, and consistent dividends.

On Wall Street, Chevron is rated a “Moderate Buy.” CVX stock is trading 6% above its average target price of $194.07. Its high price target of $242 points to a possible gain of 25% from current levels.

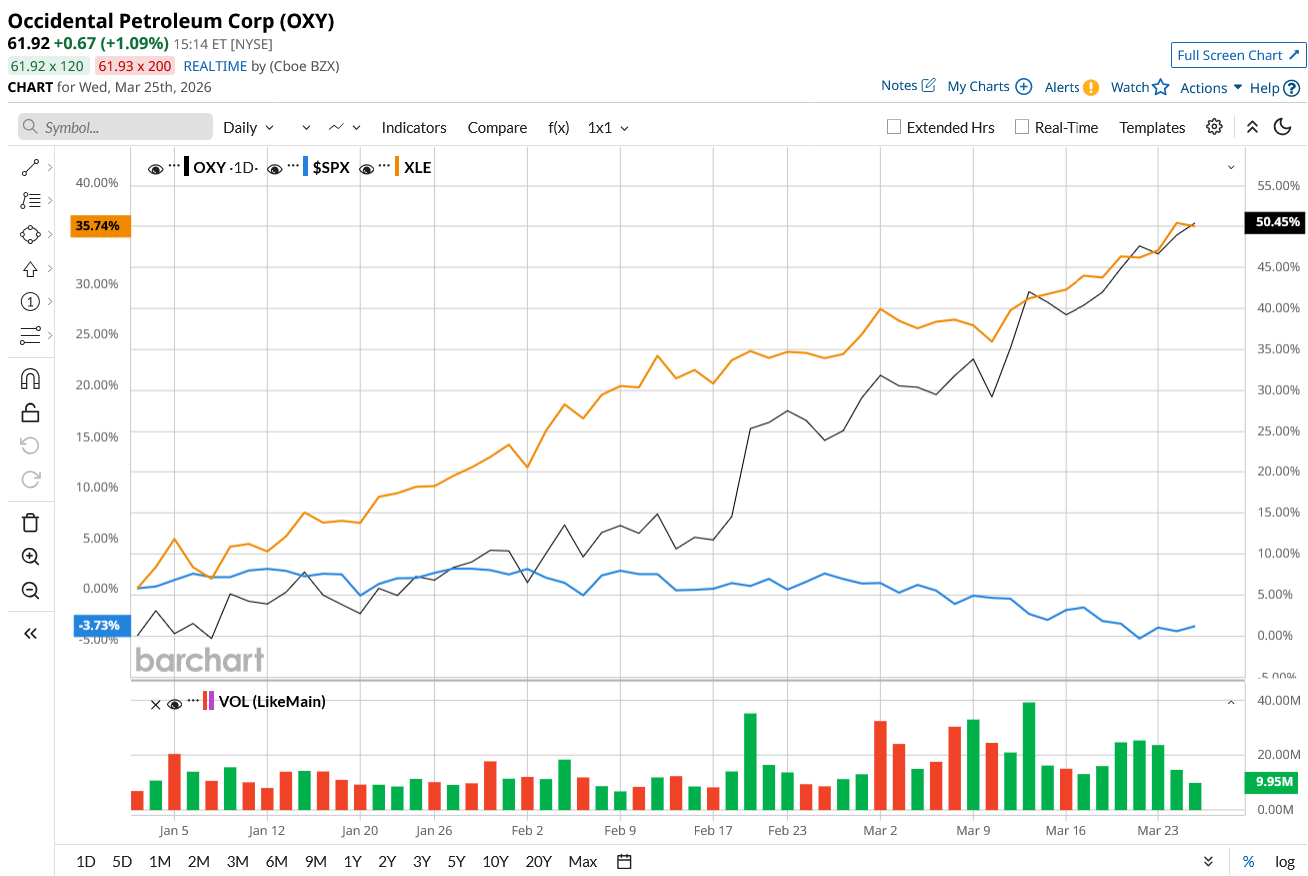

Energy Stock #3: Occidental Petroleum (OXY)

Occidental Petroleum (OXY) has been one of the biggest winners in the current oil rally, owing to its heavy exposure to upstream oil production. OXY stock has rallied 50% YTD, outperforming Exxon, Chevron, and the overall energy sector.

Valued at $60.7 billion, Occidental Petroleum is a pure-play oil and gas company. It mainly explores and produces crude oil and natural gas, with additional operations in carbon capture and low-carbon energy. In January, it sold its chemicals business (OxyChem) to Berkshire Hathaway (BRK.B) (BRK.A) for about $9.7 billion in order to focus on its main energy business. This helped to cut debt by $5.8 billion, bringing the total debt balance to $15 billion.

However, this lack of diversification means it now relies heavily on oil prices to drive profitability. This makes the stock more volatile, helping it soar during bull markets for oil while making it significantly riskier when prices fall.

Occidental also pays a dividend, yielding 1.7%. It isn’t a Dividend Aristocrat, as it has hiked its payouts for just six years in a row, including the most recent 8% increase in Q4. If oil falls after the war, Occidental is a weaker long-term investment compared to its peers.

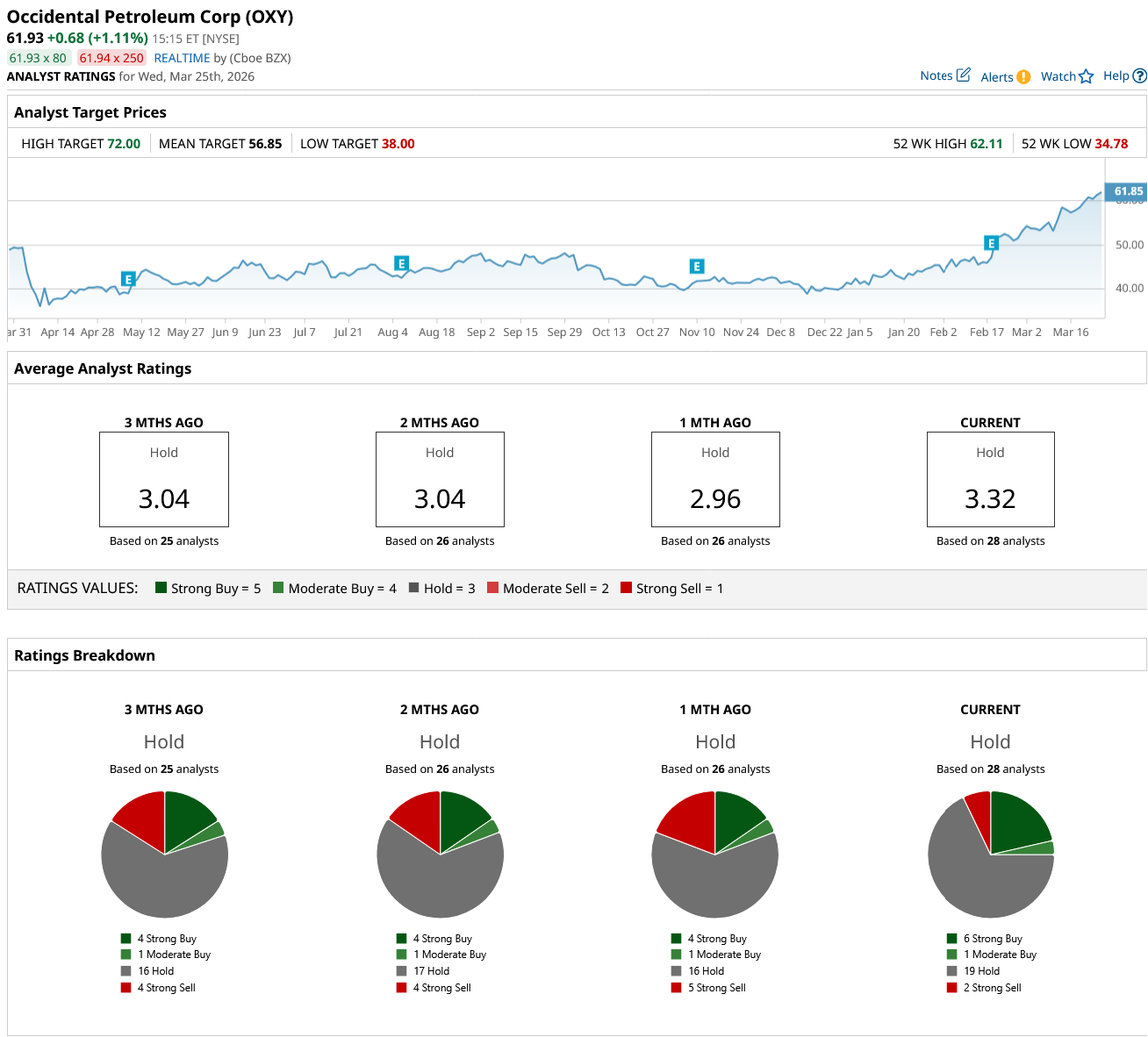

On Wall Street, Occidental Petroleum stock is rated a “Hold.” OXY stock is trading 8% above its average target price of $56.85. Its high price target of $72 points to a possible gain of 16% from current levels.

The Bottom Line

The current oil shock has created a powerful rally in energy stocks, but not all names are equally positioned for the long term. Exxon and Chevron offer stability and income, while Occidental Petroleum remains a high-risk, cycle-driven bet.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)