/Edwards%20Lifesciences%20Corp%20Irvine%2C%20Ca%20campus-by%20Steve%20Cukrov%20via%20Shutterstock.jpg)

Edwards Lifesciences Corporation (EW), headquartered in Irvine, California, provides products and technologies for structural heart disease and critical care monitoring. Valued at $48 billion by market cap, the company offers products such as tissue replacement heart valves, heart valve repair, hemodynamic monitoring devices, angioscopy equipment, oxygenators, and pharmaceuticals. The leading global structural heart innovation company is expected to announce its fiscal first-quarter earnings for 2026 in the near term.

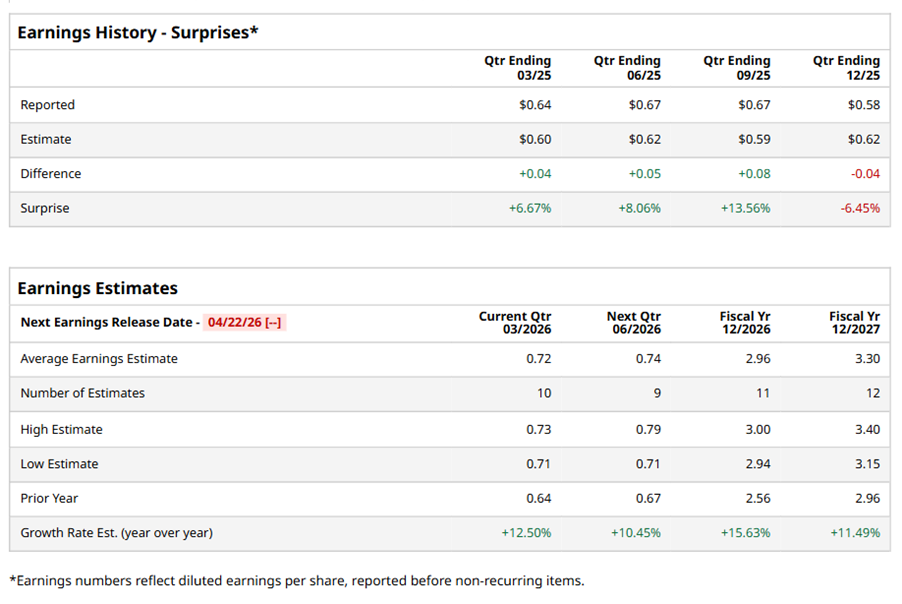

Ahead of the event, analysts expect EW to report a profit of $0.72 per share on a diluted basis, up 12.5% from $0.64 per share in the year-ago quarter. The company beat the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

For the full year, analysts expect EW to report EPS of $2.96, up 15.6% from $2.56 in fiscal 2025. Its EPS is expected to rise 11.5% year over year to $3.30 in fiscal 2027.

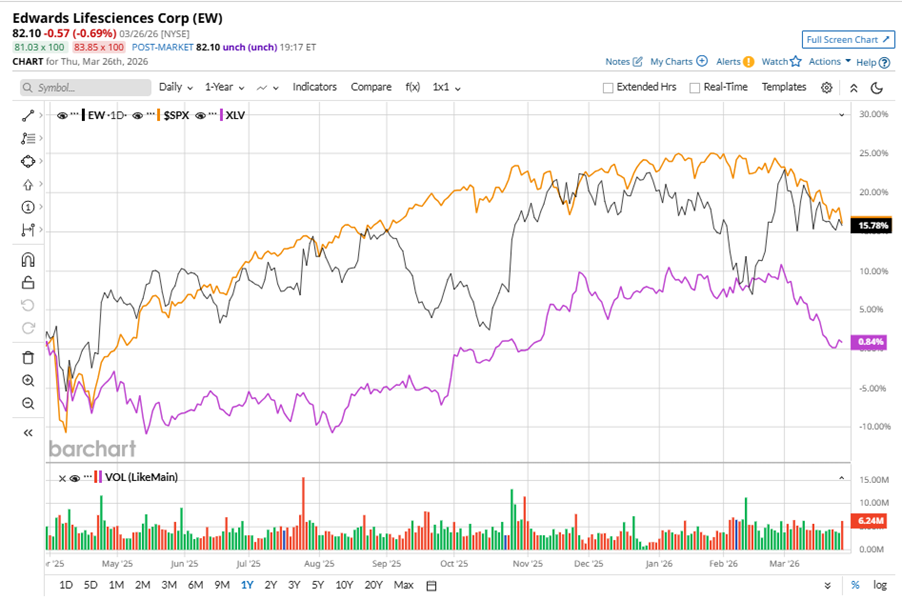

EW stock has outperformed the S&P 500 Index’s ($SPX) 13.4% gains over the past 52 weeks, with shares up 15.5% during this period. Similarly, it outperformed the State Street Health Care Select Sector SPDR ETF’s (XLV) marginal returns over the same time frame.

EW continues to outperform, driven by strong TAVR momentum and the success of its SAPIEN valve iterations. By advancing next-generation technologies like the SAPIEN M3 (the first transseptal mitral replacement), the company is strategically positioned to meet its $2 billion TMTT sales target by 2030. These innovations highlight how established healthcare firms can accelerate growth through "blockbuster" medical devices, making earnings periods essential for gaining management insights that extend beyond standard FDA approval notices.

Analysts’ consensus opinion on EW stock is moderately bullish, with a “Moderate Buy” rating overall. Out of 30 analysts covering the stock, 18 advise a “Strong Buy” rating, two suggest a “Moderate Buy,” and 10 give a “Hold.” EW's average analyst price target is $96.44, indicating a potential upside of 17.5% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)