/AI%20(artificial%20intelligence)/Image%20of%20server%20racks%20in%20modern%20server%20room%20data%20center%20by%20Sashkin%20via%20Shutterstock.jpg)

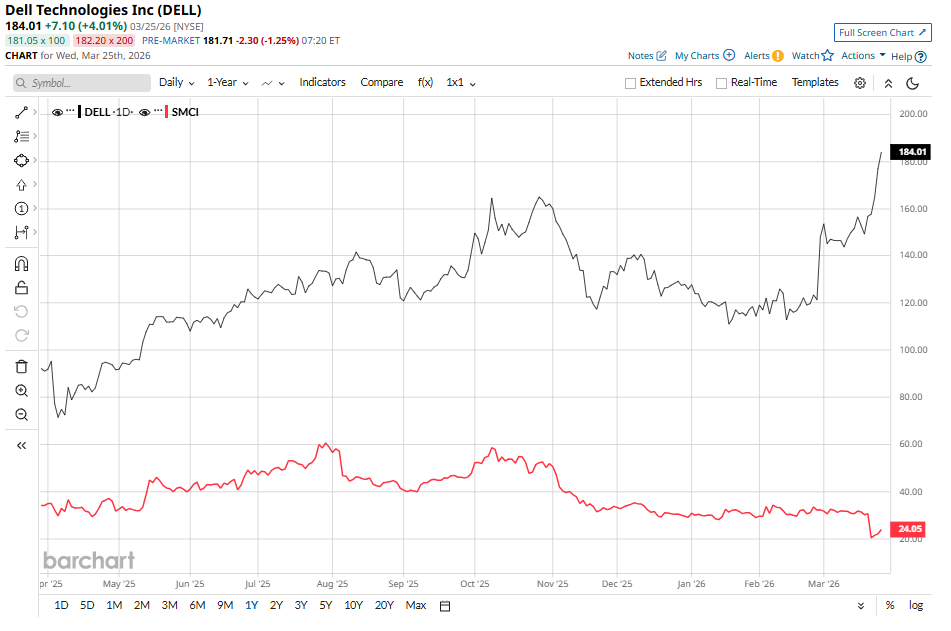

Super Micro Computer (SMCI) and Dell (DELL) are both benefiting from accelerating demand for artificial intelligence (AI) optimized servers, as enterprises increase investment in AI infrastructure. As organizations modernize data centers and invest in high-performance computing, these firms are capturing a growing share of a structurally expanding market.

However, Super Micro Computer, despite being well-positioned to benefit from rising AI infrastructure demand, has recently faced pressure. SMCI stock dropped significantly following legal action against individuals allegedly connected to the company in the unauthorized transfer of advanced AI hardware to China. This adds to regulatory scrutiny for the company, making the stock more volatile in the near term. As a result, investors may need to exercise caution when going long on SMCI stock.

By comparison, Dell Technologies appears to be executing well. It has translated AI demand into strong financial momentum, with substantial order volumes and a growing backlog that provides revenue visibility. Its ability to consistently convert demand into shipments reflects operational discipline, while its expanding AI pipeline signals continued growth potential.

In fiscal 2026, Dell reported $64.1 billion in AI orders. Moreover, it shipped $25.2 billion, and ended the year with a record $43 billion in AI backlog.

Dell is expanding its presence in the PC market while strengthening its Infrastructure Solutions Group (ISG), which includes AI-optimized servers, supported by solid margins in its traditional server and storage segments. At the same time, the company is well-positioned to capitalize on opportunities in the AI-driven future.

ISG to Propel Dell Higher

Dell’s ISG business continues to see solid operating momentum, which will drive its overall financial performance and support the share price. A key driver of strength within this segment is the accelerating demand for AI infrastructure. In the fourth quarter, Dell recorded $34.1 billion in AI orders, reflecting rapid adoption as enterprises scale AI deployments.

Dell shipped $9.5 billion worth of AI servers during the period and exited the quarter with a record backlog. This expanding backlog, alongside a growing pipeline, indicates strong growth ahead.

Customer diversification is also contributing to ISG’s growth trajectory. Dell’s customer base has surpassed 4,000, with expansion across neocloud providers, traditional enterprise clients, and sovereign entities. This broad-based adoption reflects the strength of Dell’s infrastructure offerings across multiple end markets.

Within ISG, its traditional server business is performing exceptionally well. Dell reported strong double-digit demand growth across all geographic regions, with momentum building throughout the period. Unit volumes increased alongside a larger active buyer base, while the product mix improved due to greater adoption of new-generation platforms.

Dell’s storage business is also contributing positively to overall performance, supported by strong demand for its proprietary IP portfolio. Profitability within the segment is improving and is likely to benefit from a higher mix of Dell’s proprietary solutions.

Is DELL Stock a Buy?

Thanks to the solid AI-driven demand and continued strength in its traditional server business, DELL stock has gained 40% year-to-date (YTD). Its solid backlog and compelling valuation suggest further upside potential.

Dell trades at approximately 14.9 times forward earnings, which is compelling given its strong growth outlook. Analysts project a 28% increase in earnings for fiscal 2027, followed by another year of double-digit expansion in fiscal 2028.

In addition, Dell is returning significant cash through share buybacks and dividends, which support its investment case. In fiscal 2026, it repurchased $7.5 billion worth of its own shares. Dell is also raising its annual dividend by 20% in fiscal 2027. The company further reinforced its commitment to shareholder returns by approving an additional $10 billion in share repurchase authorization.

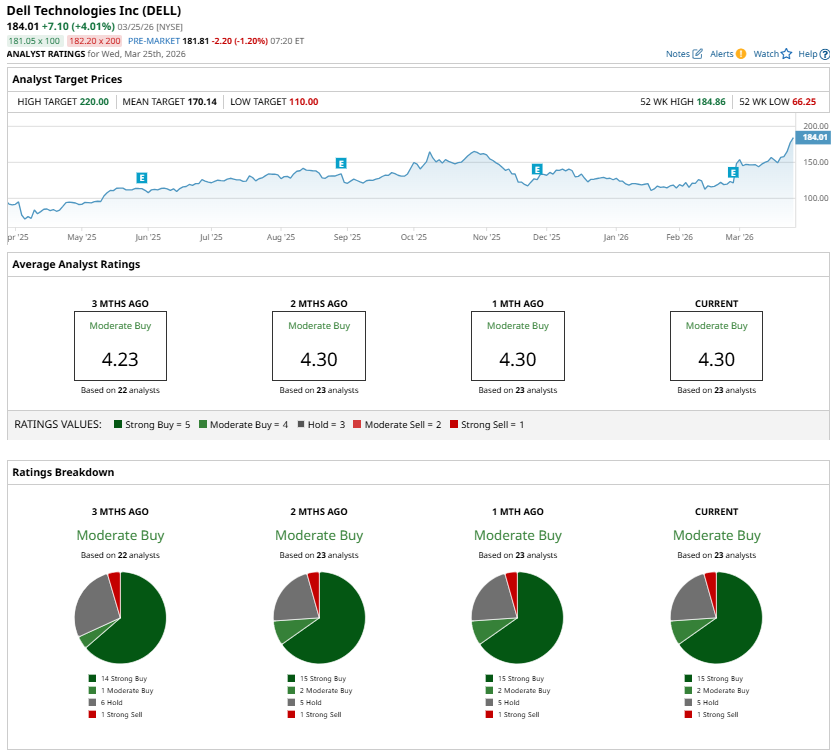

Analysts currently assign DELL stock a “Moderate Buy” consensus rating. In contrast, Super Micro Computer carries a “Hold” consensus rating on Wall Street, indicating a more cautious stance from analysts.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)