/Super%20Micro%20Computer%20Inc%20HQ%20photo-by%20Tada%20Images%20via%20Shutterstock.jpg)

Super Micro Computer (SMCI) stock has come under renewed pressure following legal developments involving individuals associated with the company. After a period of improving sentiment, the stock has declined sharply following charges filed by the Department of Justice (DOJ) against three people allegedly connected to the company for involvement in the illicit transfer of advanced artificial intelligence (AI) hardware to China.

The case centers on high-performance servers equipped with Nvidia (NVDA) chips, which are critical components of AI infrastructure. According to the indictment, the accused individuals engaged in efforts to circumvent U.S. export restrictions by using falsified documentation, staging equipment to mislead inspectors, and arranging complex shipment arrangements.

Those charged include Yih-Shyan “Wally” Liaw, a senior vice president of business development and board member; Ruei-Tsang “Steven” Chang, a Taiwan-based sales manager; and Ting-Wei “Willy” Sun, a contractor. In response, the company has placed the two employees on administrative leave and terminated its relationship with the contractor, effective immediately.

The situation reflects the broader geopolitical sensitivity surrounding advanced semiconductor and AI technologies. In recent years, the U.S. has implemented strict export controls to limit China’s access to powerful AI chips, aiming to maintain a technological advantage in the sector.

This is not the first instance of significant selling pressure on SMCI stock. Previously, shares declined sharply after Hindenburg Research published a report raising concerns about the company’s accounting practices and other operational issues. The situation was further exacerbated when the company delayed its annual filing, heightening investor uncertainty.

Time to Load Up SMCI Stock or Stay Away?

Although Super Micro has not been named as a defendant in the case, it introduces regulatory and reputational risks for the company. These developments may contribute to near-term stock volatility and create longer-term exposure to geopolitical and compliance-related challenges.

Operationally, however, the company continues to deliver exceptional results. In the second quarter of fiscal 2026, revenue surged to $12.68 billion, marking a 123% year-over-year (YoY) increase. This performance was driven by higher shipment volumes, including the clearing of previously delayed orders, as well as stronger pricing. The latter reflects a strategic shift toward higher-value offerings, particularly in advanced AI infrastructure.

Demand for AI GPU-based systems has accelerated sharply, especially for liquid-cooled and air-cooled servers. These premium systems boost revenue and strengthen Super Micro’s positioning in a rapidly evolving, high-performance computing market.

Looking ahead, management expects momentum to continue into the third fiscal quarter. Growth is anticipated to be supported by an expanded Datacenter Building Block Solution (DCBBS) portfolio, deeper engagement with enterprise and hyperscale customers, and ongoing investment in global manufacturing capacity.

The company has guided for at least $12.3 billion in Q3 revenue, a sharp increase from $4.6 billion a year earlier, and projects full-year revenue of at least $40 billion.

Despite this favorable revenue outlook, margin pressures remain a concern. Changes in the customer mix could weigh on pricing, while tariffs and the costs of expanding international manufacturing operations are likely to increase operating expenses. Additionally, ongoing supply constraints in key components, particularly memory and storage, continue to elevate input costs.

Although management anticipates a modest sequential improvement in gross margin, it still points to a YoY decline of around 300 basis points.

Taken together, while Super Micro’s growth trajectory remains compelling, the combination of margin headwinds, competitive pressures, and emerging regulatory uncertainties suggests a potentially volatile near-term outlook.

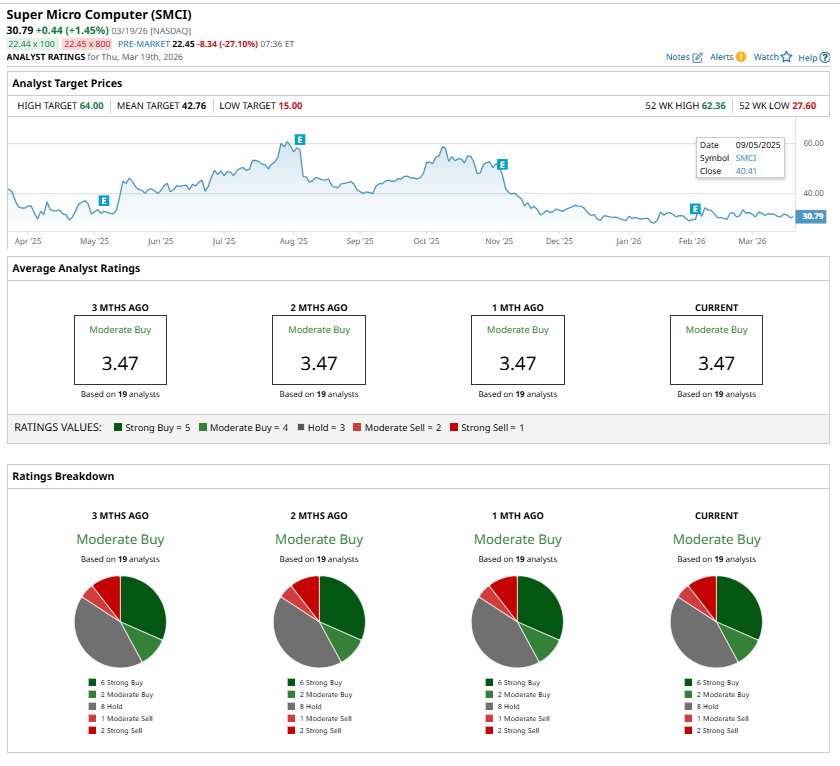

Although analysts currently maintain a “Moderate Buy” consensus rating on SMCI stock, evolving conditions could prompt revisions to their recommendations and estimates. Investors may therefore consider a cautious approach as the risk-reward balance continues to shift.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)