/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

The story on Wall Street has been artificial intelligence (AI), which has led to the unprecedented surge of some notable names. One such name is Advanced Micro Devices (AMD), which has earned its popularity through its CPUs and GPUs. Recently, the company has been focusing on forging longstanding partnerships, such as its supply agreement with OpenAI and the 6-gigawatt agreement to power the AI infrastructure of Meta Platforms (META).

The stock also got another lift this month when its prime competitor, Intel Corporation (INTC), reported its earnings that showed solid demand for CPUs. Against this backdrop, UBS analyst Timothy Acuri raised AMD's price target from $310 to a new Street-high $455 while maintaining a bullish “Buy” rating. Should you consider buying AMD now?

What Is Going On With AMD Stock?

Headquartered in Santa Clara, California, Advanced Micro Devices is a leading semiconductor company that designs high-performance CPUs, GPUs, and adaptive computing solutions powering data centers, PCs, gaming, and AI applications worldwide. AMD's innovations, from Ryzen processors to Instinct accelerators, drive breakthroughs in computing efficiency and compete fiercely with Intel in the chip market. The company has a market capitalization of $526.94 billion.

AMD holds a strong position in the AI space as a key challenger to Nvidia (NVDA), offering high-performance Instinct MI300X/MI325X GPUs optimized for large language models and data center inference. Its open-source ROCm software stack enhances developer accessibility.

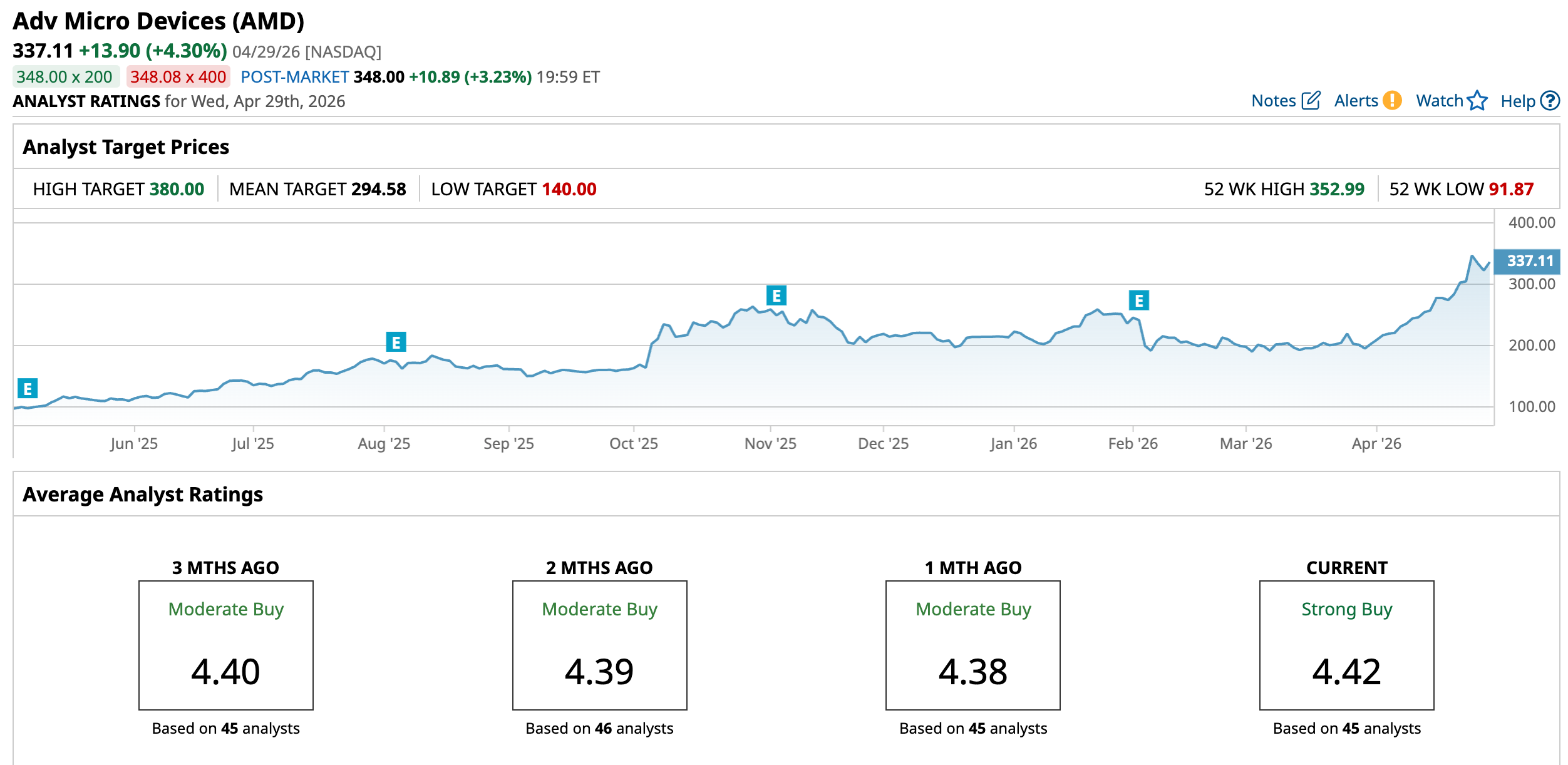

AMD’s stock surged 250.94% over the past 52 weeks on explosive AI GPU demand, deals with OpenAI and Oracle (ORCL), and data center revenue surging to power hyperscale training. The stock is also up 57.41% year-to-date (YTD). It reached a 52-week high of $352.99 on April 24, but is down 4.5% from that level.

AMD’s 14-day RSI of 76.15 is currently in overbought territory, which also indicates a solid momentum in the stock. On a forward-adjusted basis, its price-to-earnings (non-GAAP) ratio of 47.99 times is higher than the industry average of 23.21 times.

AMD Posted Record 2025 Revenue on AI Data Center Boom

Last year, AMD reported a record revenue of $34.64 billion, up 34% year-over-year (YOY). The company highlighted strong demand for its high-performance and AI platforms, as it entered 2026 with rising adoption of its high-performance EPYC and Ryzen CPUs while scaling its data center AI franchise.

In fact, the data center segment’s revenue for 2025 increased 32% YOY to a record $16.60 billion, indicating growth across both EPYC CPUs and AMD Instinct GPUs.

AMD’s non-GAAP operating margin declined from 24% in 2024 to 22% in 2025. However, the 2025 results included approximately $440 million in net inventory and related charges due to the U.S. Government's export controls on AMD Instinct MI308 data center GPU products. Non-GAAP EPS of $4.17 reflects a 26% YOY upsurge.

AMD’s fourth-quarter revenue was a record $10.27 billion, underscoring a 34% growth from the prior-year period. This was also higher than the $9.69 billion that Wall Street analysts had expected. Moreover, its quarterly non-GAAP EPS of $1.53 shows a 40% YOY growth, ahead of the $1.32 that analysts had expected.

Wall Street analysts are robustly optimistic about AMD’s future earnings. They expect the company’s EPS to climb by 35.9% YOY to $1.06 for Q1 2026 (to be reported on May 5, after the market closes). For fiscal 2026, EPS is projected to surge 78% annually to $5.82, followed by 60% growth to $9.31 in fiscal 2027.

Here’s What Analysts Think About AMD’s Stock

Interestingly, there have been some very differing opinions on AMD recently. After 11 years of a bullish stance, analysts at Northland Capital Markets downgraded AMD from “Outperform” to “Market Perform” and set a $260 price target. Analysts at the firm believe that while AMD is a great company, the “CY27 consensus is likely too high,” with Intel closing the gap and Nvidia continuing to consolidate its position in AI infrastructure.

DA Davidson analysts don’t agree with this position, as they upgraded the stock from “Neutral” to “Buy,” and raised the price target from $220 to $375. Analysts at the firm cited a structural increase in CPU demand and the possibility that AMD could play a larger role in data center expansion. DA Davidson sees the company primed to raise prices across its portfolio to support margins amid demand outpacing supply.

Stifel raised AMD’s price target from $280 to $320, while maintaining a bullish “Buy” rating, citing multi-gigawatt strategic commitments from Meta and OpenAI as factors supporting AMD’s outlook.

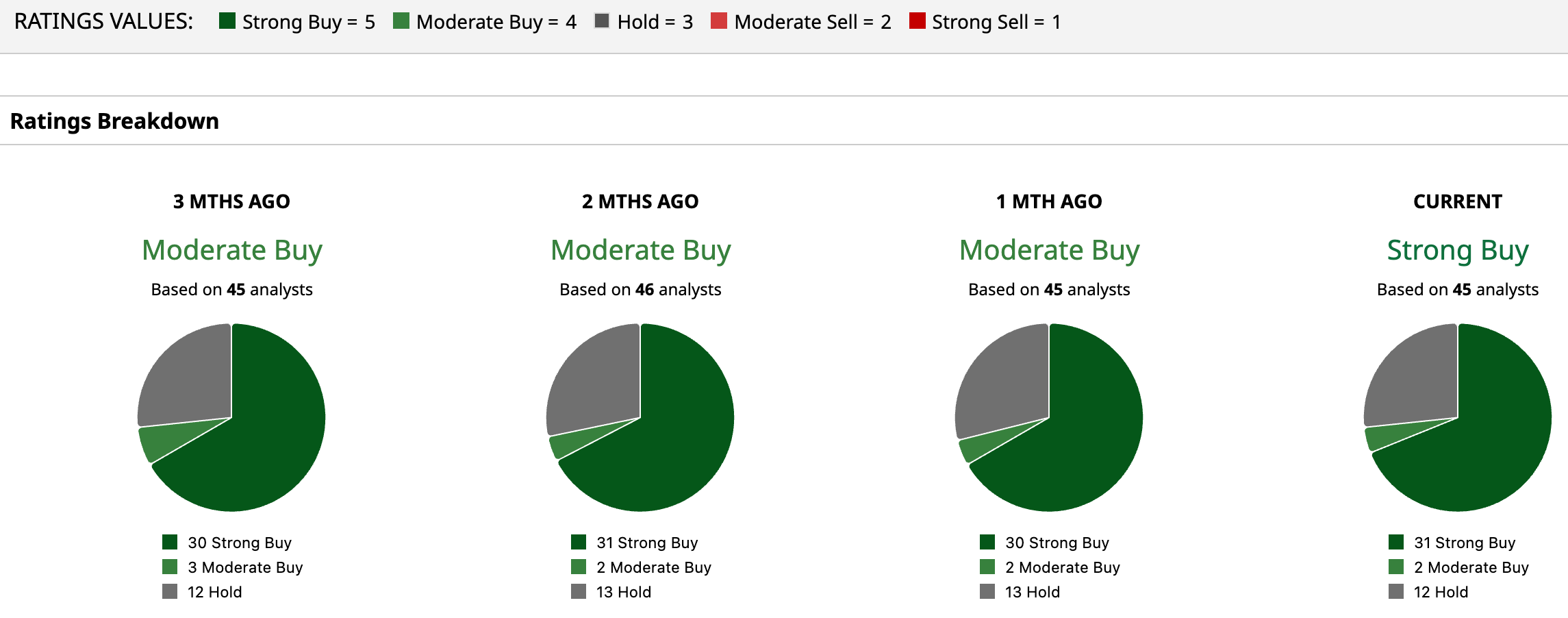

Chip giant AMD is an extremely popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 45 analysts rating the stock, a majority of 31 analysts have given it a “Strong Buy” rating, two analysts rated it “Moderate Buy,” while 12 analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $294.58 represents an 12.62% downside from current levels.

Key Takeaways

AMD is well on its way to consolidate its market share, and Intel’s blockbuster earnings report has also raised investor optimism surrounding the CPU-making giant. Therefore, while the UBS-given $455 price target implies a 35% upside from current levels, AMD might be a “Buy” prior to its Q1 earnings report.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)