/AI%20(artificial%20intelligence)/AI%20by%20TierneyMJ%20via%20Shutterstock.jpg)

Super Micro Computer (SMCI) is in a downward spiral. The server maker's stock tumbled 33% in a single session last Friday after a federal indictment named three individuals tied to the company in an alleged scheme to smuggle artificial intelligence chips to China. Now, Wall Street is reassessing how much the stock is worth, and the answers aren't pretty.

The question for investors sitting on losses or eyeing a potential bargain is whether the selloff has gone too far. Or is there more pain ahead?

Wall Street Is Nervous About SMCI Stock

Super Micro makes high-performance server systems used across cloud computing, data centers, and AI workloads. It's been a direct beneficiary of the AI infrastructure buildout, posting record revenue of $12.7 billion in its fiscal second quarter of 2026, a 123% year-over-year (YoY) jump.

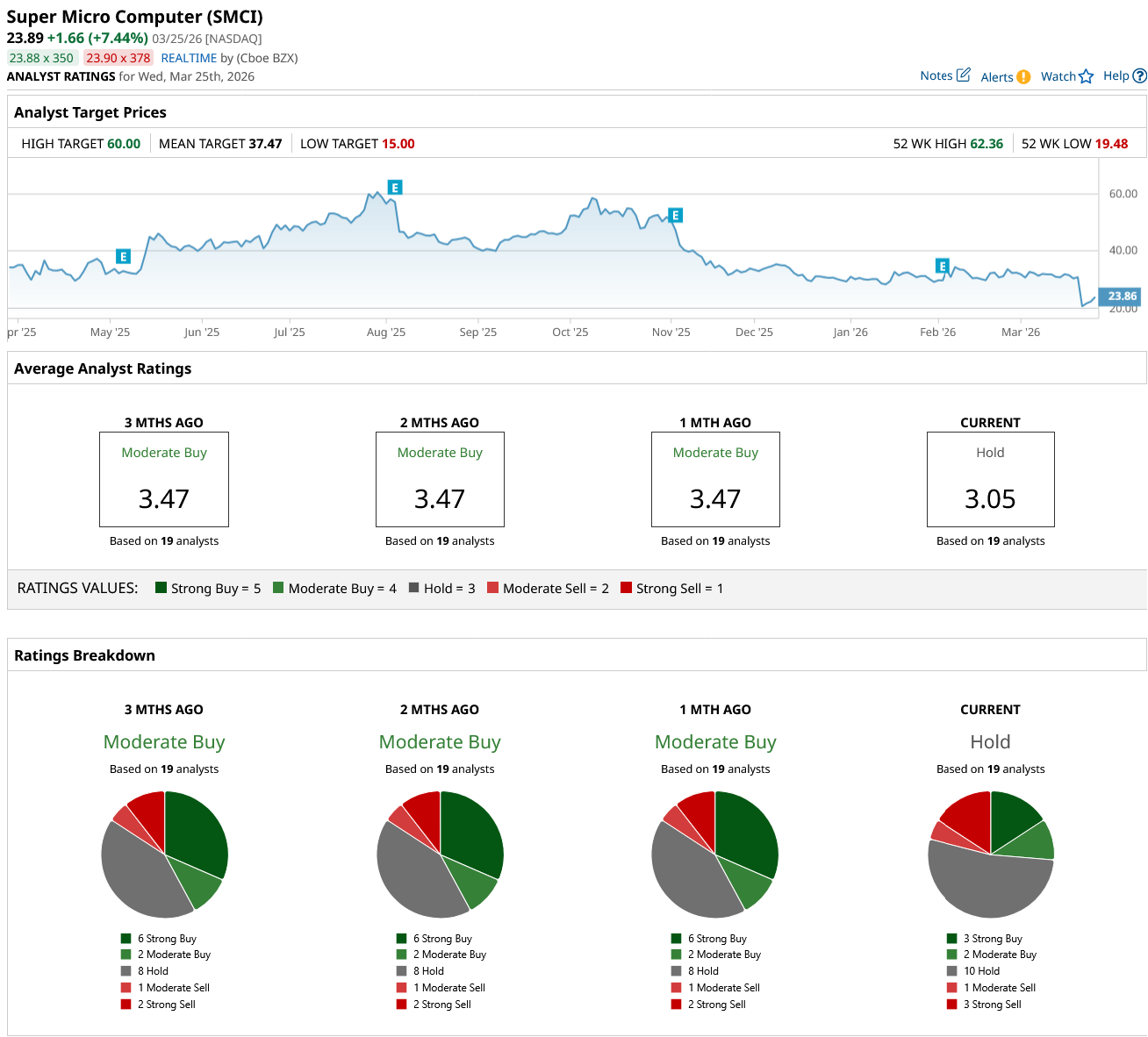

That kind of growth would normally have analysts falling over themselves to raise price targets. Instead, they're cutting them. Citigroup (C) trimmed its price target on SMCI to $25 from $39, a reduction of about 35%, while holding its “Neutral” rating, signaling that the risk-reward balance remains uncertain.

The driver? Reputation risk.

A federal court unsealed an indictment naming three individuals connected to Super Micro, alleging a conspiracy to violate U.S. export control laws. The accused include Yih-Shyan "Wally" Liaw, the company's senior vice president of business development and a board member; Ruei-Tsang "Steven" Chang, a sales manager in Taiwan; and Ting-Wei "Willy" Sun, a contractor.

According to the indictment, a Southeast Asian company allegedly acted as a middleman, compiling fake paperwork and repackaging servers to make it appear the hardware would remain in the region, when in reality it had already been forwarded to China. The defendants allegedly used "dummy" servers to fool both the company's own compliance team and a U.S. export control officer during a site visit.

The alleged scheme reportedly generated roughly $2.5 billion in sales for the server maker since 2024. Super Micro did not hold the required U.S. Commerce Department license to export servers featuring Nvidia (NVDA) graphics processing units to China, the indictment said.

Super Micro is not named as a defendant. According to a company statement, "The conduct by these individuals alleged in the indictment is a contravention of the Company's policies and compliance controls." SMCI said it placed Liaw and Chang on administrative leave and immediately terminated its relationship with the contractor.

Liaw subsequently resigned from the board. Following his departure, the board comprises eight directors. The company also appointed DeAnna Luna, a veteran trade compliance executive who formerly worked at Intel (INTC) and Teledyne Technologies (TDY), as its acting chief compliance officer.

SMCI Stock Impacted by Falling Margins

Despite the legal cloud hanging over the stock, Super Micro's underlying business continued to grow. The server maker raised its full-year fiscal 2026 (ending in June) revenue guidance to at least $40 billion, up from prior estimates, and guided for at least $12.3 billion in third-quarter revenue.

However, non-GAAP gross margin came in at just 6.4% in the December quarter, down from 9.5% in the prior quarter. Expedited shipping costs, component shortages, particularly in memory and storage, and a heavy reliance on large data center customers who carry pricing leverage all weighed on profitability.

CEO Charles Liang expressed confidence that margins will recover. He pointed to the company's Data Center Building Block Solutions (DCBBS) product line, a one-stop-shop infrastructure offering that covers everything from cooling systems to power backup, as a higher-margin growth driver. DCBBS contributed 4% of profits in the first half of fiscal 2026, and management expects that contribution to reach double digits by the end of calendar 2026.

Should You Buy SMCI Stock Right Now?

Buying a dip works best when the dip is about sentiment, not fundamentals. Presently, SMCI faces both.

The business is growing fast. But between margin pressure, customer concentration risk (one customer made up 63% of Q2 revenue), and now a federal indictment involving senior executives, this is not a clean story.

Out of the 19 analysts covering SMCI stock, three recommend “Strong Buy,” two recommend “Moderate Buy,” 10 recommend “Hold,” one recommends “Moderate Sell,” and three recommend “Strong Sell.” The average SMCI stock price target is $37.47, above the current price of about $24.

Investors with a high-risk tolerance and a long time horizon may find the current price compelling. Everyone else might want to wait for more clarity on the legal situation before stepping in.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)