/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

AI server maker Super Micro Computer (SMCI) has found itself in more trouble after its co-founder and two others were indicted by the U.S. Justice Department for violating U.S. export laws. The three allegedly illegally exported Nvidia (NVDA) GPUs worth about $2.5 billion to China, with one of the co-founders being the primary accused. Among the other two accused, one was a Super Micro sales manager in the Taiwan office, while the other was a contractor.

Although the company itself was not named as a defendant in the case, the indictment of the plaintiff was quite damning, stating, “Those controls are in place to protect U.S. national security and foreign policy interests, among other things.”

About Super Micro Computer

Founded in 1993, Super Micro is a high-performance server and data center infrastructure provider. Its core offerings include AI servers, data center infrastructure, storage, cloud systems, and edge/5G infrastructure. Its customers span the entire spectrum of the AI ecosystem, including hyperscalers, enterprises, cloud providers, and AI startups.

Valued at a market cap of $12.3 billion, SMCI stock is down 52% over the past year.

So, what to make of the company's latest setback? Let's find out.

SMCI: The AI Meme Stock

Between March 2022 and March 2024, the SMCI stock went parabolic, rallying by an unbelievable 2,640% to reach its all-time high of $114. Hailed particularly for its cooling capabilities, Super Micro was supposed to be one of the leaders of the massive AI infrastructure building. However, the stock has dwindled by 82% from those levels, as all the hype around the company was undone by governance and accounting issues simmering beneath.

While this was not the company's first tryst with falling foul of export restrictions, recent years have been particularly debilitating in terms of adverse issues. Delisting from Nasdaq in 2018 and being accused of accounting manipulations by the SEC in 2020 were some of its earlier problems; 2024 was the nadir. A scathing report from short-seller Hindenburg Research in August was followed by a Justice Department investigation in September, culminating in its auditor, Ernst & Young, resigning, citing transparency and internal control issues.

Thus, the company has been in the doldrums ever since. But it should not have been like this.

Not Driven by Meme Madness Alone

During that same 2022–2024 period, Super Micro Computer transformed from a relatively niche server manufacturer into a central pillar of the artificial intelligence infrastructure boom, which ignited a historic rally in its share price. This spectacular rerating was not merely a byproduct of market hype but was underpinned by a dramatic acceleration in the fundamental performance of the business. As hyperscalers and enterprise data centers scrambled to build out the immense computational capacity required to train and run generative AI models, Super Micro positioned itself as the premier hardware provider capable of turning raw silicon into fully optimized plug-and-play server racks.

A primary catalyst for this success was the highly adaptable modular approach of the company, known as Building Block Solutions. Rather than designing rigid, one-size-fits-all servers, Super Micro engineered a vast catalog of interchangeable components that could be rapidly assembled and customized to meet the highly specific demands of different clients. This engineering philosophy gave the company a massive competitive advantage in speed to market. When new generations of advanced processors were released, Super Micro could iterate and ship compatible server racks months faster than larger legacy hardware giants like Dell (DELL) or Hewlett-Packard Enterprise (HPE). In a fast-paced AI arms race where early deployment of compute power dictated market dominance for cloud providers, this agility allowed Super Micro to capture significant market share and win massive enterprise contracts.

Furthermore, Super Micro established a wide economic moat through its pioneering advancements in direct-to-chip liquid cooling technology. As artificial intelligence chips became exponentially more powerful, they also generated unprecedented levels of heat that traditional air-cooled data centers simply could not manage efficiently. Super Micro anticipated this thermal bottleneck and aggressively marketed rack-scale liquid-cooled solutions that significantly reduced power consumption and operating costs for data center operators. This technological edge made their servers the hardware of choice for power-hungry large language model deployments, further differentiating them from standard legacy hardware vendors.

However, the issue is of trust now, not demand or its capabilities. The scrutiny is also heavy, as hyperscalers have come increasingly under the scanner to justify their huge capex on AI, and alignment with a company riddled with governance and accounting issues would be fraught with risks. The only way Super Micro can salvage this situation is by overhauling the management and key decision-makers who have led the company down this slippery slope.

Financials Look Okay (But, Can They Be Trusted?)

Super Micro's results for the most recent quarter were the first in a while to report a beat on both the revenue and earnings front. Q2 2026 saw the company's net sales multiply to $12.7 billion from $5.7 billion in the year-ago period. Earnings went up by 17% in the same period to $0.69 per share, coming in much ahead of the Street expectations of $0.49 per share.

For fiscal Q3 2026, the company expects net sales and earnings to be at least $12.3 billion and $0.60 per share, which would denote yearly growth rates of 167.4% and 93.5%, respectively.

Coming back to Q2, for the six months ended Dec. 31, 2025, Super Micro's net cash flow from operations came in at a negative $941.4 million, compared to an inflow of $169.1 million in the prior year. Overall, the company closed the quarter with a cash balance of about $4.1 billion, which was much higher than its short-term debt levels of $201.8 million.

Notably, the company's stock is also trading at undervalued levels. Its forward P/E and P/S of 9.10 and 0.30 are lower than the sector medians of 21 and 2.93, respectively.

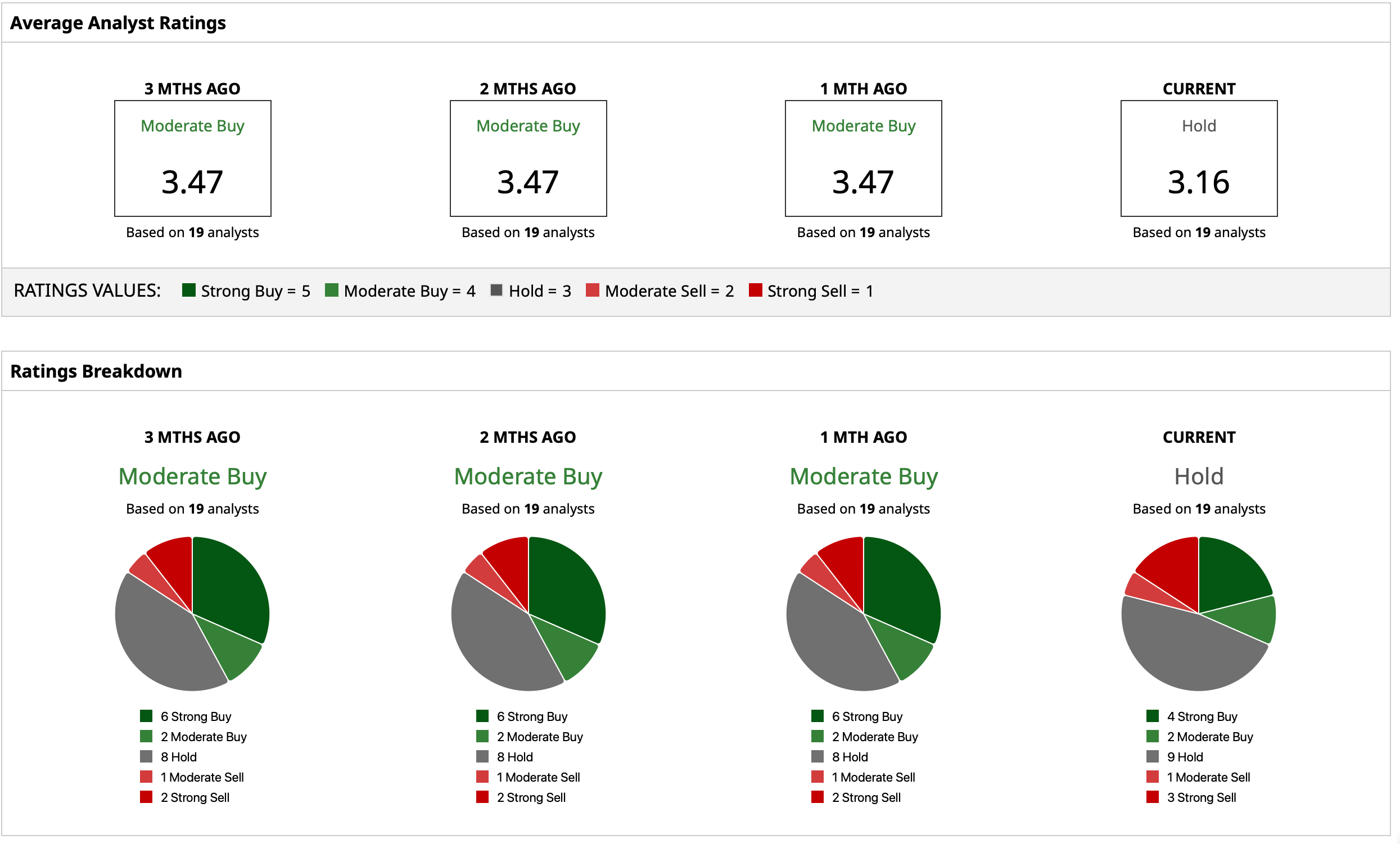

Analyst Opinion on SMCI Stock

Considering all this, analysts have attributed an overall rating of “Hold” for SMCI stock, with a mean target price of $42.31. This denotes an upside potential of about 100% from current levels. Out of 19 analysts covering the stock, four have a “Strong Buy” rating, two have a “Moderate Buy” rating, nine have a “Hold” rating, one has a “Moderate Sell” rating, and three have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)