Constellation Brands, Inc. (STZ) is a leading New York-based beverage alcohol company, best known for its premium portfolio of imported beer, wine, and spirits. With a market cap of $25 billion, the company has built a strong position by focusing on high-end, consumer-favored brands and shifting its mix toward faster-growing categories like imported beer.

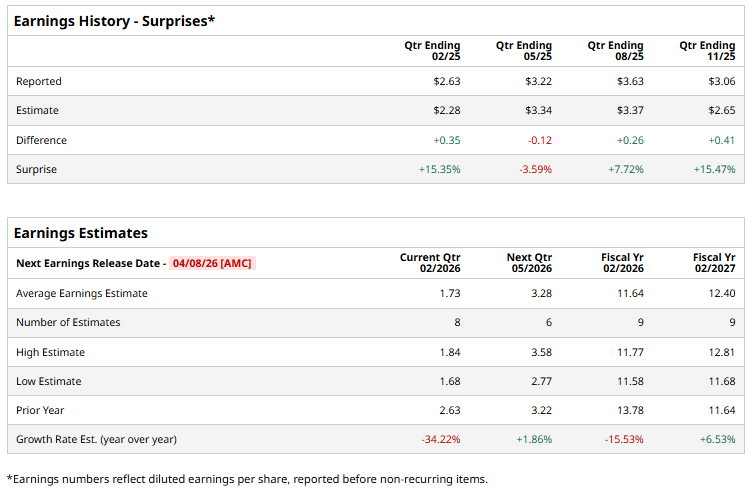

The beverage titan is expected to announce its fourth-quarter earnings for 2026 after the market closes on Wednesday, Apr. 8, 2026. Ahead of the event, analysts expect STZ to report a profit of $1.73 per share on a diluted basis, down 34.2% from $2.63 per share in the year-ago quarter. The company exceeded consensus estimates in three of the last four quarters, while missing the forecast on one another occasion.

For the fiscal year that ended in February 2026, analysts expect STZ to report EPS of $11.64, down 15.5% from $13.78 in fiscal 2025. However, its EPS is expected to rise 6.5% year over year to $12.40 in fiscal 2027.

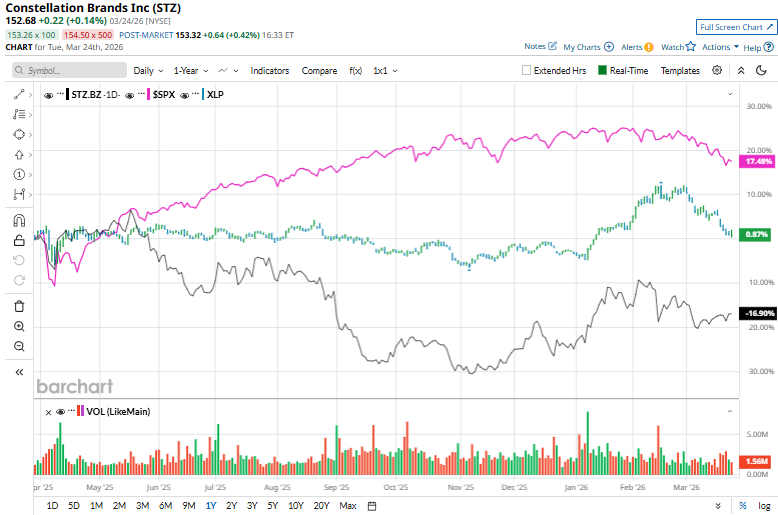

STZ stock has slumped 15.3% over the past year, trailing the S&P 500 Index’s ($SPX) 13.7% gains and the State Street Consumer Staples Select Sector SPDR Fund’s (XLP) 2.2% rise over the same time frame.

Constellation Brands has trailed the broader market over the past year mainly due to slowing growth and margin pressures in its core beer segment, which had previously been its primary driver. Rising input costs, such as packaging and raw materials, increased marketing and capacity investments, and softer-than-expected demand growth have weighed on profitability. Investor sentiment has also been dampened by concerns around valuation, execution risks, and its exposure to consumer spending trends.

Analysts’ consensus opinion on STZ stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 24 analysts covering the stock, 10 advise a “Strong Buy” rating, three suggest a “Moderate Buy,” nine give a “Hold,” one advocates a “Moderate Sell,” and the last analyst recommends a “Strong Sell.” STZ’s average analyst price target is $171.68, indicating a potential upside of 12.4% from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)