/AI%20(artificial%20intelligence)/AI%20Infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

Vertiv Holdings (VRT) has officially entered the S&P 500 Index ($SPX) as of March 23, cementing its position as one of the most essential infrastructure providers in the artificial intelligence (AI) ecosystem.

The timing is no coincidence. Vertiv's growth has been fueled by staggering demand for AI data center infrastructure, particularly power and cooling systems required for high-performance computing. Vertiv’s shares have surged 64% so far this year, while the Magnificent Seven stocks have slumped. Over the past year, the stock has rallied 183%, outperforming the broader market gain of 17.4%.

Is it too late to buy VRT stock? Let’s find out.

Inclusion in the S&P 500—What Does It Mean for Investors?

Valued at $96.9 billion, Vertiv provides the critical infrastructure that powers and cools data centers. As AI workloads become more demanding, Vertiv's technology helps to reduce overheating, downtime, and energy inefficiencies, making it a critical enabler of modern digital and AI infrastructure.

Now that Vertiv has been added to the S&P 500 Index as part of its quarterly rebalancing, trillions of dollars in passive funds or ETFs tracking the index are required to buy Vertiv’s shares. This creates immediate demand and supports the share price. It also signals that Vertiv has reached a certain scale, profitability, and stability, which has allowed it to earn this place and justify its premium over time.

Vertiv’s Fundamentals Justify It

Organic orders in the fourth quarter rose 152% year-over-year (YoY), reflecting a massive acceleration in demand. What’s more, over the trailing twelve months, organic orders grew 81%. Revenue increased 23% to $2.8 billion, while adjusted EPS jumped 37% to $1.36 in the quarter. The company’s book-to-bill ratio stood at an extraordinary 2.9x, while backlog reached $15 billion. Management expects this backlog to translate into revenue over the next 12 to 18 months.

For the full year, the company reported $10.2 billion in revenue, up 26% organically, while EPS surged 47% to $4.20. Management believes that the AI-driven data center buildout is still in its early stages, and Vertiv is well-positioned to benefit from rising demand. Its "One Core" platform is an end-to-end data center solution capable of growing to gigawatts, while "SmartRun" offers prefabricated infrastructure that shortens setup times. These technologies are already being deployed at scale by major customers such as Microsoft (MSFT), Amazon (AMZN), and AT&T (T), among others, highlighting Vertiv's role as a key enabler of AI infrastructure.

While investing aggressively for growth, Vertiv can expand its margins, which is rare for a growing company. Adjusted operating margin reached 23.2% in Q4, thanks to operational leverage, productivity gains, and favorable pricing. Cash flow generation is equally strong, with full-year free cash flow reaching $1.9 billion.

Vertiv’s outlook for 2026 suggests that its growth story is just getting started. For Q1 of 2026, Vertiv expects EPS growth of 53% and revenue growth of 22%, with continued strength in the Americas. For the full year, the company expects adjusted EPS of approximately $6.20 at the midpoint, representing 43% growth with 28% organic growth at $13.5 billion.

Buy Now or Too Late?

Vertiv’s inclusion in the index is a turning point for the company. It validates its position as a large-cap leader in the most critical and evolving sector now—AI infrastructure. Its $15 billion backlog, accelerating pipeline, and strong 2026 guidance all signal that demand remains robust and is far from peaking. However, it also raises valuation concerns. VRT stock is trading at a premium of 41x forward 2026 earnings, which are estimated to increase by 46%. Analysts further expect earnings to increase by 30% in 2027. Though pricey, Vertiv’s fundamentals justify owning the stock.

While Vertiv is an excellent long-term buy, risk-averse investors might want to wait for a better entry point.

Is VRT Stock a Buy, Hold, or Sell on Wall Street?

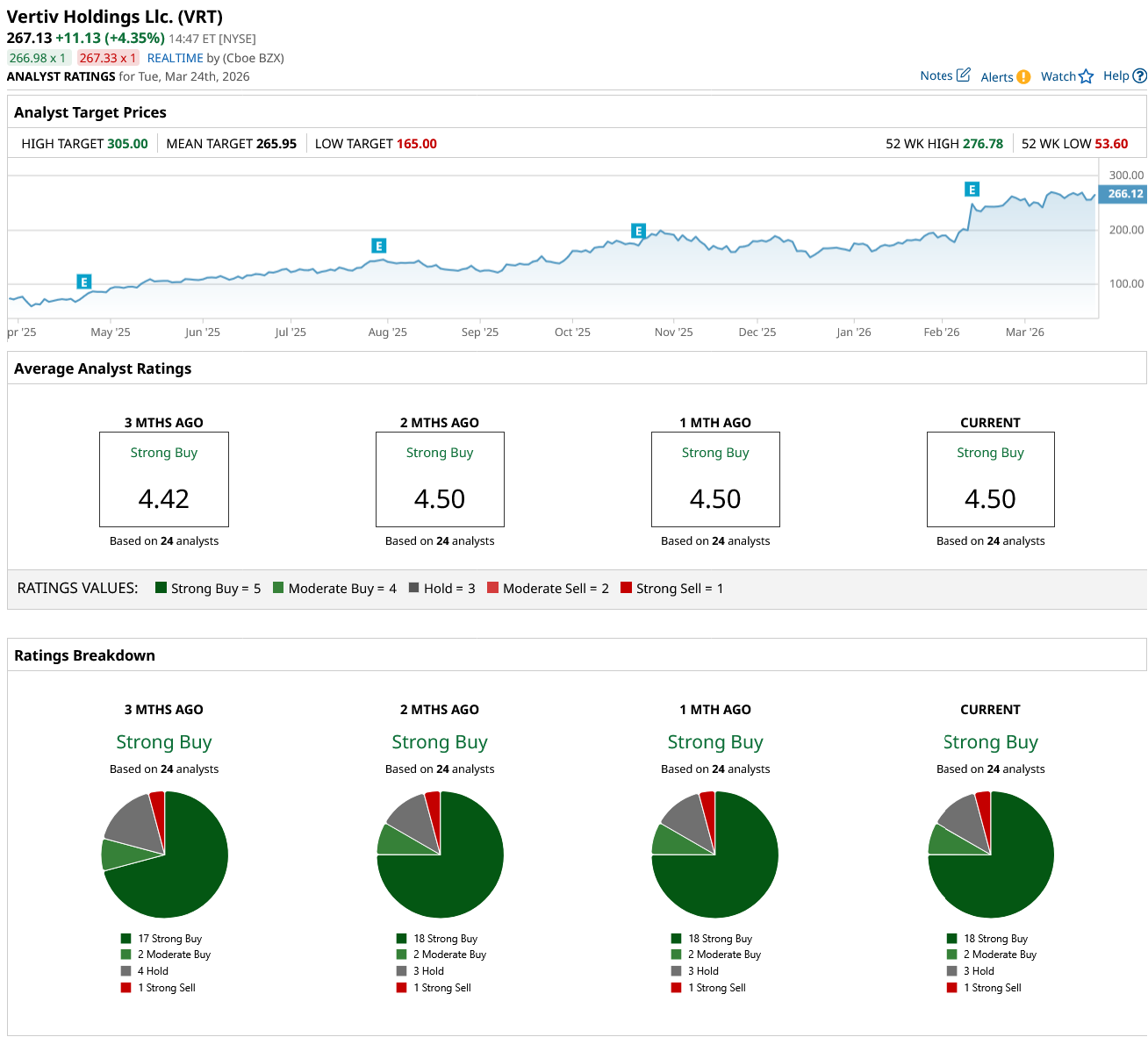

On Wall Street, VRT stock has garnered an overall “Strong Buy” rating. Of the 24 analysts covering the stock, 18 rate it as a "Strong Buy," two call it a "Moderate Buy," three recommend a “Hold,” and one has a “Strong Sell” rating. It currently sits just above its average price target of $265.95. However, its high price estimate of $305 indicates a possible 14% rally over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)