Airport chaos has become the new normal in the U.S., with long security lines, widespread delays, and frequent cancellations disrupting travel. The prolonged partial government shutdown has left thousands of TSA agents unpaid, triggering mass absenteeism and resignations. Geopolitical uncertainty is adding another layer of risk. Missile and drone volleys across the Middle East have already led to airspace closures, longer flight routes, and surging fuel costs.

As disruptions mount both on the ground and in the air, investors might want to reassess their exposure to the sector. For airline stocks, rising costs and unreliable schedules can quickly pressure margins and weaken demand.

Is it time to give up on these two airline stocks?

Airline Stock #1: American Airlines (AAL)

Valued at $7.1 billion, American Airlines (AAL) operates passenger and cargo flights, connecting hundreds of destinations across the U.S. and internationally through a network of major hubs like Dallas-Fort Worth, Charlotte, and Miami. For American Airlines, the financial and operational impact is becoming increasingly hard to ignore, led by the recent events.

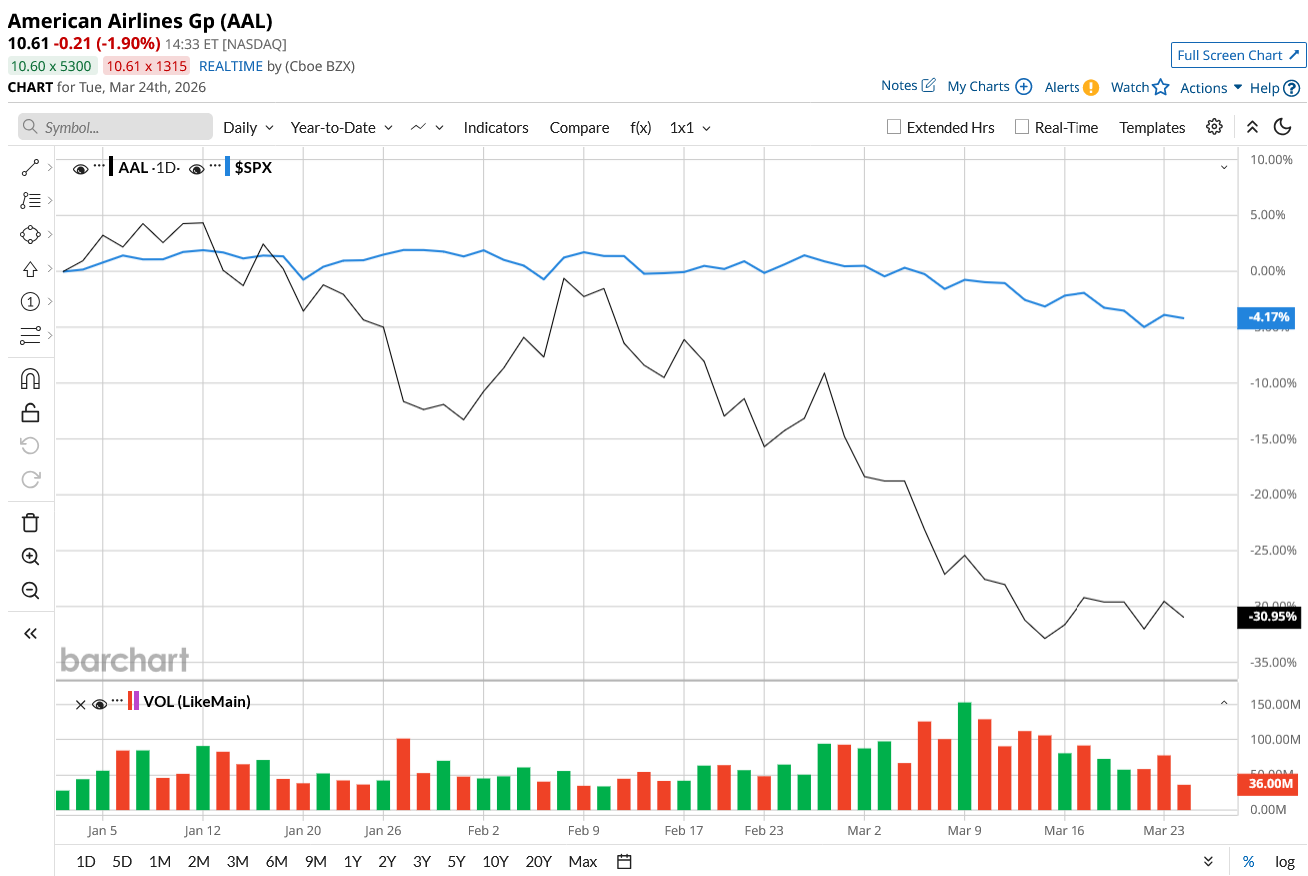

AAL stock is down 32% year-to-date (YTD), compared to the S&P 500 Index ($SPX) dip of 4.2%.

The airlines closed 2025 on a turbulent note as weather-related concerns caused widespread disruptions. More than 9,000 flights were cancelled in only four days, wreaking havoc on key hubs such as Dallas-Fort Worth and Charlotte. Even with improved systems and planning, disruptions of this scale can take a toll on revenue. To add to the worries, a prolonged U.S. government shutdown alone reduced revenue by approximately $325 million in the fourth quarter. The impact was severe in domestic markets, particularly Washington, D.C., where government-related travel demand is high.

Bookings declined in Q4, revealing how vulnerable airline revenues are to macroeconomic and political disturbances. Total operating revenue increased by 2.5% to $13.9 billion, while full-year revenue gained by 0.8% to $54.6 billion. The most significant impact was on profitability, with net income falling 82% to $0.15 per share in the fourth quarter and 86.3% for the year.

Despite the challenges, management stated that bookings rebounded in early 2026, with system-wide revenue up double digits year-over-year (YoY) in January. Premium travel continues to be a major strength, reflecting sustained demand from higher-paying customers. Looking ahead, the company expects Q1 revenue growth of 7% to 10% and a return to positive domestic unit revenue trends. It also expects to generate free cash flow of over $2 billion in 2026. But unit costs (excluding fuel) are expected to rise 3% to 5% in the first quarter, partly due to labor investments and operational adjustments.

Furthermore, weather delays may also have an additional $150 million to $200 million impact on revenue. Thus, American Airlines anticipates a loss of $0.10 to $0.50 per share in the first quarter.

Financially, the airline is working on strengthening its balance sheet. It reduced its total debt by $2.1 billion in 2025, with current total debt now standing at $36.5 billion. It ended the quarter with $9.2 billion in cash and investments. The company now targets reducing debt below $35 billion by 2026. The overall impact of the current disruptions in March will be clearer when the company reports its first-quarter results.

On the one hand, demand is recovering, premium travel is strong, and American Airlines’ long-term strategy appears solid. On the other, the airlines’ business remains highly exposed to factors beyond its control, including extreme weather, government disruptions, and global uncertainty. With operational chaos mounting and costs rising, investors need to assess if the risk-reward of staying invested in AAL stock is still attractive.

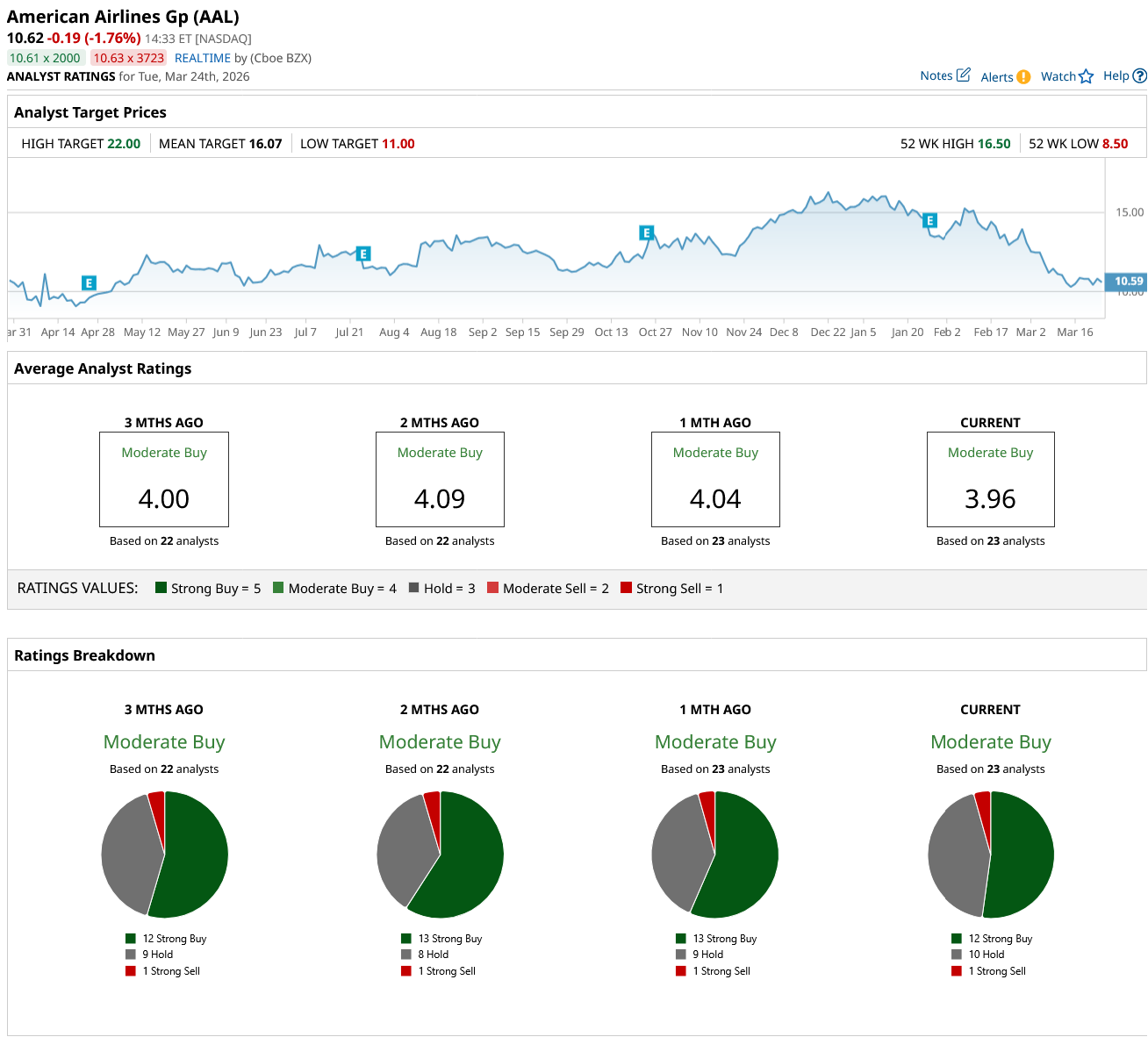

Overall, Wall Street rates AAL stock as a “Moderate Buy.” Of the 23 analysts covering the stock, 12 rate it a “Strong Buy,” 10 rate it a “Hold,” and one says it is a “Strong Sell.” The average target price of $16.07 suggests the stock can climb by 51% from current levels. Plus, the high price estimate of $22 suggests AAL has an upside potential of 107% over the next year.

Airline Stock #2: Delta Air Lines (DAL)

Valued at $42.5 billion, Delta Air Lines (DAL) is a major global airline that transports passengers and cargo, operating an extensive network of domestic and international flights through key hubs like Atlanta, New York, and Los Angeles. While Delta Air Lines is exposed to the same chaos as most airlines, its business model has made it strong enough to withstand these shocks.

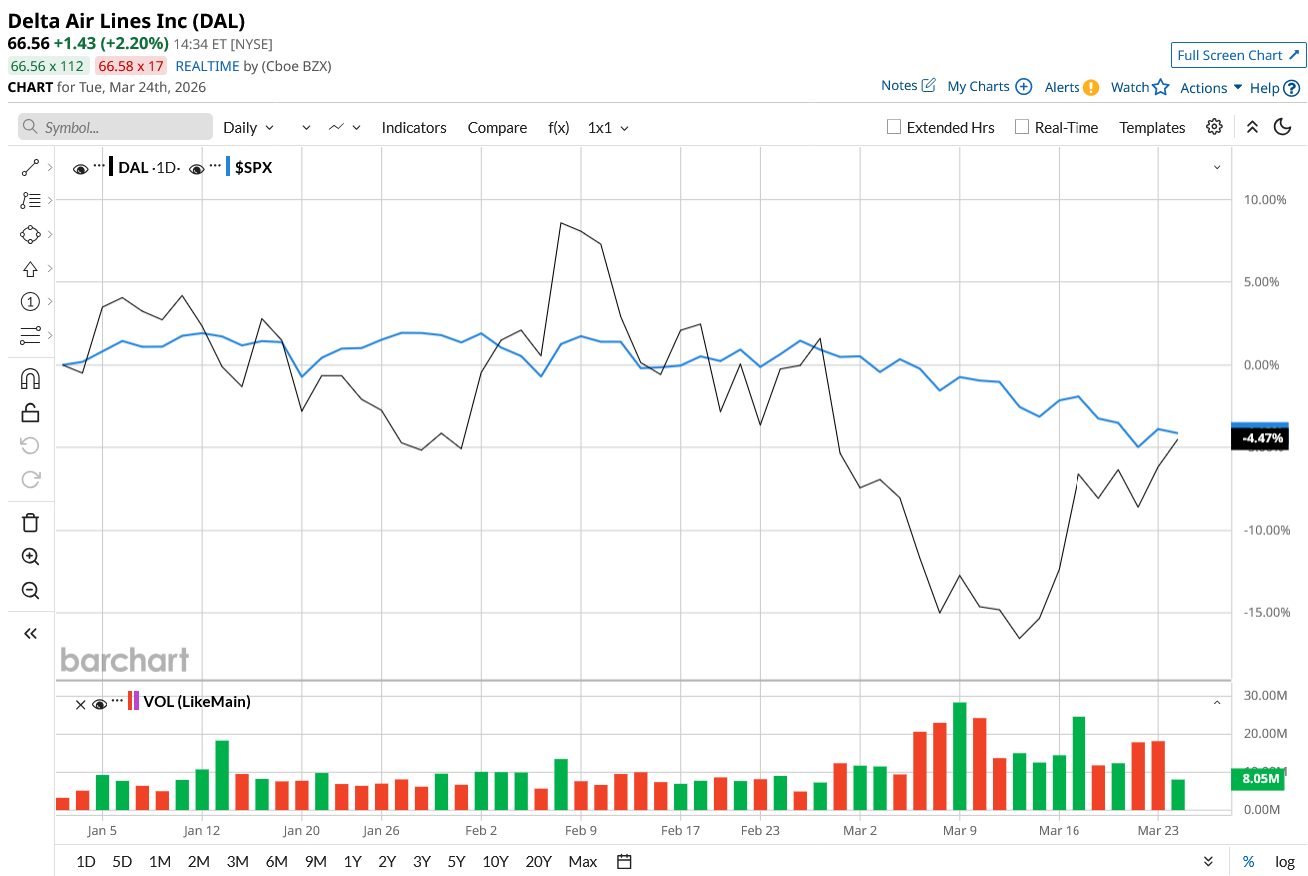

Delta stock is down 5% YTD, better than AAL’s dip so far this year.

Despite the turbulences, Delta ended 2025 on a healthy note. Total revenue increased 2.2% to $58 billion for the full year. Delta no longer relies primarily on ticket sales. It has now built a diversified revenue model that now accounts for 60% of total revenue. In 2025, premium revenue grew 7%, reflecting strong demand for higher-end travel experiences. Cargo revenue rose by 9%, while maintenance, repair, and overhaul (MRO) revenue surged by 25%, highlighting the strength of Delta’s ancillary businesses. Loyalty revenue rose 6%, and travel-related product sales also rose double-digit. Similarly, corporate travel showed solid momentum, with sales rising 8% YoY.

However, management noted that the results weren’t completely immune to macroeconomic issues. The government shutdown reduced Q4 pre-tax profit by $200 million (or $0.25 per share) and slowed capacity expansion by around two points. Net income declined 16.2% YoY to $1.55 per share in Q4 and by 5.5% for the full year to $5.82 per share.

Delta remains stronger than American Airlines when it comes to cash generation and balance sheet strength. It generated $4.6 billion in free cash flow in 2025. Over the past three years, total free cash flow has reached $10 billion, allowing Delta to aggressively reduce debt. In 2025 alone, the company lowered its debt by $2.6 billion. It ended the year with adjusted net debt of around $14 billion and "unencumbered assets" of $35 billion.

In 2026, Delta expects to generate free cash flow between $3 billion and $4 billion and reduce leverage further to around 2x. Despite all the external disruptions, Delta has built a business model designed to withstand these challenges. That said, airline stocks are not immune to external shocks. The impact of the recent disruptions will be more clear in its first-quarter results.

Delta appears to be structurally stronger than American Airlines due to its diverse revenue base, robust financial sheet, and significant free cash flow. All in all, if you are ready to put up with the short-term volatility, Delta is still a stronger airline company to own right now.

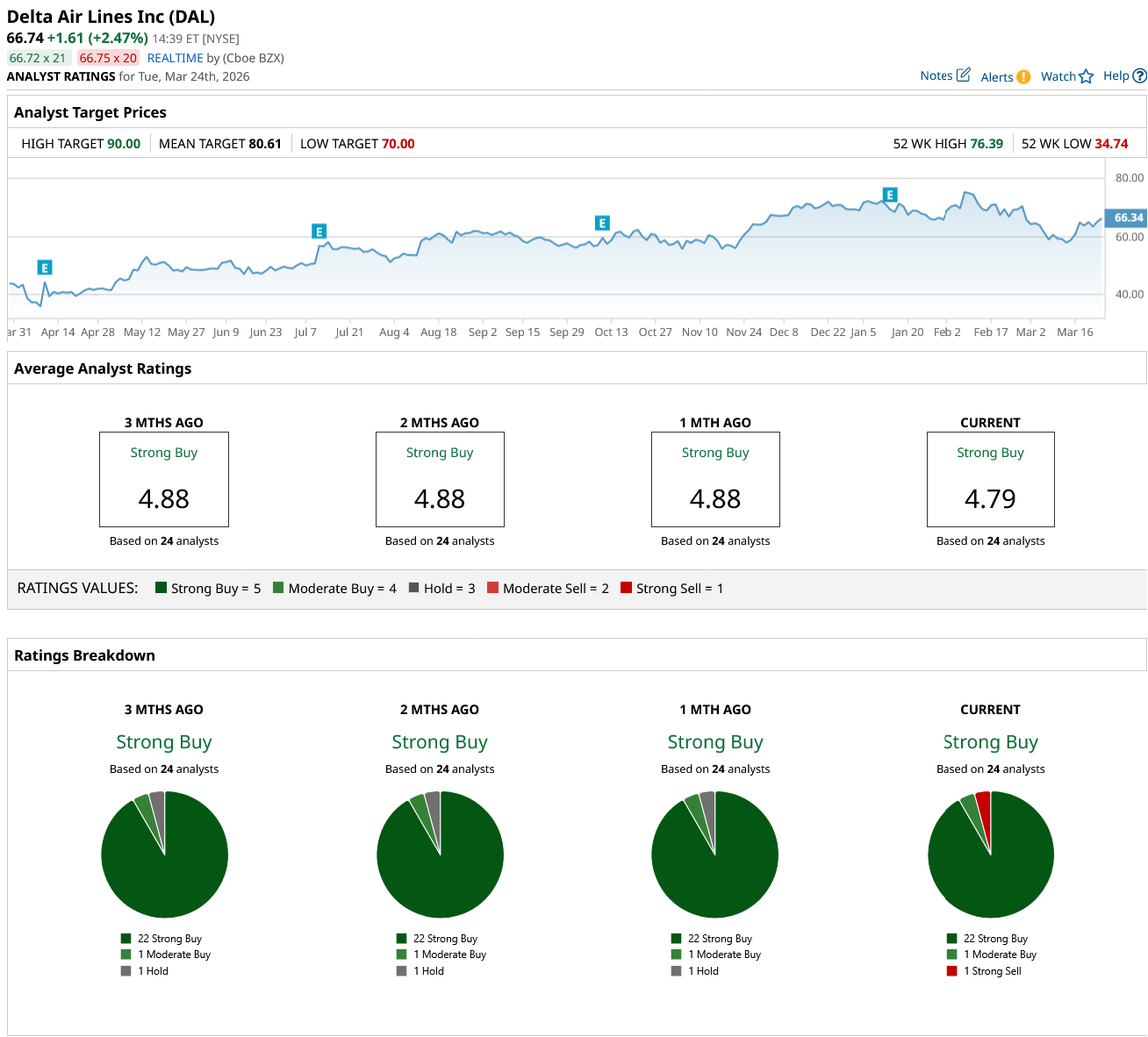

Overall, Wall Street rates DAL stock as a “Strong Buy.” Of the 24 analysts covering the stock, 22 rate it a “Strong Buy,” one says it is a “Moderate Buy,” and one rates it a “Strong Sell.” The average target price of $80.61 suggests the stock can climb by 21% from current levels. Plus, the high price estimate of $90 suggests AAL has an upside potential of 35% over the next year.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)