Tesla (TSLA) has never been shy about thinking big. But what the company is set to unveil this week may be its most ambitious move yet, and most investors haven't fully processed what it means.

On March 14, CEO Elon Musk posted on X, formerly Twitter, that the "Terafab Project launches in 7 days." That puts the official kickoff on March 21. If Tesla pulls this off, it could reshape the entire semiconductor industry.

Here's why Tesla shareholders should be paying close attention.

What Is Tesla's Terafab Project

Terafab is Tesla's plan to build a massive, vertically integrated semiconductor fabrication facility. The goal is to produce logic chips, memory, and advanced packaging all under one roof, domestically, at an enormous scale.

According to a report from Teslarati, the facility is projected to produce between 100 billion and 200 billion AI and memory chips per year, targeting 100,000 wafer starts per month. For context, that kind of output would put Tesla in the same conversation as TSMC (TSM) and Samsung, the world's most advanced chipmakers. The facility is expected to use two-nanometer (nm) process technology, which is among the most advanced nodes currently in commercial production worldwide.

Musk first flagged the need for a chip fab at Tesla's annual shareholder meeting last year, warning that even the best-case output from existing suppliers wouldn't be enough to meet Tesla's needs.

He repeated the warning on the company's fiscal Q4 earnings call, telling investors directly, “If we don't do the Tesla Terafab, we're going to be limited by supplier output of chips.” The concern isn't abstract. Musk projected that chip supply could become Tesla's single biggest growth constraint within three to four years. That's the window Terafab is designed to close.

"Optimus is completely useless without an AI chip," Musk said on the earnings call. "It's like the Tin Man from The Wizard of Oz….but even worse, at least the Tin Man could walk."

A Tepid Performance in Q4

To understand why Terafab matters so much right now, it helps to look at where Tesla stood at the end of 2025.

Tesla’s Q4 2025 earnings call painted a picture of a business in transition.

- Total gross margin came in above 20% for the first time in two years, a meaningful recovery.

- Automotive gross margin, excluding regulatory credits, improved from 15.4% to 17.9% sequentially.

- Energy revenue for the full year reached nearly $12.8 billion, up 26.6% year-over-year (YoY).

- At the same time, Tesla flagged some real headwinds. Tariff impacts exceeded $500 million in Q4.

- Net income took a hit from a markdown in Bitcoin holdings and unfavorable foreign-currency movements.

- Free cash flow came in at $1.4 billion, which may not be enough to fuel Tesla’s expansion plans.

Chief Financial Officer Vaibhav Taneja said on the call that capital expenditures for 2026 are expected to exceed $20 billion, covering six new factories, expanded AI compute infrastructure, and fleet growth for both Robotaxi and Optimus. That level of spending will burn cash, and Taneja acknowledged that the company is in active discussions with banks about financing options, particularly for the Robotaxi fleet.

Full Self-Driving adoption also continued to climb, reaching nearly 1.1 million paid customers globally by the end of Q4. That number, and the recurring subscription revenue it represents, is increasingly central to Tesla's financial story going forward.

The Q4 results made one thing crystal clear: Tesla is betting its next decade on autonomy and artificial intelligence (AI). Terafab is how it plans to win that bet on its own terms.

Tesla also recently announced an expanded partnership with LG Energy Solution to build a $4.3 billion lithium iron phosphate (LFP) prismatic battery cell manufacturing facility in the U.S. Production begins in 2027, and the cells will power Tesla's Megapack 3 energy storage systems built in Houston, adding another layer to Tesla's domestic supply chain.

What Is the TSLA Stock Price Target?

Analysts forecast Tesla to increase revenue from $94.83 billion in 2025 to $266 billion in 2029. In this period, adjusted earnings are forecast to expand from $1.66 per share to $11.39 per share. If TSLA stock is priced at 50x forward earnings, it could gain 40% over the next four years.

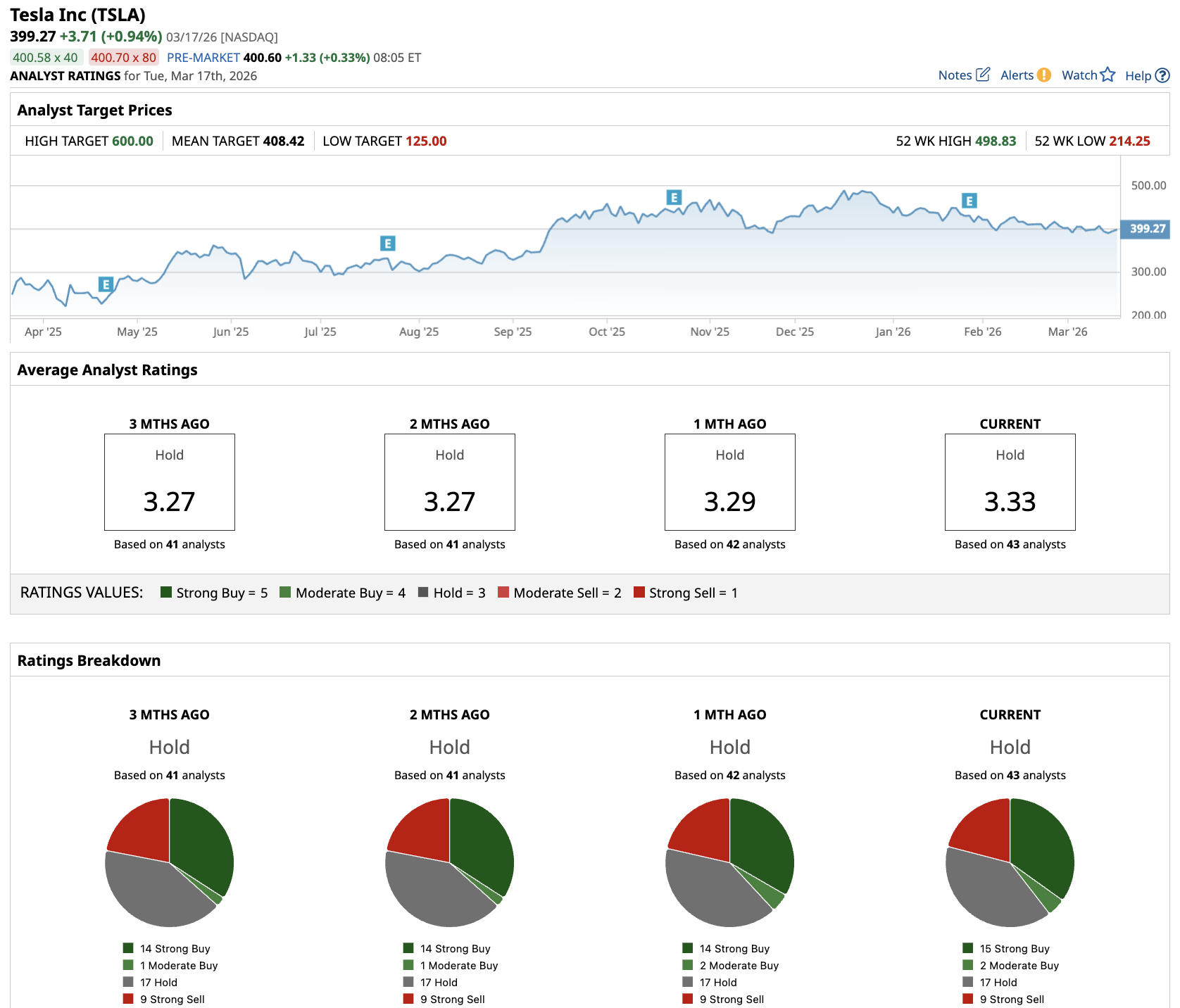

Out of the 43 analysts covering TSLA stock, 15 recommend “Strong Buy,” two recommend “Moderate Buy,” 17 recommend “Hold,” and nine recommend “Strong Sell.” The average TSLA stock price target is $408.42, above the current price of about $400.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)