I concluded a January 23, 2026, Barchart article on whether sugar’s bearish trend will end in 2026 with the following:

Commodity cyclicality suggests that sugar prices could be closer to a potential low than a high in 2026, making the risk-reward on a long position attractive.

Nearby March sugar futures were trading at 14.96 cents per pound on January 22, 2026. While the price fell to a lower low in mid-February, sugar futures have rallied over the past few weeks and are approaching technical resistance in the bear market that has remained firmly intact since the November 2023 high of 28.14 cents per pound.

A new multi-year low and a bounce

The continuous world sugar futures reached a 13.34 cents per pound low on February 12, 2026.

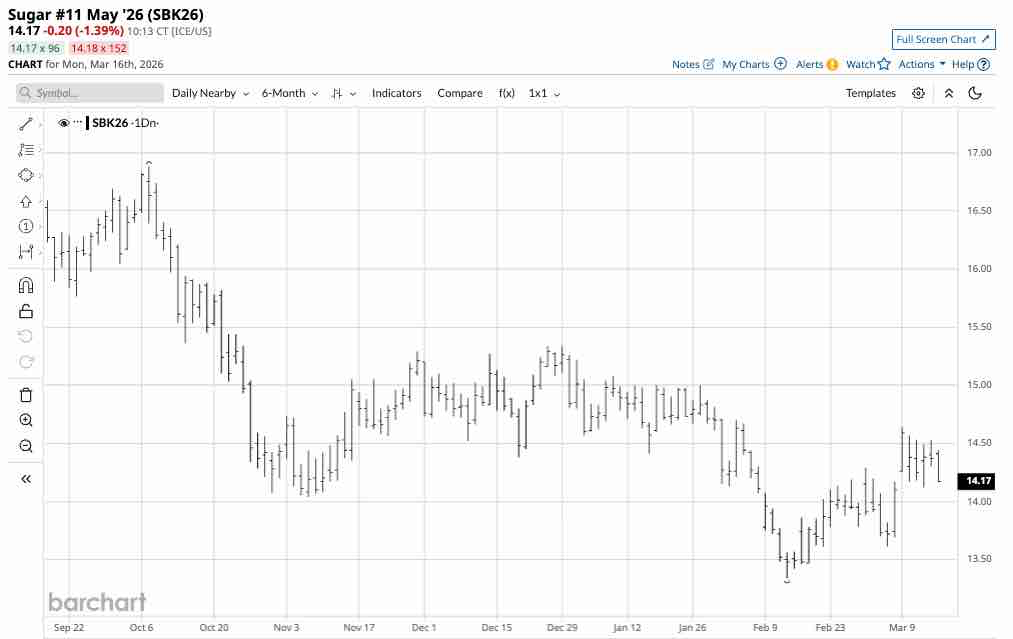

The daily continuous six-month chart shows that the sugar futures bounced higher from the low on February 12, reaching a high of 14.64 cents per pound on March 9.

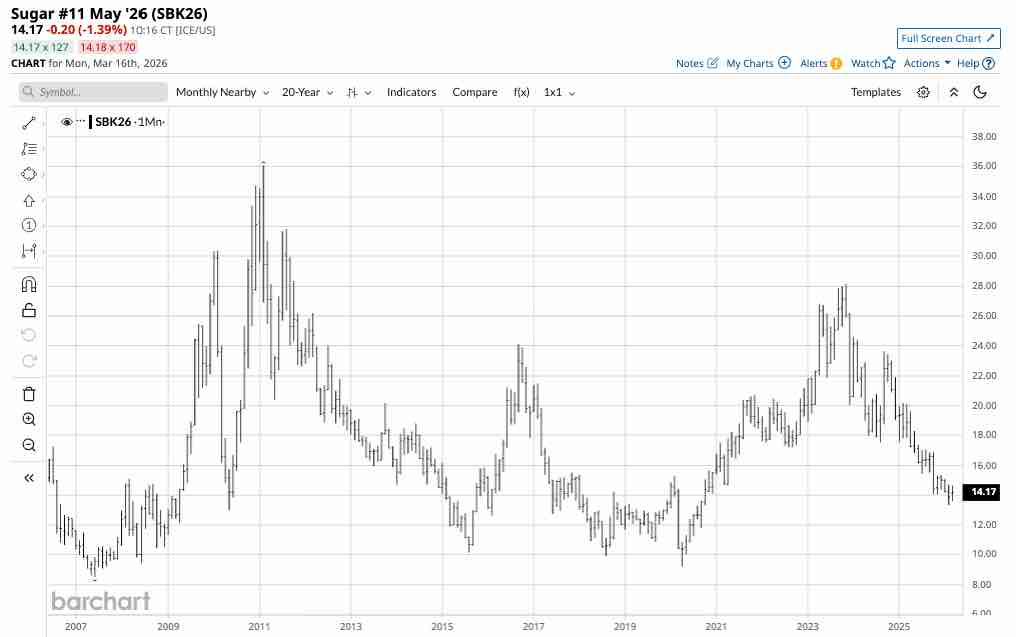

The monthly continuous contract chart highlights that the February 12 low was the lowest price for world sugar futures since October 2020. While world sugar futures bounced from the lowest price in years, the trend remains bearish.

Technical levels to watch in world sugar futures

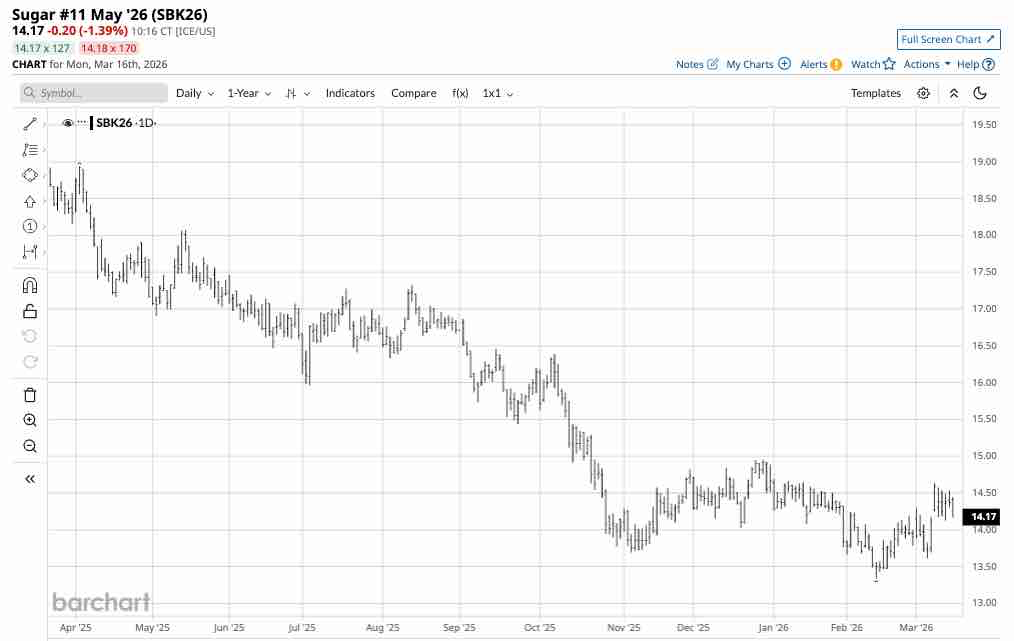

The daily one-year chart of ICE world sugar futures for May 2026 delivery highlights the critical technical levels to watch from a short-term perspective.

World sugar futures remain in a bearish trend despite the recent bounce from the mid-February multi-year low. The first technical resistance target is at the December 29, 2025, 14.95 cents. A move above 15 cents could be a gateway to a challenge of the October 7, 2025, high of 16.38 cents per pound. Technical support remains at the lowest level since October 2020 at 13.34 cents.

Commodity cyclicality continues to support sugar fundamentals

After reaching a 28.14 cents per pound high in November 2023, world sugar futures have more than halved at the most recent low. While many countries, including the United States, subsidize sugar prices to encourage production and avoid shortages, commodity cyclicality could mean that prices have declined to levels where free-market sugar production will decline, inventories will fall, and consumption will rise, leading to a price bottom.

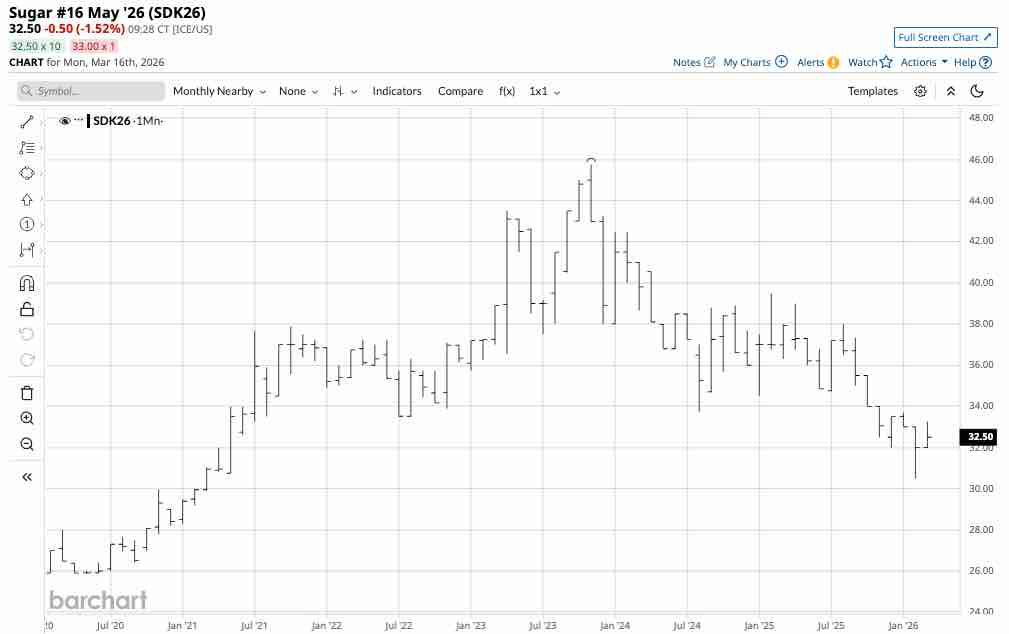

While world sugar futures for May delivery are at the 14.38 cents per pound level, U.S. subsidized sugar is more than double that price and is above the November 2023 high.

The monthly chart of U.S. sugar #16, which is the subsidized price, remains in a bearish trend, but the price at 32.50 cents per pound is over double the price of free market world sugar #11 futures. The U.S. subsidized price has declined from the high of 45.75 cents per pound in November 2023, when world sugar prices traded over 28 cents per pound. However, the subsidies will continue to affect global sugar prices, as they encourage production to avoid shortages.

World sugar is one of the most liquid soft commodities

In the soft commodities sector, world sugar futures are among the most liquid contracts with a of 1,014,621 contracts of long and short positions Each contract is 112,000 pounds. At 14.16 cents per pound, the contract value is $15,859.20. The total open interest is worth over $16.09 billion. The value of the other soft commodities open interest at current price levels is as follows:

- Arabica coffee- Open interest at 167,262 contracts, each contract is for 37,500 pounds. At $2.9200 per pound, the value of the open interest is $18.315 billion.

- Cocoa- Open interest at 188,663 contracts, each contract is for 10 tons. At $3,390 per ton, the value of the open interest is $6.396 billion.

- Cotton- Open interest at 334,317 contracts, each contract is for 50,000 pounds. At 68 cents per pound, the value of the open interest is $11.367 billion.

- Frozen concentrated orange juice- Open interest at 7,873 contracts, each contract is for 15,000 pounds. At $1.9975 per pound, the value of the open interest is $235.9 million.

World sugar and Arabica coffee are the most liquid soft commodities. The average daily trading volume in the world sugar futures is around 200,000 contracts or approximately $3.17 billion. In Arabica coffee, the value of the average daily volume of 40,000 contracts is higher at $4.38 billion.

World sugar and Arabica coffee are highly liquid futures markets, encouraging hedging and speculative activity. Moreover, liquid markets tend to be less volatile than illiquid markets that typically experience more price gaps.

CANE is the only ETF that tracks ICE world sugar futures

The most direct route for a risk position in world sugar is through the futures and options offered by the Intercontinental Exchange. The Teucrium Sugar ETF (CANE) provides a liquid alternative to the ICE futures. At $9.60 per share, CANE had over $13.85 million in assets under management. CANE trades an average of over 219,000 shares per day and charges a 0.93% management fee.

CANE owns a portfolio of three actively traded ICE sugar futures contracts, excluding the nearby contract, which attracts the most speculative activity and thus minimizes roll risks. Since the nearby contract tends to experience the most price volatility, CANE tends to underperform the nearby contract on the upside and outperform it when prices decline.

The latest rally in world sugar futures lifted the price by 9.75% from the February 12, 2026, low of 13.34 to the March 9, 2026, high of 14.64.

Over the same period, CANE moved 9.48% higher from $8.97 to $9.82 per share, which indicates that the deferred contracts moved higher in tandem with the nearby contract. The rise in deferred sugar futures could be a bullish sign for the soft commodity.

I continue to believe that commodity cyclicality will support world sugar prices, after they more than halved since the November 2023 high at the recent low. World sugar futures dropped 52.6% from the 2023 high to the 2026 low. Meanwhile, over the same period, the CANE ETF dropped 42.2% from $15.51 to $8.97 per share, outperforming the continuous world sugar futures contract. Buying world sugar or the CANE ETF on price weakness could be optimal over the coming weeks and months.

On the date of publication, Andrew Hecht did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)