Walmart's (WMT) Sam’s Club has set the wheels in motion, and the ripple effects could land right in Costco Wholesale Corporation’s (COST) favor. On April 1, the company announced a $10 increase in its annual membership fees, effective May 1. The base club tier will rise to $60 from $50, while the Plus membership will move to $120 from $110, marking the largest nominal increase for basic members in recent history.

Jefferies Financial Group (JEF) analyst Corey Tarlow views the move as a step toward deeper reinvestment in value. Sam’s Club plans to raise its Sam’s Cash annual cap for Plus members to $750 from $500, reinforcing the idea that higher fees come with enhanced benefits.

At the same time, the increase helps normalize elevated membership pricing across the category, which could strengthen long-term revenue and profit expectations for warehouse retailers. The ripple effect extends beyond Sam’s Club and puts players like BJ's Wholesale Club Holdings (BJ) and Costco in a favorable position.

Costco, in particular, stands to gain from this shift. Its model leans heavily on membership income and strong customer loyalty, so when a competitor pushes prices higher, it effectively tests the ceiling for the entire segment. That validation works in Costco’s favor. The company already commands higher renewal rates and carries a more premium brand perception, which gives it room to adjust pricing without shaking customer retention.

The market has started to connect the dots. COST stock rose 1.9% on April 2, a day after the announcement. The reaction may seem modest at first glance, but it often pays to read between the lines. When the market nods early, it sometimes signals that a bigger move could follow. As May 1 approaches, the story is worth watching closely.

About Costco Stock

Based in Issaquah, Washington, Costco runs membership warehouses where customers stock up on groceries, fresh produce, appliances, and everyday essentials at compelling prices. It complements the core offering with fuel stations, pharmacies, optical services, and travel solutions, creating a value ecosystem that keeps members coming back.

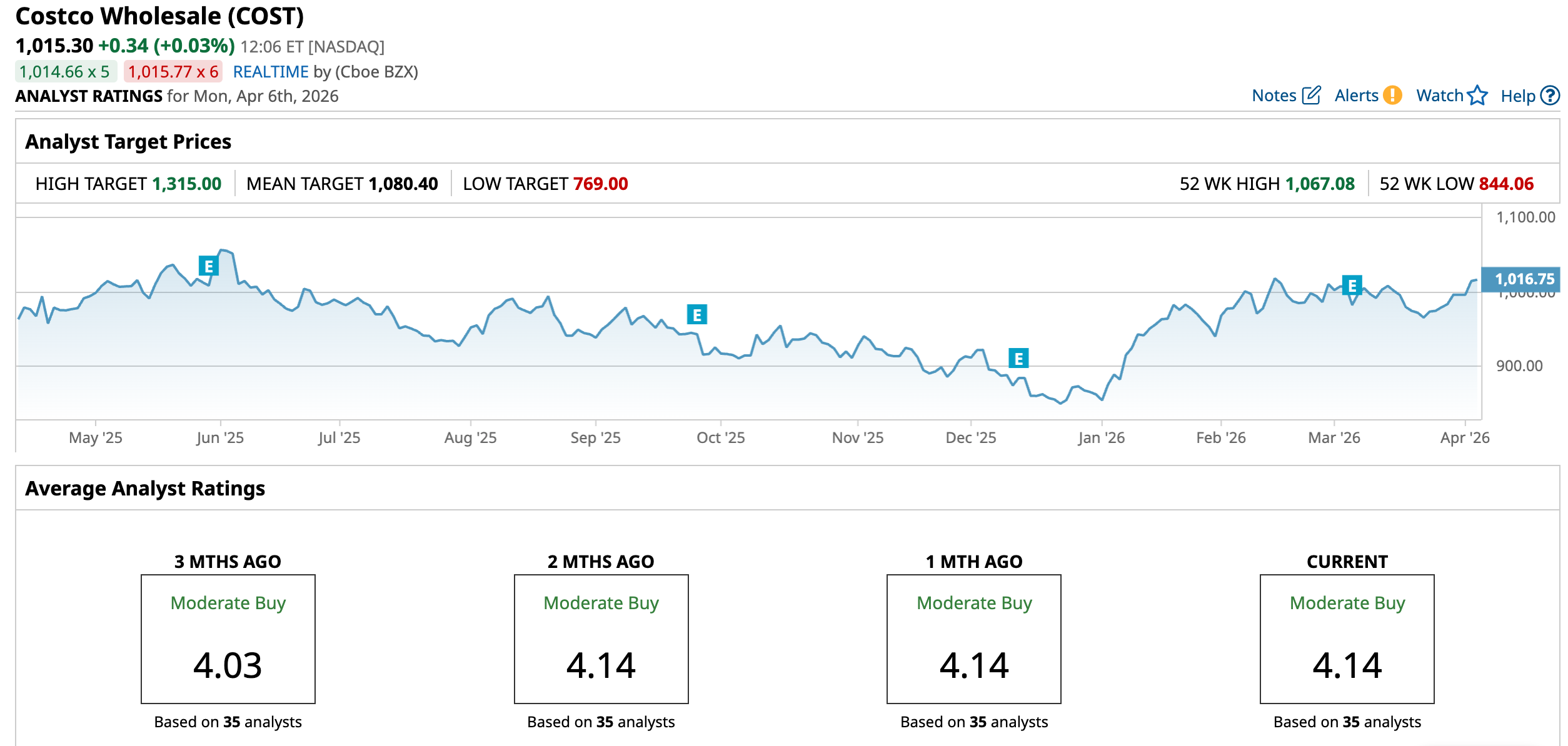

With a market cap of $450.3 billion, Costco has built both scale and trust. The consistency shows up in the stock, as shares have gained 10.86% over the past 52 weeks and climbed 17.8% year-to-date (YTD).

Momentum has held in the near term, with a 1.2% rise over the past month and a sharper 3.26% gain across the last five trading sessions, suggesting buyers continue to step in.

The market does not overlook the track record. COST stock is trading at 49.04 times forward adjusted earnings and 1.51 times sales, both above industry peers and their own five-year average multiples. Investors pay that premium because the company continues to execute and justify the multiple.

The income story ties it all together. Costco has raised its dividend for 21 consecutive years and maintains a disciplined approach to capital returns. It pays $5.20 per share annually, offering a yield of 0.51%. The company distributed its most recent dividend of $1.30 per share on Feb. 13 to shareholders on record as of Jan 30.

Costco Surpasses Q2 Earnings

On March 5, Costco reported its operating results for the second quarter of fiscal year 2026. During the quarter, revenue increased 9.2% year-over-year (YOY) to $69.6 billion, topping analyst estimates of $69.1 billion. EPS grew 13.9% from the year-ago value to $4.58, surpassing the Street’s expectations of $4.55.

Operating income rose 12.5% from the prior year’s period to $2.6 billion, while net income jumped 13.8% YOY to $2 billion. The balance sheet added another feather to the cap as cash and cash equivalents amounted to $17.4 billion as of Feb. 15, up from $14.2 billion on Aug. 31, 2025.

Membership trends continued to do the heavy lifting. At the end of the second quarter, Costco had 40.4 million paid executive memberships, up 9.5% YOY. Total paid members reached 82.1 million, growing 4.8%, while cardholders increased 4.7% to 147.2 million.

Capital expenditure came in at $1.29 billion for the quarter. Looking ahead, management is building for the long haul, expanding its warehouse footprint, upgrading high-volume locations, strengthening its depot network, and sharpening the digital experience. Owing to this, they project full-year fiscal 2026 CapEx to hit approximately $6.5 billion.

Further, Costco plans to open 28 net new warehouses in fiscal year 2026 and is aiming for 30+ annually in the years ahead. At the same time, it is fine-tuning execution through digital personalization, automation, and e-commerce, including piloting automated pay stations that enable seamless checkout with average transaction times of around eight seconds.

Looking ahead, earnings expectations remain firm. Analysts project Q3 fiscal 2026 EPS to rise 14.3% YOY to $4.89. For the full fiscal year 2026, the bottom line is expected to grow nearly 13% to $20.32, followed by another 9.8% increase to $22.32 in fiscal year 2027.

What Do Analysts Expect for Costco Stock?

Analysts continue to lean positive on Costco, and recent updates reflect growing conviction. Telsey Advisory Group maintained its “Outperform” rating while lifting its price target to $1,125 from $1,100. BMO Capital followed with an even more bullish stance, raising its target from $1,175 to $1,315 while reiterating an “Outperform” rating.

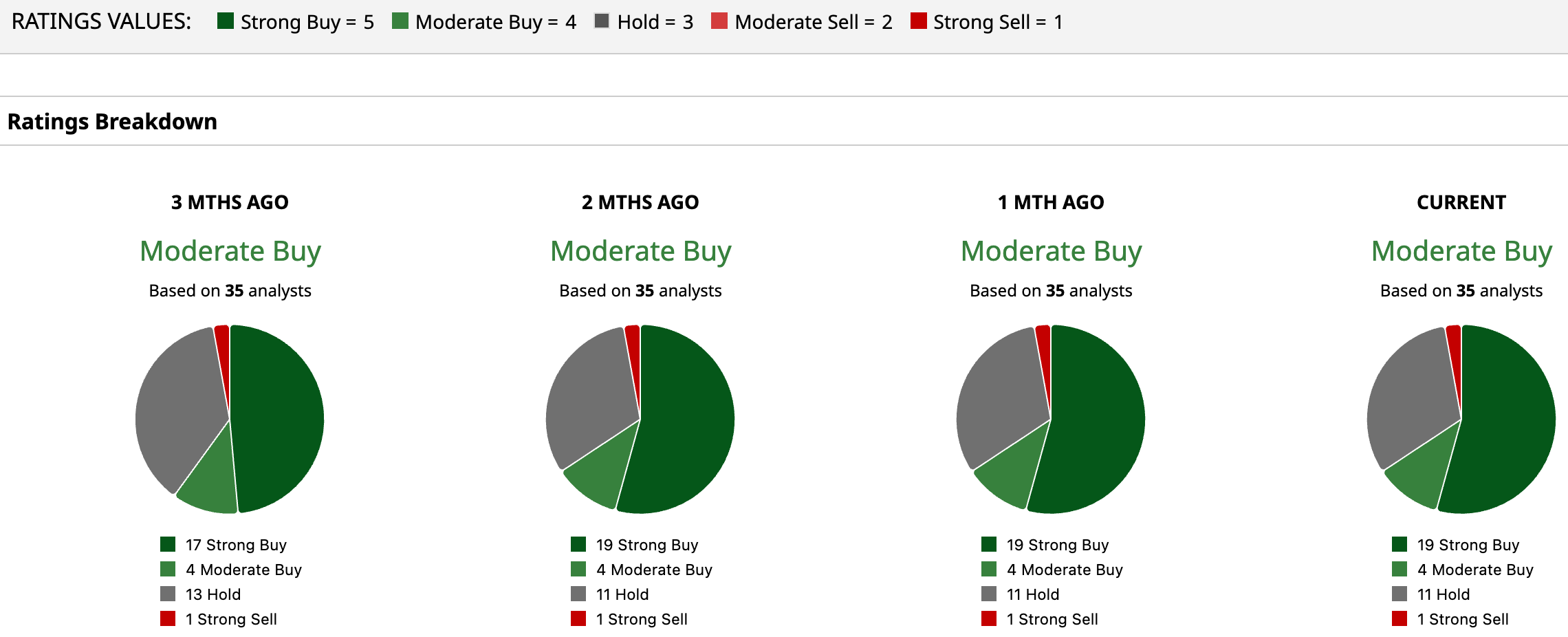

Overall, Costco carries an overall rating of “Moderate Buy.” Out of 35 analysts covering the stock, 19 rate it a “Strong Buy,” four assign a “Moderate Buy,” 11 recommend “Hold,” and one leans “Strong Sell.”

Against that backdrop, the mean price target of $1,080.40 implies a potential upside of 6.4%. Meanwhile, the Street-high target of $1,315 from BMO Capital suggests a gain of 29.5% from current levels, reflecting confidence in Costco’s ability to sustain growth, defend margins, and lean into its membership-driven model as industry pricing dynamics shift in its favor.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)