- Early Friday morning finds the commodity complex with a similar look to what we saw Thursday morning when Fear Of Inflation Long-term (F.O.I.L.) pulled markets higher.

- Gold and silver were showing gains pre-dawn, not surprising ahead of another uncertain weekend.

- The recent strength of distillates (heating oil, diesel fuel, etc.) has helped spark a strong rally in soybean oil which in turn has brought steady fund buying to soybeans.

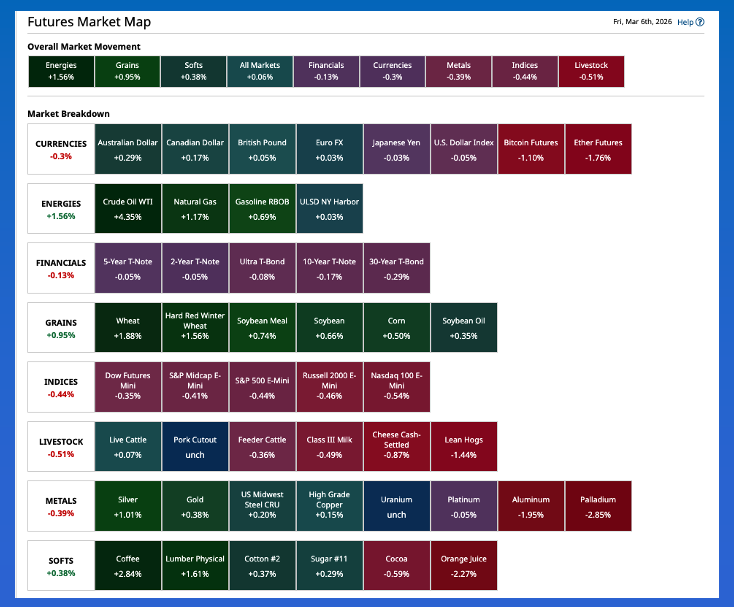

Morning Summary: If you liked Thursday’s session, then you’ll also get a kick out of what the quote screen has to show you early Friday morning. A quick glance at the Barchart Futures Market Heat Map shows Energies, Grains, and Softs leading the way higher while Metals and US stock index futures (Indices) are lower once again. As I talked about in yesterday’s Afternoon Commentary, all the pieces seem to be in place indicating a simple case of F.O.I.L. (Fear Of Inflation Long-term). It’s an understandable feeling as the Strait of Hormuz remains shut down, for the most part. It’s interesting to note the largest benefactor of the US action in Iran has been Russia, as buyers from around the world head toward the largest supplier of cheap oil. But then again, is anyone really surprised by this? Anyone? Bueller? Speaking of Energies, one of the small differences I see this morning is the spot-month distillates contract ((HOJ26) was showing a slight shade of red while the rest of the market was green again. Also, gold and silver were higher to start the day after crumbling during Thursday’s session. It would not be surprising to see these two key metals find increased buying interest heading into another uncertain weekend.

Soybeans: As for the soybean market, it was a case of Same Story, Different Day early Friday morning. The May issue added as much as 9.25 cents overnight on trade volume 21,000 contracts and was sitting 7.25 cents higher pre-dawn. There are a couple points of interest in this runaway train: First, the National Index (ZSPAUS.CM) came in near $11.0550 Thursday night, up about 9.75 cents and keeping the national average basis calculation near 73.75 cents under May futures. While merchandisers didn’t back away from the ongoing rally in the futures market, the basis market remains weak as it continues to run below the previous 5-year and 10-year averages. The latest weekly export sales and shipments update showed the US was on pace to ship 1.234 billion bushels (a fun number) as of Thursday, February 26, a point in the marketing year when the US has shipped an average 78% of what turns out to be total exports. Total commitments to China continue to run about 50% below the same week last year. The second point of interest will be this afternoon’s weekly Commitments of Traders report (legacy, futures only) to see if funds have pushed their net-long futures position beyond last fall’s peak of 254,090 contracts.

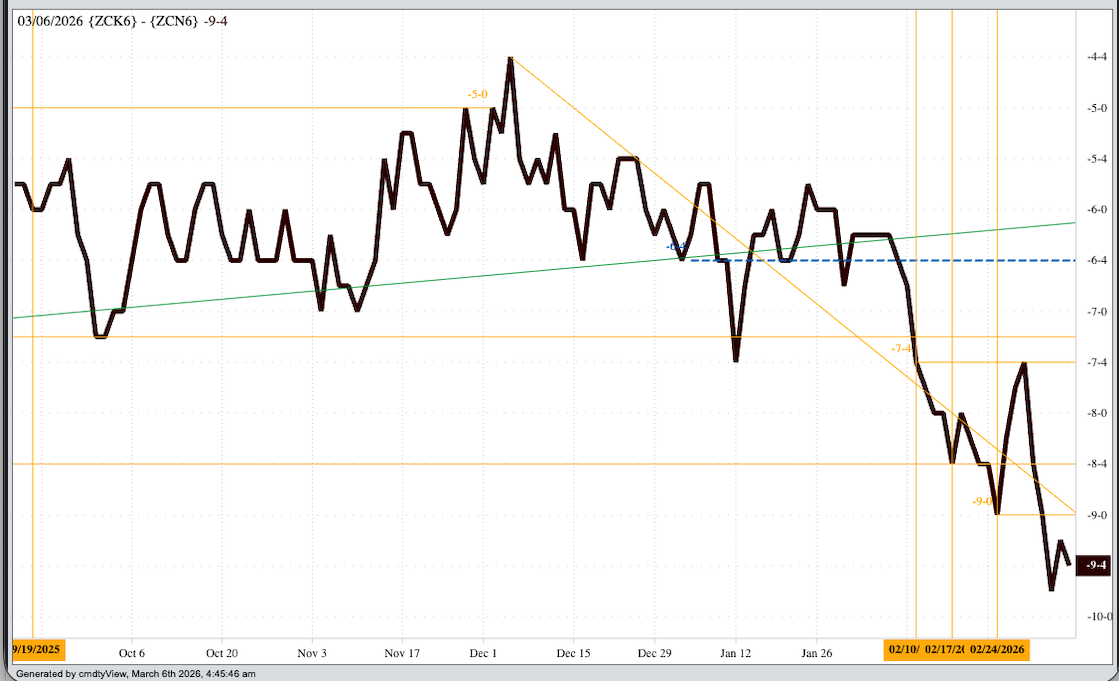

Corn: The corn market was higher early Friday morning on an uptick in overnight trade volume. My Blink[i] reaction is King Corn continues to be pulled higher by soybeans, which itself is being led by soybean oil, which in turn owes the incredible rally in distillates for its recent spike. In other words, corn doesn’t have a fundamental reason to be going up, but it is anyway, and as Market Rule #1 tells us, don’t get crossways with the trend. The May issue (ZCK26) gained as much as 2.75 cents overnight and was sitting one tick off its session high at this writing on trade volume of 36,000 contracts. Thursday evening saw the National Price Index come in near $4.1175, putting national average basis at roughly 41.75 cents under May futures. This is in line with last year’s calculation for this same week at about 41.0 cents under May. I’ll be keeping an eye on the May-July futures spread as Friday progresses to see if it posts another low daily close. The previous mark is 9.75 cents carry from this past Wednesday. The spread closed Thursday at 9.25 cents and covered a still neutral 45% calculated full commercial carry. Last year, the 2025 spread covered 30% this week.

Wheat: It was more of the same in the wheat sub-sector pre-dawn Friday with all three markets showing solid gains. Has wheat suddenly and miraculously turned fundamentally bullish? No, but it doesn’t matter at this time. As the old saying goes, “A rising tide lifts all boats”, until the holes in some of those vessels cause them to sink again. And the hole in the two winter wheat markets continues to be bearish long-term supply and demand. Turning the spotlight on new-crop markets we see July HRW (KEN26) is up another 8.25 cents at this writing, extending the uptrend on its weekly chart to a high of $6.1625, the highest price for a July HRW issue since the week of March 17, 2025. Thursday saw the July-September futures spread close at a carry of 14.25 cents and cover 63% calculated full commercial carry with the September-December covering 59%. Both are still leaning bearish. Over in SRW we see July (ZWN26) up 8.75 cents after adding as much as 12.0 cents overnight. Here the new-crop futures spreads covered a bearish 73% and 71%, based on the lower storage rate set to go into effect on March 19. We’ll see how new-crop markets finish the week given rains moving across the Plains and Midwest.

[i] Based on the Malcolm Gladwell book Blink, the theme being our initial thought is usually right before we spend time talking ourselves out of the decision.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)