/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

Sandisk (SNDK) has quickly emerged as one of the biggest beneficiaries of the artificial intelligence (AI) infrastructure boom. As hyperscalers and enterprises race to build out AI data centers, demand for NAND flash memory has surged, tightening supply and sending prices sharply higher. That powerful pricing environment has already translated into explosive earnings growth for memory producers—and now at least one analyst believes the upside may be far from over.

Lynx Equity Strategies analyst KC Rajkumar is making a bold call: he sees Sandisk generating between $90 and $100 in earnings per share (EPS) in 2026. But is this truly realistic, or is this another example of peak-cycle optimism in a historically volatile industry? Let's break down the supply-demand dynamics in the NAND market, examine pricing trends, and assess whether Sandisk can realistically deliver triple-digit earnings per share this year.

About Sandisk Stock

Sandisk Corporation is a leading developer and manufacturer of data storage devices and solutions based on NAND flash technology. The company was spun off from hard-drive manufacturer Western Digital (WDC) last year. It offers products such as solid-state drives (SSDs), removable memory cards (SD, microSD, CompactFlash), USB flash drives, and embedded storage for mobile and automotive applications. Sandisk’s storage chips, known as NAND flash memory, have become increasingly vital in AI data centers and consumer devices, fueling unprecedented growth for the company. SNDK’s market cap currently stands at $83.5 billion.

Shares of the data storage technology company have rallied 138% year-to-date (YTD), driven by overwhelming demand for its products. AI infrastructure investments are fueling massive demand for flash memory and pushing prices higher amid a very tight supply, significantly boosting Sandisk’s earnings and, in turn, its stock.

Can Sandisk Deliver $100 in EPS in 2026?

The rapid expansion of AI infrastructure is consuming a significant share of the available supply of NAND flash memory, DRAM, and hard drives. AI computing demands vast amounts of data at every stage of the process, with different types of storage serving different tasks. Sandisk’s storage chips are faster but more costly than hard drives, making them crucial for performance-critical workloads where minimizing bottlenecks is essential. Moreover, Nvidia’s next-generation AI servers will feature a significant increase in NAND storage capacity, which analysts estimate could consume as much as 10% of global NAND supply by 2027.

All of this is unfolding against the backdrop of a severe shortage in NAND flash memory supply. “Memory is in the midst of a generational supply and demand mismatch,” according to Morgan Stanley chip analyst Joe Moore. Limited supply is pushing prices higher and significantly boosting top and bottom lines for memory makers like Sandisk. In theory, a severe market shortage paired with soaring prices would typically prompt manufacturers to ramp up production sharply. However, let me explain why that may not necessarily be the case for memory companies.

The key point here is that the memory-chip industry has historically been cyclical, with periods of undersupply often followed by oversupply. With that, pricing downturns during periods of hardware oversupply can push producers into losses and weigh heavily on their stock prices. The most recent downcycle occurred in 2023, when Micron Technology, Western Digital, Seagate Technology (STX), and SK Hynix all posted annual operating losses. As a result, memory companies are cautious about expanding production capacity. It is also worth noting that Sandisk’s management said during the earnings call in late January that customers are now discussing a shift from quarterly agreements to multi-year deals with the company. That could give it greater confidence to make long-term investment decisions. Sandisk CEO David Goeckeler said at the fourth annual Bernstein TMT Forum last week that securing long-term agreements is key to reducing volatility in the industry.

But returning to the current situation, the market is facing a severe shortage of NAND flash memory supply that is expected to persist for several years. Lynx Equity Strategies analyst KC Rajkumar said the NAND flash supply shortage is likely to persist longer than the DRAM shortage. Rajkumar noted that while significant DRAM capacity is expected to come online by the second half of 2027, NAND flash buyers may have to wait until 2028. The analyst believes the supply-demand imbalance in the NAND flash market is unlikely to ease in the foreseeable future. And based on management’s comments from the FQ2 earnings call, Rajkumar said he is confident that 2026 earnings per share (EPS) could fall in the $90 to $100 range.

But just how realistic is Rajkumar’s projection? Well, it’s important to clarify that Rajkumar is likely referring to calendar year 2026, rather than the company’s fiscal year 2026, which runs through June. With that, calendar year 2026 would encompass the company’s Q3 and Q4 results for fiscal 2026, as well as Q1 and Q2 results for fiscal 2027. Sandisk’s average analyst estimate for adjusted EPS stands at $73.37 for the current calendar year, which is not far from Rajkumar’s projected range. And if the company continues to smash Wall Street expectations as it did in late January, Rajkumar’s numbers could even prove conservative. But let’s take a closer look at the details.

Once again, in a tight-supply market, a company’s profitability will depend heavily on pricing. And with no signs that demand for NAND flash memory will ease anytime soon, SNDK’s pricing is likely to strengthen further, fueling the company’s explosive earnings growth. UBS forecasts that NAND flash memory contract pricing will rise roughly 40% sequentially in the first quarter of 2026. Separately, BNP Paribas said on Wednesday that it expects memory pricing to keep rising amid strong AI-driven demand. “For NAND, we estimate CQ1 prices could increase 55% Q/Q, followed by 5% Q/Q increase in CQ2, predominantly driven by supply-side dynamics as NAND suppliers continue to shift capacity to enterprise storage products while remaining prudent on capacity additions,” said analyst Karl Ackerman. With that, Rajkumar’s $100 adjusted EPS projection for Sandisk in 2026 appears more than reasonable.

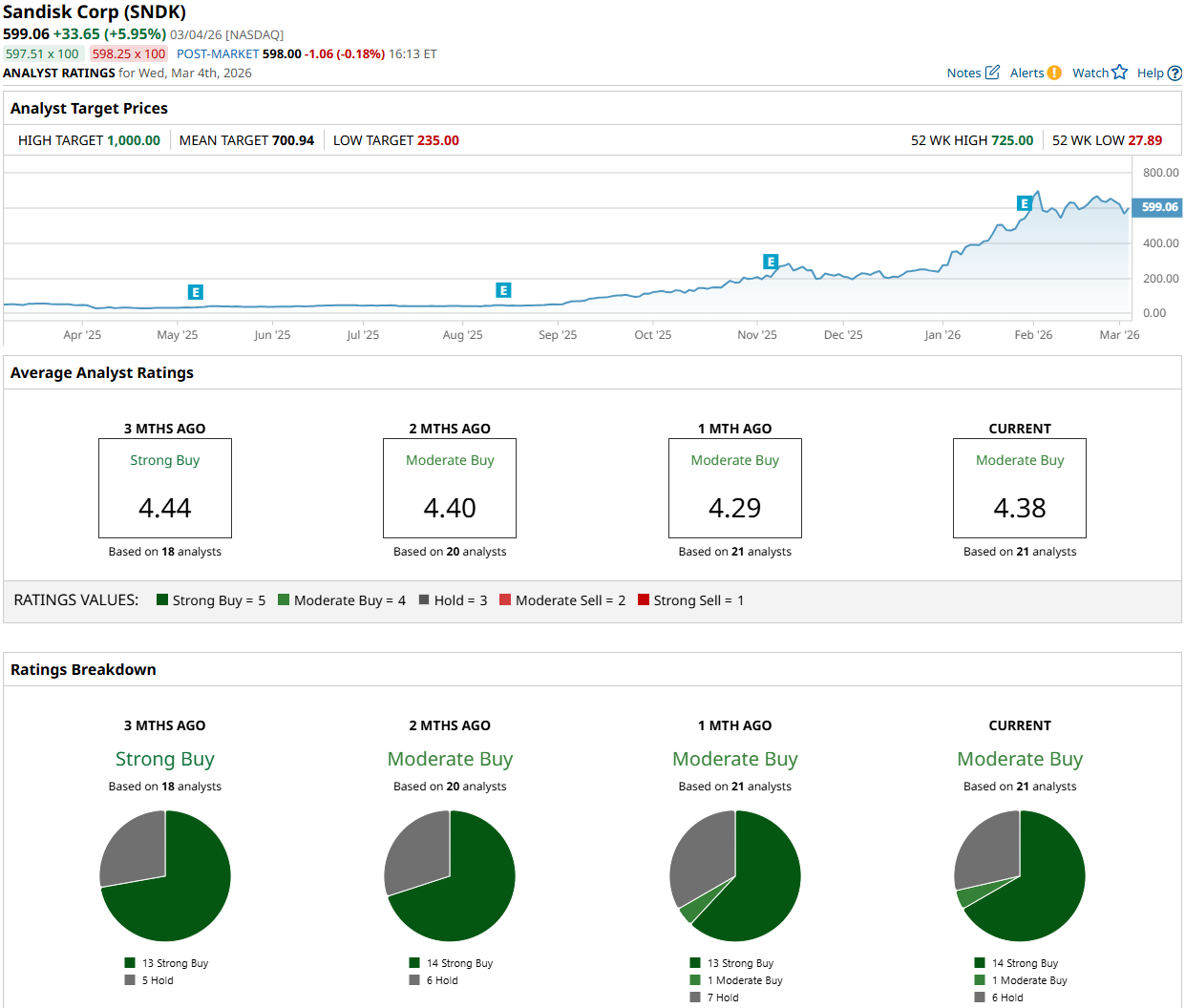

What Do Analysts Expect for SNDK Stock?

Wall Street analysts have a consensus rating of “Moderate Buy” on SNDK stock. Among the 21 analysts covering the stock, 14 recommend a “Strong Buy,” one advises a “Moderate Buy,” and the remaining six give a “Hold” rating. The average price target for SNDK stock is $700.94, implying a potential upside of 17% from current levels.

On the date of publication, Oleksandr Pylypenko did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)