Legal tech services provider LegalZoom.com (LZ) has been having a tough time on Wall Street. It has come under pressure, along with other software stocks, due to the rise of artificial intelligence (AI). The technology is now perceived as a hindrance to software companies, with a large-scale selloff triggered by the launch of Anthropic’s enhancements to its Claude large language model.

However, rather than opposing the rise of AI, LegalZoom has decided to incorporate it into its operations. Last month, the company announced that it’s integrating its attorney-services into the Claude ecosystem in an effort to challenge the traditional billable hour model. Against this backdrop, there might be a bull case for LegalZoom’s stock, as the Street-high price target of $11 implies a 57.8% upside. Should you buy the stock here?

About LegalZoom Stock

LegalZoom.com operates an online platform that delivers easy-to-use legal tech services for everyday people and small companies. Users can draft key documents, such as wills, trusts, business setups, and IP protections like trademarks, using self-guided tools, often skipping full attorney involvement.

The firm blends smart software, expert guidance, and lawyer referrals for cost-effective solutions on a simple site. Based in Glendale, California, LegalZoom streamlines personal and business legal tasks. The company has a market capitalization of $1.22 billion.

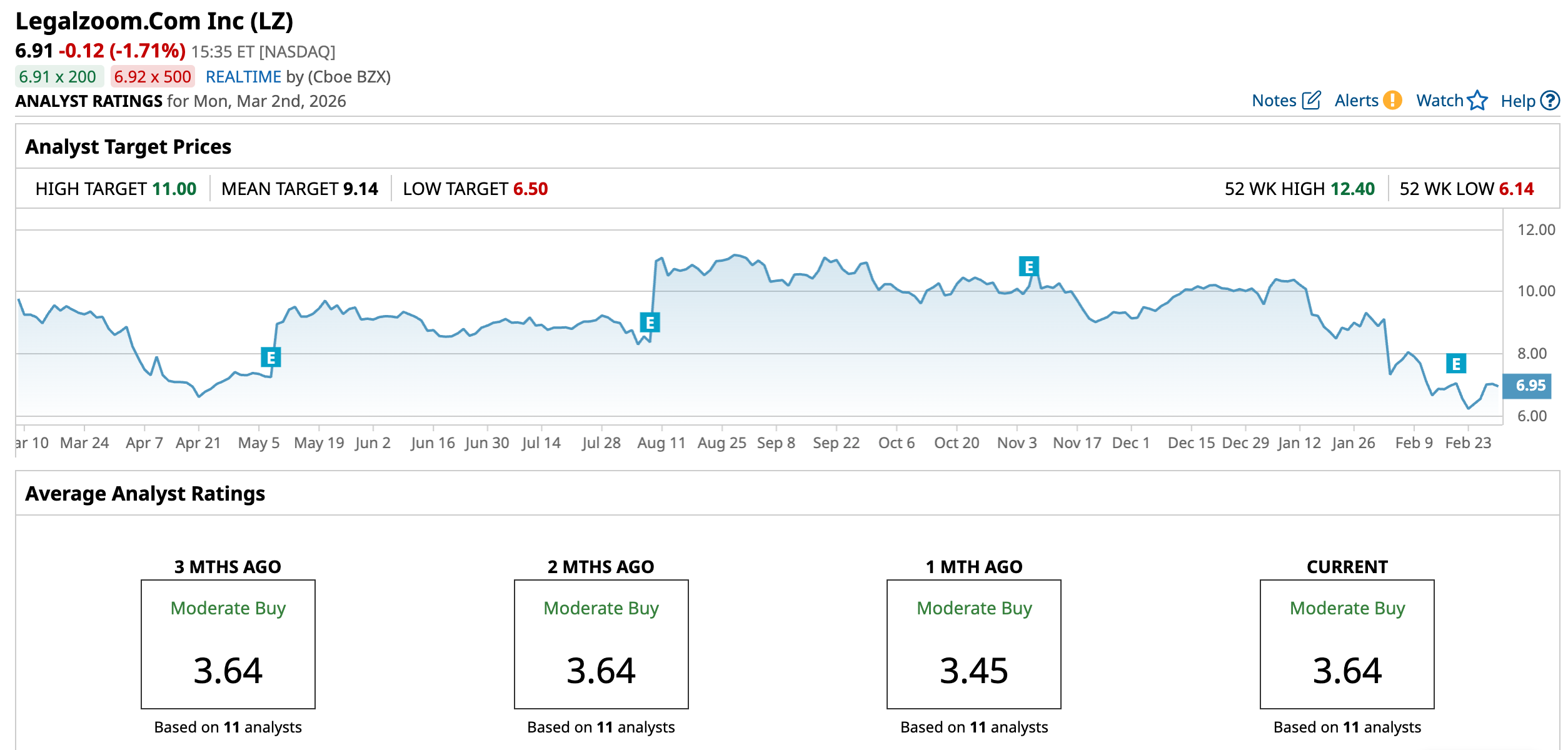

Declining margins and profitability concerns have caused a downturn in the stock price, as LegalZoom faces challenges amid fears of disruption from agentic AI technologies. LegalZoom’s stock has declined 31.6% over the past 52 weeks, while it has been down 30% year-to-date (YTD). Just for comparison, the broader S&P 500 Index ($SPX) has gained 15.8% and marginally over the same periods, respectively. The company’s shares had reached a 52-week low of $6.14 on Feb. 24, but are up 13% from that level.

The selloff has made the stock significantly cheaper. On a forward-adjusted basis, its price-to-earnings ratio of 9.66x is lower than the industry average of 21.33x.

LegalZoom Reports Strong Q4 Revenue Beat Amid Margin Squeeze

On Feb. 19, LegalZoom reported its fourth-quarter results, which were a mixed bag. The company’s total revenue increased 18% year-over-year (YOY) to $190.27 million, which was higher than the $184.30 million that Wall Street analysts had expected. Its average order value for the quarter was 13% higher than what it was a year ago, at $248.

Average revenue per subscription unit (at period end) increased by 1% YOY to $266. LegalZoom’s subscription revenues continue to show robust growth, increasing by 20% from the prior-year period to $130.95 million. In fact, the company’s 2025 results reflected an emphasis on subscription initiatives and contributions from the Formation Nation acquisition.

However, LegalZoom’s margins have come under pressure. Its Q4 net income margin dropped from 8% to 3%. The company’s non-GAAP EPS was $0.17 for the quarter, down 11% YOY and lower than the $0.18 that analysts had expected.

For the current year, LegalZoom expects an 8% YOY revenue growth (at the midpoint of the guidance range), with a focus on higher-value customer acquisition and differentiated human-in-the-loop service offerings. However, this implies a step down from the 11% YOY growth observed in 2025.

On the other hand, Wall Street analysts expect LegalZoom’s profitability to improve this year. For fiscal 2026, analysts expect the company’s EPS to grow by 285.7% YOY to $0.27, followed by a 51.9% expansion to $0.41 in fiscal 2027.

What Do Analysts Think About LegalZoom’s Stock?

Last month, JP Morgan's analyst Ella Smith maintained an “Overweight” rating, but lowered its price target from $14 to $11. But, this still remains the Street-high price target. Just a couple of days later, analysts at UBS maintained a “Neutral” rating on LegalZoom’s stock but lowered its price target from $12 to $8, despite the company’s strong Q4 results, with four consecutive quarters of accelerating subscription revenue growth. However, the company’s fiscal 2026 revenue growth is projected to slow as improvements in average revenue per user take over from expansion in customer units.

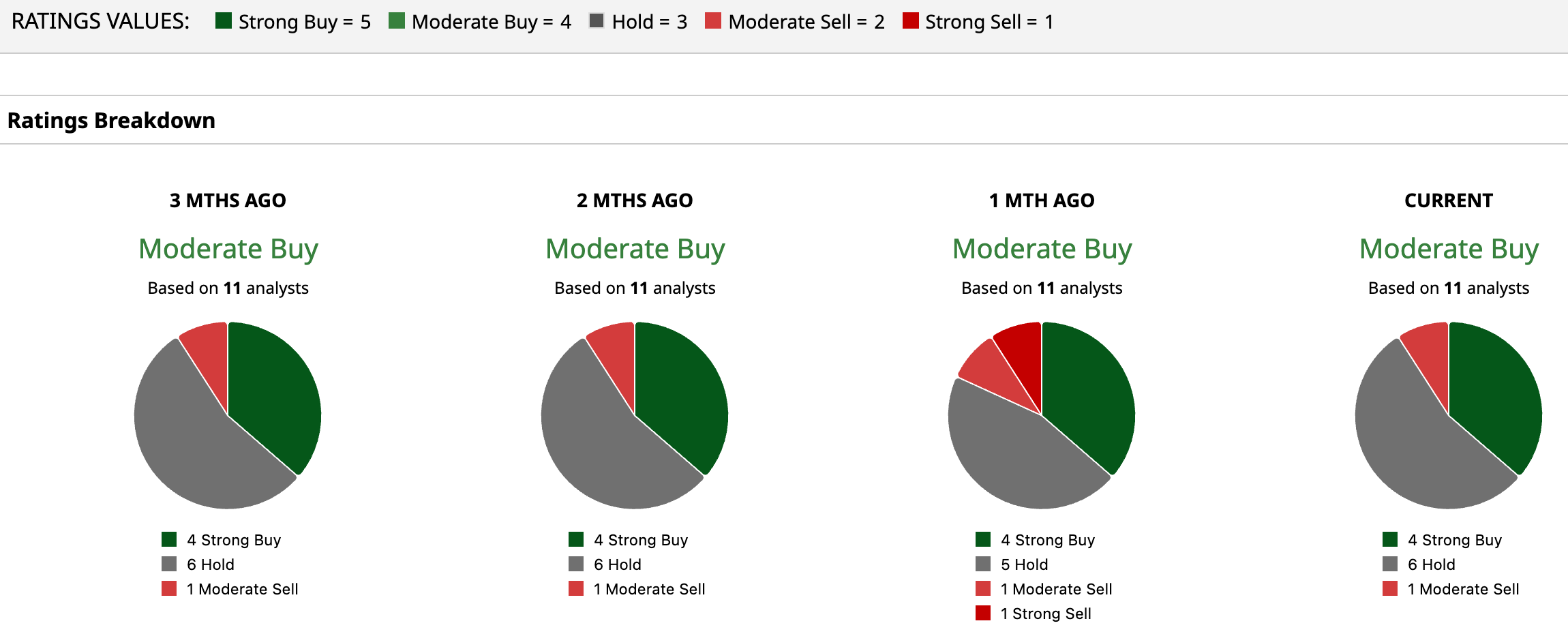

LegalZoom is well-liked on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating. Of the 11 analysts rating the stock, four analysts have given it a “Strong Buy” rating, while six analysts are taking the middle-of-the-road approach with a “Hold” rating, and one suggested “Moderate Sell.” The consensus price target of $9.14 represents a 30% upside from current levels. Moreover, as already stated, the Street-high JPMorgan-given price target of $11 implies a 56.5% upside.

Key Takeaways

The concerns about AI causing a downturn in software demand might be a bit overblown. We see that when it comes to LegalZoom, its subscription revenue keeps growing, and the integration of its attorney services into the Claude platform indicates that the company is leaning into the AI boom. Therefore, while the stock remains beaten down, it might be an opportune time to get in.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)