/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

The expectations around the companies associated with the AI trade are so high that merely beating the ones on the Street is not enough anymore. Even if there is the slightest hint of a miss, shares are getting whacked, with no consideration given to the fact that demand remains solid and growing at a rapid pace, and the companies are reporting record revenues, profits, and cash flows.

The latest casualty of this phenomenon: Advanced Micro Devices (AMD).

About AMD

Founded in 1969, AMD is a fabless semiconductor company producing high-performance compute and graphics solutions. AMD is diversified across PCs, data centers, gaming, embedded systems, and AI, giving exposure to multiple large markets (including the fast-growing AI silicon market).

Valued at a market cap of $394.2 billion, the AMD stock is up 72% over the past year. However, shares were down by more than 17% in yesterday's trading session as some analysts on the Street expected a stronger guidance from the Lisa Su-led company.

So, should serious investors pay heed to this downturn or double down on AMD stock now? Let's find out.

AMD's Sensational Q4

AMD's results for Q4 2025 handily beat Street expectations on both the bottom line and the topline, as the company reported record quarterly revenues. Revenues were up 34% from the previous year to $10.27 billion, with the data center segment witnessing revenues of $5.4 billion. Not only was this up 39% yearly, but it also came in much higher than the consensus estimate of $4.97 billion. The other key segment of Client and Gaming saw its revenues surge by 37% in the same period to $3.9 billion.

Earnings went up by 40% from the corresponding period a year ago to $1.53, easily outpacing the consensus estimate of an EPS of $1.32. Notably, this marked the fifth consecutive quarter of earnings beat from the company.

Coming to the much-talked-about guidance, AMD forecasted revenues for Q1 2026 to be in the range of $9.5-$10.1 billion, the midpoint of which would denote an annual growth rate of 32%. However, this includes about $100 million of AMD Instinct MI308 chip sales to China, which remain uncertain.

Notably, along with an improvement in gross margins to 57% from 54% in the year-ago period, cash flow from operations remained solid as well. For the quarter ended Dec. 27, 2025, net cash provided by operations increased to $2.6 billion from $1.3 billion, with the company closing the quarter with a cash balance of $5.5 billion. This towered over its short-term debt levels of just $874 million.

Yet, notwithstanding its strong fundamentals, AMD continues to trade at punchy levels. Its forward P/E, P/S, and P/CF at 36.63, 8.63, and 53.10 are all above the sector medians of 23.65, 3.36, and 17.95, respectively. However, its forward PEG ratio, which takes into account AMD's future growth rate, makes the stock look relatively reasonable. Standing at 0.79, it is lower than the sector median of 1.52.

What Comes Next?

AMD’s current development pipeline is heavily focused on an annual cadence for AI accelerators to compete with Nvidia’s (NVDA) Blackwell and Rubin cycles while simultaneously pushing into the 2nm node for its next generation of CPUs. However, the developments that the stakeholders are most excited about are around the Instinct MI400 Series and the Helios Platform.

Shedding light on the Instinct MI400 Series first, it represents a fundamental shift in AMD's strategy. While the MI300 and MI350 focus on memory capacity, the MI400 is moving to the TSMC (TSM) 2nm (N2) process node and debuting the CDNA 5 architecture. How is it better? Well, just in terms of raw compute, the upcoming series of chips will deliver 40 PFLOPS (Floating-Point Operations Per Second) (FP4) and 20 PFLOPS (FP8). This is a 2x jump over the MI350 series and a staggering 10x improvement over the original MI300X.

In terms of memory, it is the first AMD chip to use HBM4, jumping to 432GB of capacity and 19.6 TB/s bandwidth. It allows researchers to fit massive trillion-parameter models on a single GPU (or fewer chips), drastically reducing the "latency tax" of moving data between chips. Moreover, by moving to the 2nm node, it is expected that there will be a 25–30% reduction in power at the same performance level compared to 3nm. Because AMD is doubling performance, the real-world benefit is a significant reduction in the Total Cost of Ownership (TCO) related to cooling and electricity.

Meanwhile, the Helios Rack-Scale system (integrating 72 MI400s) is designed with liquid cooling as a primary requirement to manage the high thermal density, aiming to outperform Nvidia’s GB200/NVL72 systems in energy efficiency for long-running training jobs. Additionally, because Helios has significantly more memory (31 TB vs. 20 TB), it can handle larger Mixture-of-Experts (MoE) models without needing to send data across the slower data center network. This reduces latency and power waste. Notably, analysts suggest Helios provides a lower TCO because it uses standard Ethernet networking, which is cheaper to maintain and scale than Nvidia's specialized fabrics.

The developments on the CPU front also remain solid, with the Zen 6 "Morpheus" & EPYC “Venice.” Particularly, Venice increases core counts to 256 cores/512 threads per socket (up from 192 in Turin). This represents a 30% increase in thread density, specifically targeting hyperscale cloud providers. Notably, Venice will be the first EPYC to support 12-channel (and potentially 16-channel) DDR6 memory and PCIe Gen 6, significantly reducing the data bottleneck for AI-heavy workloads.

Finally, AMD is no longer treating software as a secondary concern. The release of ROCm 7.0 (late 2025) and 7.2 (January 2026) signals a move toward a "universal" AI software stack. ROCm 7.0 reportedly delivers a 3x throughput improvement for AI training compared to ROCm 6, purely through software optimization and better kernel management. Further, the integration of Triton 3.3 allows developers to write code that is "vendor-agnostic." This is a direct attack on Nvidia’s CUDA lock-in, as it makes porting models from Nvidia to AMD nearly instantaneous.

Analyst Opinion on AMD Stock

So, a lot is going on for AMD, and most of it is in its favor. Agreed, it still trails Nvidia by a wide margin in terms of GPU market share, but it is taking rapid strides and gaining its own share as well. Additionally, not just GPU, AMD is looking to compete with its bigger peer across the full-stack of AI solutions, and so far, they are making a pretty good case for it.

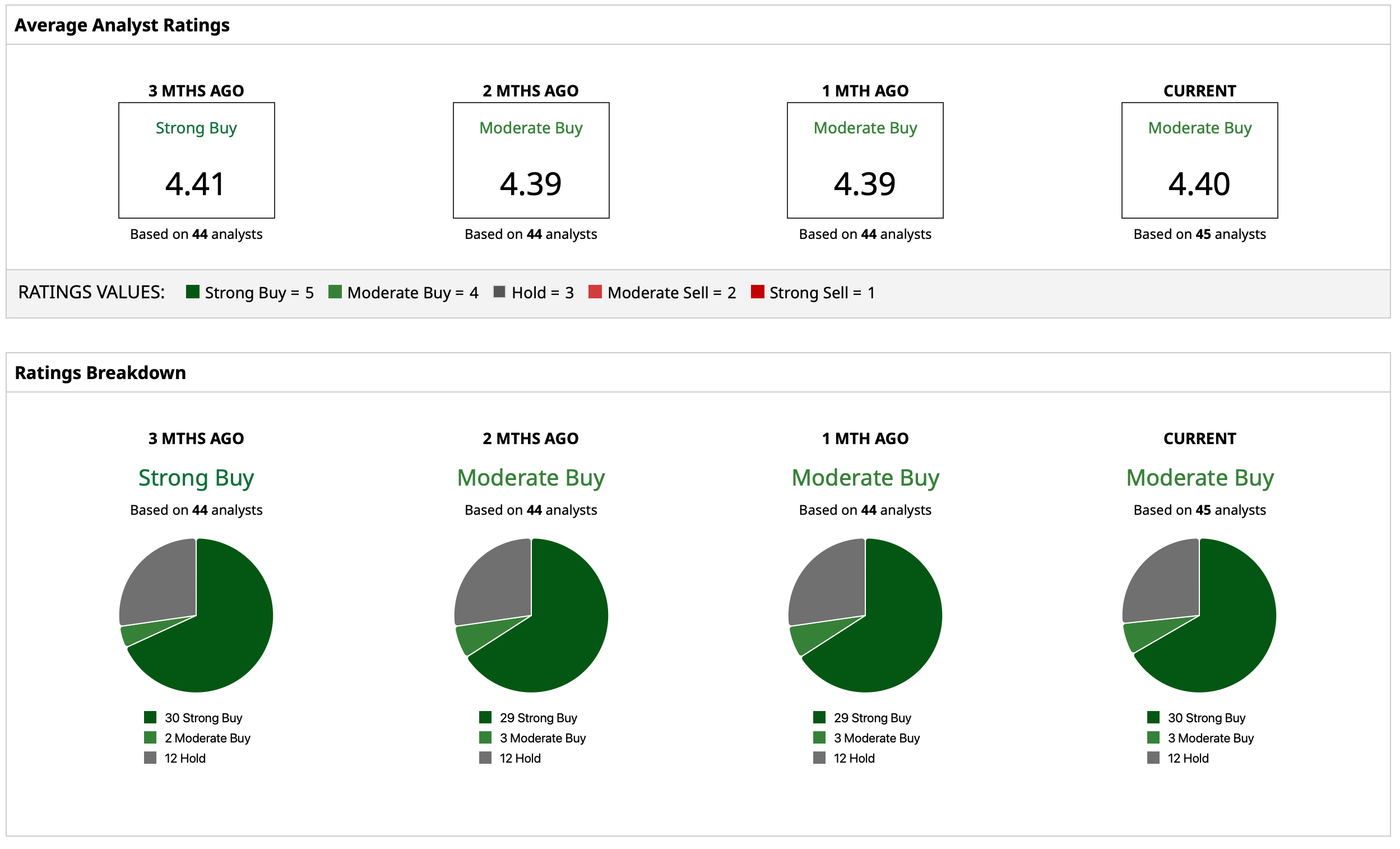

Considering this, analysts remain cautiously optimistic about AMD stock, giving it a consensus rating of “Moderate Buy.” The mean target price of $288.56 indicates an upside potential of about 47% from current levels. Out of 45 analysts covering the stock, 30 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and 12 have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/AI%20microchip%20by%20DesignKingBD360%20via%20Shutterstock.jpg)