With a market cap of $57.3 billion, Digital Realty Trust, Inc. (DLR) owns, acquires, develops, and operates data centers, providing colocation and interconnection solutions to a broad range of domestic and international customers. As of September 30, 2025, the company operates 311 data centers across multiple continents, supporting mission-critical technology and enterprise operations with a portfolio of approximately 42.7 million square feet of stabilized space.

Shares of the Austin, Texas-based company have underperformed the broader market over the past 52 weeks. DLR stock has dropped 1.4% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 12.2%. However, shares of the company are up 6.5% on a YTD basis, outpacing SPX’s marginal drop.

Zooming in further, shares of the REIT have slightly less pronounced decline than the State Street Real Estate Select Sector SPDR ETF’s (XLRE) 1.8% dip over the past 52 weeks.

Shares of Digital Realty rose 2.2% following its Q3 2025 results on Oct. 23. The company reported stronger-than-expected core FFO of $1.89 per share and revenue of $1.58 billion. Investors also reacted positively to solid operating momentum highlighted by $201 million in new annualized bookings, an expanded $852 million backlog, and 8% cash rental rate growth on renewals. In addition, management raised full-year 2025 core FFO guidance to $7.32 per share - $7.38 per share.

For the fiscal year that ended in December 2025, analysts expect DLR’s core FFO to rise 9.5% year-over-year to $7.35 per share. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

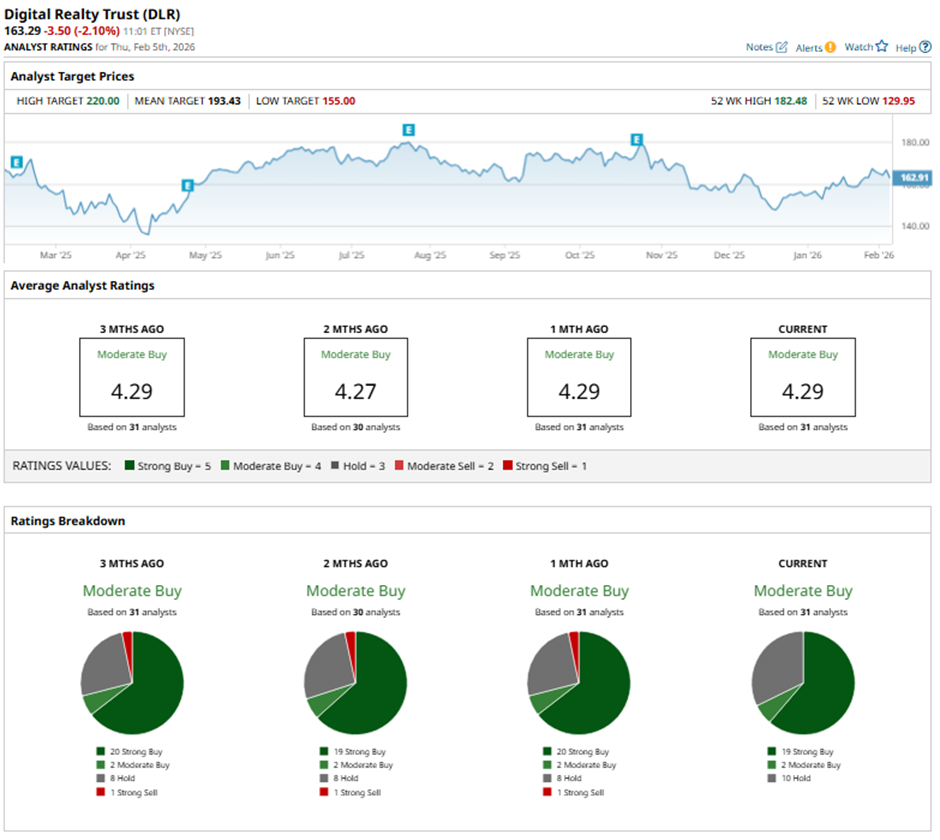

Among the 31 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 19 “Strong Buy” ratings, two “Moderate Buys,” and 10 “Holds.”

This configuration is slightly less bullish than three months ago, with 20 “Strong Buy” ratings on the stock.

On Jan. 14, Scotiabank cut its price target on Digital Realty to $189 while maintaining an “Outperform” rating.

The mean price target of $193.43 represents a 18.5% premium to DLR’s current price levels. The Street-high price target of $220 implies a potential upside of 34.7% from the current price.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)