Since I’m a risk manager first and foremost, my career has led me to be naturally skeptical of “moonshot” moves in stocks and exchange-traded funds (ETFs). It kept me out of trouble by not chasing stocks like Oracle (ORCL) and Advanced Micro Devices (AMD) in recent months. But it costs me on the other end.

As with the iShares Asia 50 ETF (AIA). This has been my go-to for non-Japan Asia investing. I like its simple, 50-stock, market-cap-weighted structure. I’ve owned it a few times over the years, but not recently. Because I find the global stock market too highly correlated to be excited about drifting very far from where the market’s core is — the S&P 500 Index ($SPX), and the Dow ($DOWI) and Nasdaq ($NASX).

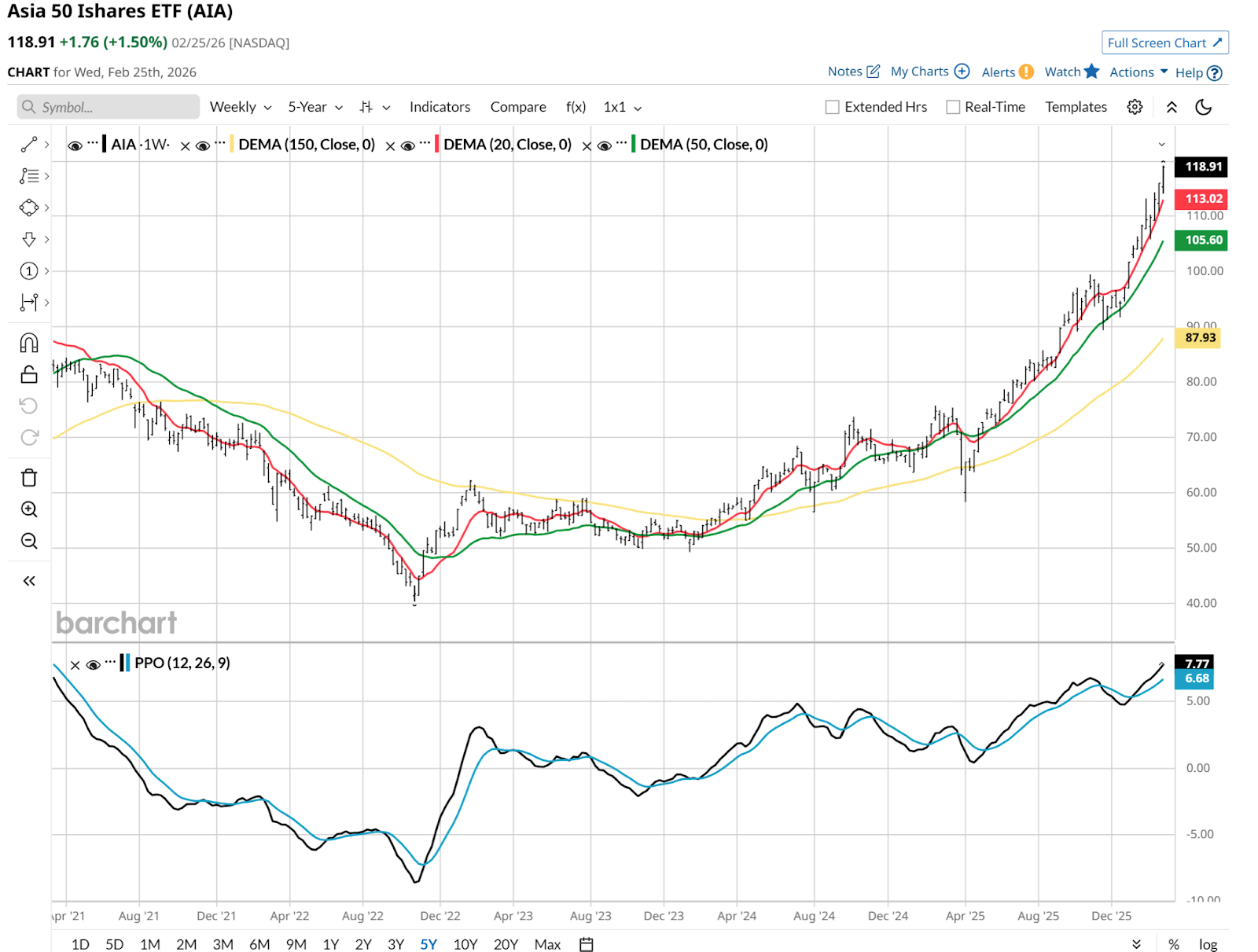

That hardened view on risk management can also cost some upside. I will miss moves like the one we just saw in AIA. It bucked the recent trend and flew higher without the U.S. markets leading it. And after a more than 30% move from $90 in late November to nearly $119 at Wednesday’s close, the fair question is whether AIA and the non-Japan Asia equity market is now the leader.

I’d describe the above chart of weekly prices as not yet peaking. That doesn’t mean it can’t soon. That’s the market climate we live in. But the other price-based factor to point out is perhaps the biggest bullish argument I can make for ETFs like AIA, and Asian stocks more broadly. It might be making up for a lot of lost time.

Why AIA’s Rally Might Not Be Over

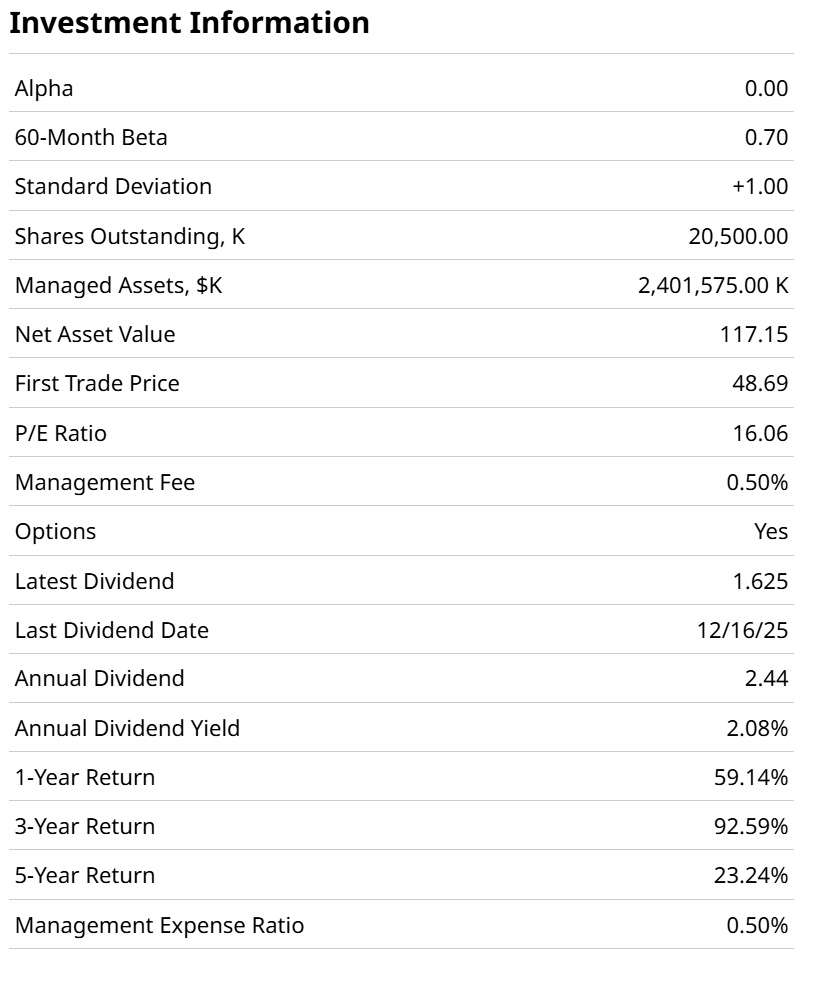

AIA put up a “goose egg” from April 2021 through August of 2025, more than four years of about zero return. And the current portfolio price-to-earnings (P/E) ratio of 16x tells me that it was around 12x to 13x not long ago. That is long-term bottoming territory for a market like this.

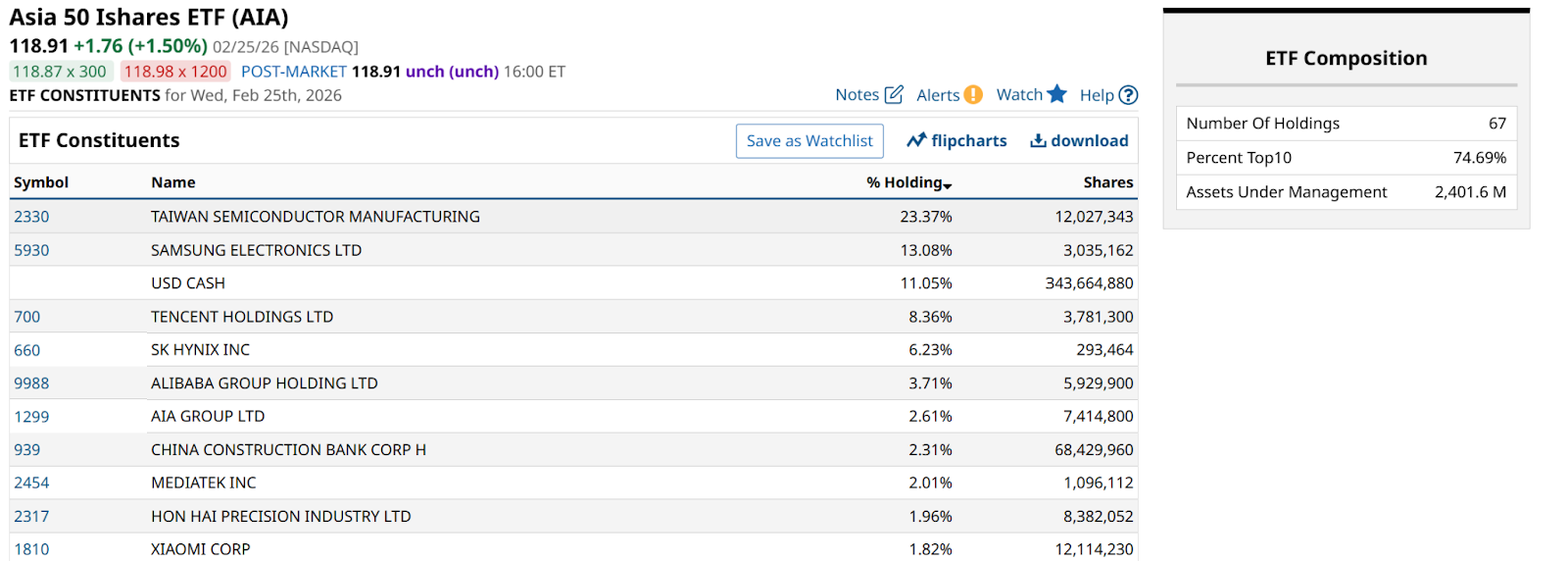

AIA owns the economic heavyweights of the Pan-Asian region by tracking the 50 largest and most liquid companies across China, Hong Kong, South Korea, Singapore, and Taiwan. The fund is heavily anchored by the technology sector, which accounts for more than half of its market value. This concentration makes it a primary vehicle for expressing a regional view on Asian growth, particularly as it relates to the global artificial intelligence buildout. It may also be a solid diversifier from U.S. tech.

The geographic composition of the fund is dominated by mainland China, Taiwan, and South Korea, which together represent more than 85% of the total allocation. At the stock level, while this ETF owns 67 holdings, just 10 account for three-quarters of assets.

So, as with many equity ETFs, you are not buying a “market,” you are buying a handful of big players. The rest are really just accounting entries. They do not often move the full portfolio’s value.

The current run for AIA is supported by improving fundamentals across its core markets, particularly in South Korea and Taiwan where earnings growth expectations are high due to semiconductor demand. South Korea has emerged as a particularly high-conviction area for 2026, with some analysts projecting substantial surges in Korean equities driven by record-high foreign capital inflows and a cyclical upswing in exports.

Going forward, the key impacts on AIA’s performance range from the impact of currency fluctuations, as a declining U.S. dollar historically provides a tailwind for capital inflows into Asian market, to the evolving regulatory landscape in China and how the growth of application-led platform companies might diverge from the hardware-led growth seen in Taiwan and Korea. And of course, there’s the high return and risk potential when you have so few stocks crowding the fund’s asset base.

I ran a ROAR analysis on AIA, and it points out what I said at the top of this article. Its ROAR score turned green (70 or above) last May around $75 a share. That was the easy part, in hindsight.

There was another lower-risk signal on Oct. 10, 2025, around $91. But as is often the case in my risk-management-dominant system, as the spike in price occurred, AIA’s ROAR score lost value. It remains in the neutral risk zone (ROAR score of 40), but trees don’t grow to the sky, as they say.

Yogi Was Right

What’s next? I am not a binary investor, trying to predict the future, which as Yogi Berra once said, is very difficult. What I can say about AIA is that the makings are there for a continued run. And ROAR assigned a 40% chance of the next major move being up, not down. But that also means a 60% chance the next big move is down.

Such is life for a risk manager. That’s why perhaps the way to look at this and other “stretched in price” ETFs is to consider owning it in smaller than normal size. What’s normal? That’s up to every investor.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/McDonald's%20Corp%20arches%20by-%20TonyBaggett%20via%20iStock.jpg)