Matt Cerminaro, the brains behind Chart Kid Matt, published his latest chart on Feb. 24. Entitled The Craziest Stat Of 2026, it highlighted something very interesting.

More importantly, it gave me a story idea about U.S.-listed stocks hitting new 52-week highs and lows from Tuesday’s trading.

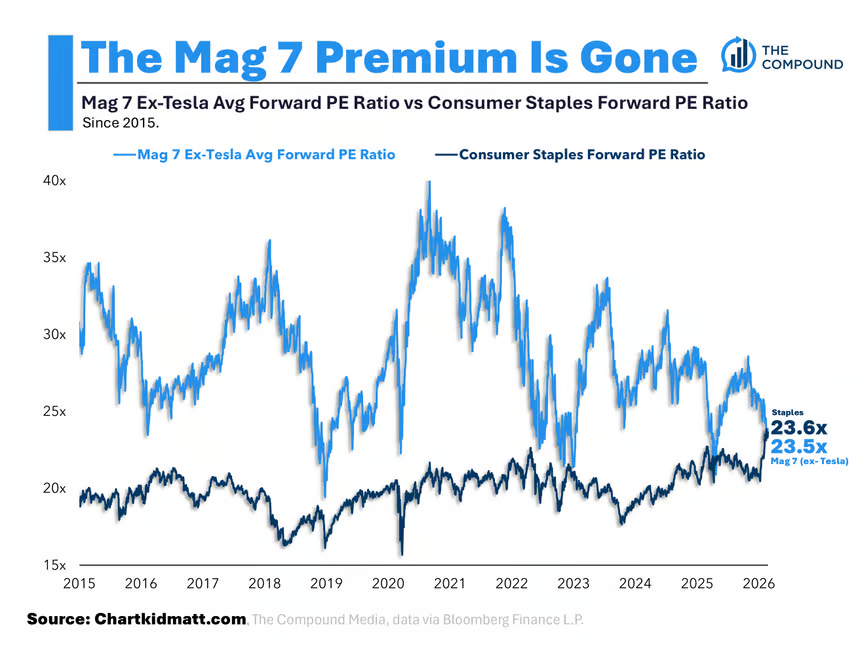

The main point of Cerminaro’s post and chart is that the average forward P/E of the Magnificent 7, excluding Tesla (TSLA), is now below the Consumer Staples sector.

And there you have it.

The consumer staples forward P/E ratio of 23.6x is 1 basis point higher than the average forward P/E for the six Mag 7 stocks excluding Tesla. That might not seem like much, but when you consider that the spread was close to 20x in 2020, this is a massive convergence.

Which leads me to yesterday’s new 52-week highs and lows.

The NYSE had 171 new 52-week highs and 79 new 52-week lows, while the Nasdaq had 226 new 52-week highs and 220 new 52-week lows. Among the 397 stocks hitting new 52-week highs, I counted 11 consumer staples stocks, but there’s probably more that I missed.

Meanwhile, excluding Tesla, none of the six other Mag 7 stocks hit new 52-week lows yesterday. However, and this is or isn’t a coincidence, all six of the stocks have set between 11 and 14 new 52-week lows over the past 12 months.

So, today, I’ll suggest three of the 11 consumer staples stocks to sell and which Mag 7 stocks you should redeploy capital into.

Sell Mama’s Creations (MAMA) and Buy Nvidia (NVDA)

Mama’s Creations (MAMA) hit a new 52-week high of $17.42 on Tuesday, its 42nd of the past 12 months. Its shares are up 28.8% in 2026 and 180.8% in the past year.

The smallest of the three stocks, with a market cap of $707 million, is a New Jersey-based fresh deli prepared foods company that provides its family of brands, including MamaMancini’s, T&L Creative Salads, Olive Branch, and others, to over 12,000 stores in the U.S.

Its primary goal is to become a one-stop shop deli solution with annual sales of $1 billion. It plans to reach that goal through organic sales initiatives and accretive strategic acquisitions.

In the fourth quarter, its latest acquisition was Crown 1 Enterprises Inc., a manufacturer of value-added proteins and ready-to-eat meals. It paid $17.5 million in cash for the former Sysco (SYY) subsidiary. The acquisition adds $56 million in annual revenue. Crown 1 brings an upgraded 42,000-square-foot production facility to the company.

In the past five years, its annual revenues have grown by 221.2% from $47.1 million in fiscal 2021 (January year-end) to $151.3 million for the 12 months ended Oct. 31, 2025. At the same time, it went from an operating loss of $100,000 in 2021 to an operating profit of $7.2 million as of Q3 2025.

While there’s no question it’s growing, its $704.5 million enterprise value is 66.4 times its EBIT (earnings before interest, taxes, depreciation and amortization) for the next 12 months, according to S&P Global Market Intelligence.

As an aside, I recommended MAMA stock in July 2024, when it traded around $7.50. I wouldn’t be offended if you didn’t sell. It is an excellent holding for aggressive investors. I just think its share price could cool off as we move through 2026.

On the other hand, Nvidia's (NVDA) enterprise value is 22.4 times its EBIT for the next 12 months. Over the past 20 quarters, its forward EV/EBIT multiple has been this low only three times: Q4 2025, Q1 2025, and Q4 2023.

With Jensen Huang as its CEO, I’m confident it will continue to grow. You’re getting growth at a reasonable price.

Sell Monster Beverage (MNST) and Buy Microsoft (MSFT)

Monster Beverage (MNST) hit a new 52-week high of $85.59 on Tuesday, its 56th of the past 12 months. Its shares are up 11.6% in 2026 and 64.1% in the past year.

I’ve followed the company for a long time; it was called Hansen’s Natural when I first came across it. A consortium of investors led by CEO Hilton Schlosberg and Chairman Rodney Sacks acquired the company in 1992 for $14.6 million.

After a few years of losses, they came upon Red Bull in Europe and decided to create a U.S. energy drink. We know the rest of the story.

As consumer staples stocks go, you don’t get long-term performance that’s much better than Monster -- its shares are up 2,127% since the turn of the century, a 34.3% compound annual growth rate.

Analysts generally like MNST stock. Of the 23 analysts that cover it, 13 rate it a Buy (4.09 out of 5), with a target price of $82.23, a few dollars below its current share price.

If you don’t already own it, I’d wait for a better entry point or use cash-secured puts to achieve the same goal. Its valuation is high. Based on the Wall Street earnings estimate of $2.29, its share price is 37.2 times this forecast, which is higher than it’s been in the past five years.

Monster reports Q4 2025 earnings after today’s close. I don’t think there will be anything too surprising. On the bottom line, it has beaten the analysts’ estimate in the past two quarters by 4.10% and 9.22%, respectively. It should probably beat in single digits again.

However, even with a third consecutive beat, its shares are already richly valued. Any bad economic news and down it goes. If you already own shares and want to hold for the long haul -- you can’t argue with success -- married puts would help protect any unrealized gains you might have.

Meanwhile, among the six Mag 7 stocks, Microsoft (MSFT) has the lowest EV/NTM EBIT at 18.17x. It hasn’t been this low since Q2 2019.

The company’s relationship with OpenAI, albeit fractured at times, remains on track. Last October, the two companies reported how the next chapter of their partnership -- which has been ongoing since 2019 -- will proceed.

The two most important parts: 1) OpenAI will purchase $250 billion in Azure services from the company, and 2) Microsoft will receive 20% of OpenAI’s revenue through 2032.

While Microsoft gave up some control over OpenAI’s future spending on computing power, its investment in the AI company is now valued at $135 billion and likely to move higher in the years ahead.

Its shares won’t be this reasonable for too much longer.

Sell Casey's General Stores (CASY) and Buy Meta Platforms (META)

Casey's General Stores (CASY) hit a new 52-week high of $684.61 on Tuesday, its 46th of the past 12 months. Its shares are up 23.3% in 2026 and 61.2% in the past year.

It’s been a long time since I’ve considered the pros and cons of the Iowa-based convenience store operator. When I last seriously followed CASY stock over a decade ago, Casey’s was busy fending off a $1.9 billion hostile takeover from Alimentation Couche-Tard (ANCTF). This Canadian convenience store giant flirted with buying Japan’s Seven & I Holdings (SVNDF) and its 7-Eleven subsidiary for nearly a year before throwing in the towel last July.

A lot’s changed about Casey’s and the convenience store industry in the 16 years since. For starters, Casey’s has grown from a small-cap stock into a decent-sized mid-cap, with a market cap about 13 times higher than Couche-Tard’s 2010 offer.

Convenience store consolidation continues. Casey’s has participated in this trend. In late 2024, it acquired 148 CEFCO stores in Texas and an additional 50 in Alabama, Florida and Mississippi, paying $1.1 billion. The acquisition greatly strengthened its position in the southern U.S.

Since the acquisition, the company has spent the past year assessing all of the CEFCO locations and comparing its prepared foods, grocery, and general merchandise operations to Casey’s.

CEO Darren Rebelez believes that once these locations are rebranded as Casey’s, the CEFCO stores will deliver higher margins. The company will spend $150 million converting the CEFCO locations to Casey’s branding.

Analysts like what the company’s doing. Of the 17 analysts covering its stock, 10 rate it a Buy (4.18 out of 5). However, the 12-month target price of $639.50 is below its current share price.

The obvious appeal to investors: whether it’s as a consolidator or consolidated by a larger buyer, its shares are likely to receive a nice premium in the future. That would suggest the downside in the near term is minimal.

Casey’s EV is 27.4 times its NTM EBIT compared to 17.0 times Alimentation Couche-Tard’s. It can’t afford any mistakes.

Meanwhile, you can buy Meta Platforms (META) for 18.5 times its NTM EBIT. And even though there is a lot to dislike about Mark Zuckerberg and his company, you can’t deny that the $43.6 billion in 2025 free cash flow (21.7% FCF margin) it generated isn’t impressive.

You pay 27.4 times NTM EBIT for Casey’s stock or 32% less for one of the world’s trillion-dollar companies. Based on valuation, I’d go with the latter.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)