/Chubb%20Limited%20magnified%20website-by%20Pavel%20Kapysh%20via%20Shutterstock.jpg)

Chubb Limited (CB) is a leading global insurer, specializing in property and casualty coverage, personal lines, and tailored specialty protection. The company offers commercial and personal insurance policies, reinsurance, and comprehensive risk management solutions, leveraging strong underwriting skills, a diverse product portfolio, and extensive distribution channels for businesses and individuals worldwide.

Headquartered in Zurich, Switzerland and with a market capitalization of $122.37 billion, Chubb maintains a vast international presence across numerous countries. The company is expected to report its fourth-quarter results for fiscal 2025 soon. Ahead of the release, Wall Street analysts are optimistic about the company’s bottom-line trajectory.

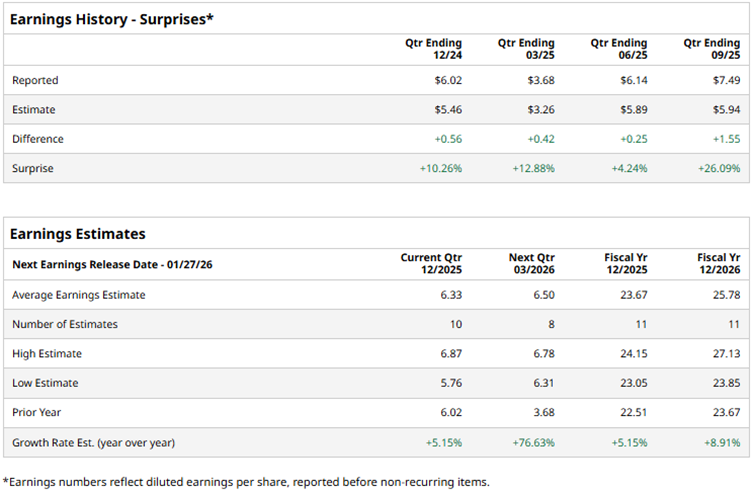

Analysts expect Chubb to report a profit of $6.33 per share on a diluted basis in Q4, up 5.2% year-over-year (YOY). The company has a solid history of surpassing consensus estimates, topping them in all four trailing quarters. Analysts also expect the company to improve its bottom line this year. For the full fiscal year 2025. Wall Street analysts expect Chubb’s diluted EPS to grow by 5.2% annually to $23.67.

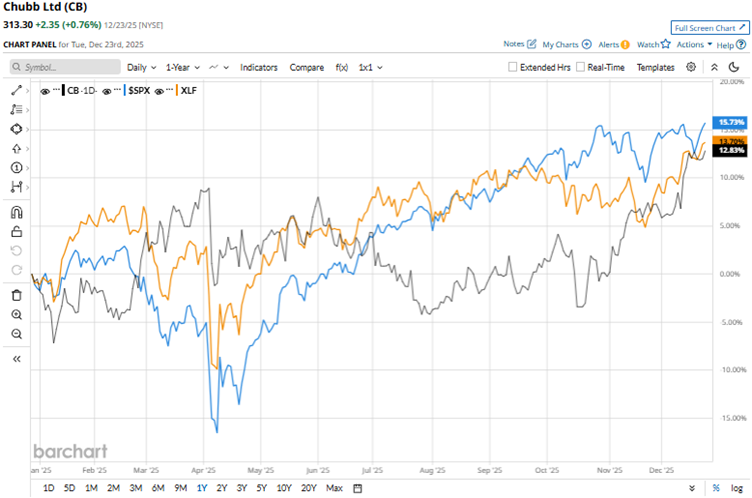

Chubb’s stock has been underperforming the broader market over the past year. Over the past 52 weeks, the stock has gained 13.8%, and over the past six months, it has been up 8.7%. On the other hand, the broader S&P 500 Index ($SPX) has increased by 15.7% and 14.7% over the same periods, respectively.

Next, we compare the stock with its own sector’s performance. The State Street Financial Select Sector SPDR ETF (XLF) has gained 14.5% over the past 52 weeks and 9.1% over the past six months. Therefore, the stock has also underperformed its sector over these periods.

On Oct. 21, Chubb reported its third-quarter 2025 results, showing robust growth. The company reported a 7.5% increase in net premiums written to $14.87 billion. In the P&C segment, net premiums written increased by 5.3% YOY to $12.93 billion. Its underwriting income also increased robustly, which added to its growth. Chubb’s net income for the quarter was $2.80 billion, up 20.5% annually. After this result, the stock gained 2.7% intraday on Oct. 22.

Wall Street analysts have been bullish about Chubb’s future. Among the 26 analysts covering the stock, the consensus rating is “Moderate Buy.” The ratings configuration has remained roughly unchanged over the past month, except for the addition of one extra “Hold” rating. The stock has nine “Strong Buys,” one “Moderate Buy,” 14 “Holds,” one “Moderate Sell,” and one “Strong Sell” rating.

The mean price target of $313.54 implies negligible upside from current levels, while the Street-high price target of $364 implies 16.2% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)