/Technology%20abstract%20by%20TU%20IS%20via%20iStock.jpg)

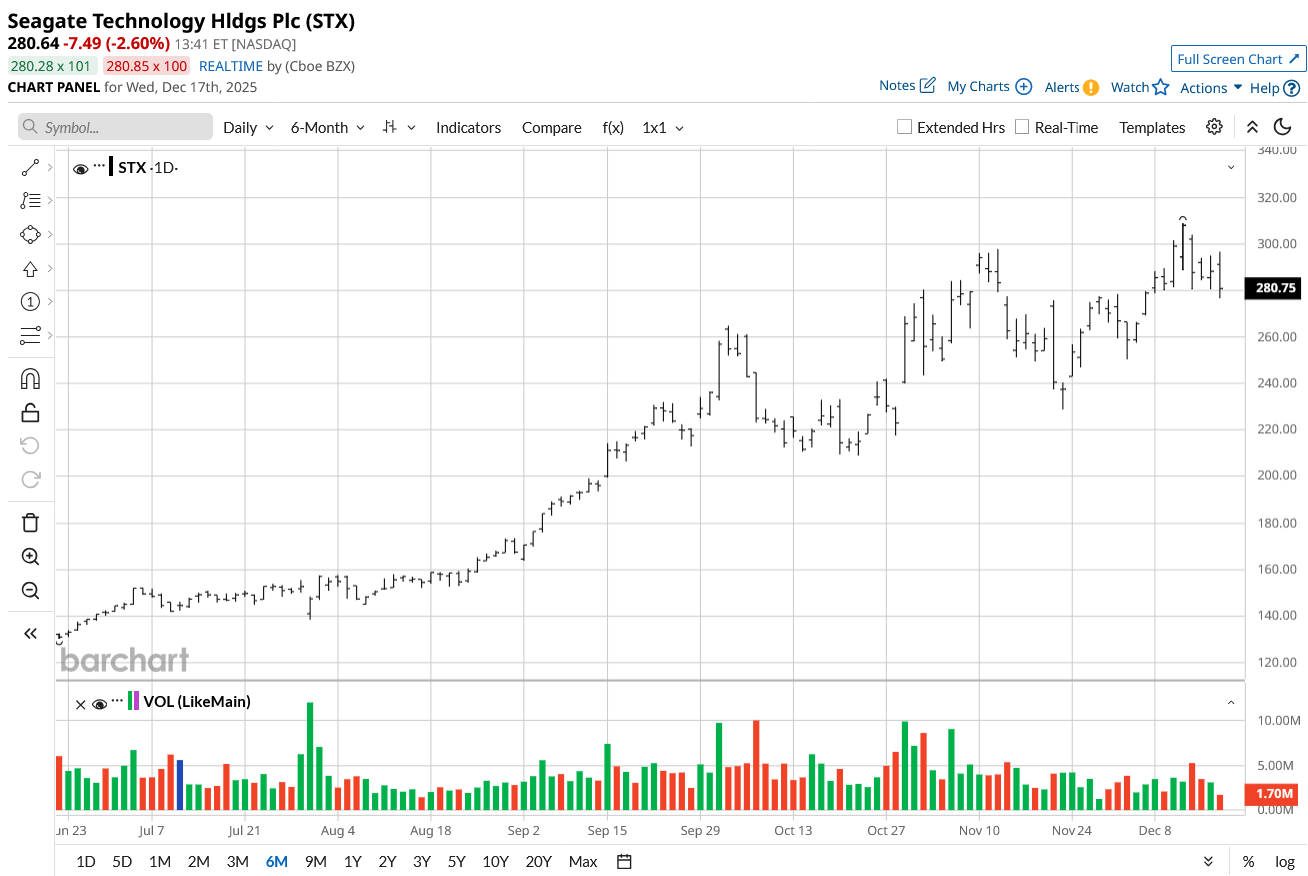

Seagate (STX) stock is yet another AI tailwinds-driven winner that has outperformed with returns of 225% for the year. While the rally has been significant, forward valuations remain attractive considering the growth outlook.

The good news continues to flow with the recent announcement that STX stock will be added to the Nasdaq-100 Index after the annual reconstitution. This is likely to translate into buying activity, as funds tracking the Nasdaq-100 Index will also realign their portfolios.

Of course, that’s not the only reason to be positive. The strong demand for HDDs is likely to translate into healthy revenue growth coupled with margin expansion.

About Seagate Stock

Seagate, headquartered in Fremont, California, is a provider of mass-capacity data storage. The company’s product portfolio includes enterprise nearline hard disk drives, enterprise nearline solid-state drives, and enterprise nearline systems, among others.

For Q1 2026, Seagate reported healthy revenue growth of 21% on a year-on-year (YoY) basis to $2.63 billion. Further, the company has guided for revenue of $2.7 billion for Q2 2026, which is likely to be supported by strong data center market demand.

With healthy growth, robust cash flows, and positive industry tailwinds, STX stock has surged by 115% in the past six months.

Strong Fundamentals and Growth Outlook

With healthy revenue growth, Seagate has witnessed sustained improvement in credit metrics. As of Q1 2026, the company reported $1.1 billion in cash. Further, with an undrawn credit facility of $1.3 billion, the total liquidity buffer stands at $2.4 billion.

While Seagate reported gross debt of $5 billion, it’s unlikely to be a concern considering the fact that leverage is low at 1.5x. The interest coverage ratio for the same period was healthy at 8.6x.

It’s also worth noting that for Q1 2026, the company reported operating and free cash flow of $532 million and $427 million, respectively. This implies an annualized FCF potential of $1.7 billion.

Seagate offers an annualized (FWD) dividend of $2.88 per share. With swelling cash flows, it’s likely that dividends will increase. At the same time, the company has been creating value through share repurchase.

Besides these factors, high financial flexibility allows Seagate to invest in innovation-driven growth. The company is already ramping up shipments of areal density-leading Mozaic HAMR products. This product has been validated and certified by the world’s five largest cloud customers.

Additionally, Mozaic 4+ HAMR-based drives are likely to see volume ramp-up in the second half of FY 2026. It’s worth noting that Seagate expects more than 50% gross margin over the next 12 months for HDD sales. With higher volumes coupled with margin expansion, the earnings growth outlook is likely to be robust.

Coming back to innovation, Seagate believes that advancing areal density is the key factor that gives a competitive edge. The company is already working on technologies like silicon photonics to “pave the path to 10 terabytes per disk.”

What Analysts Say About STX Stock

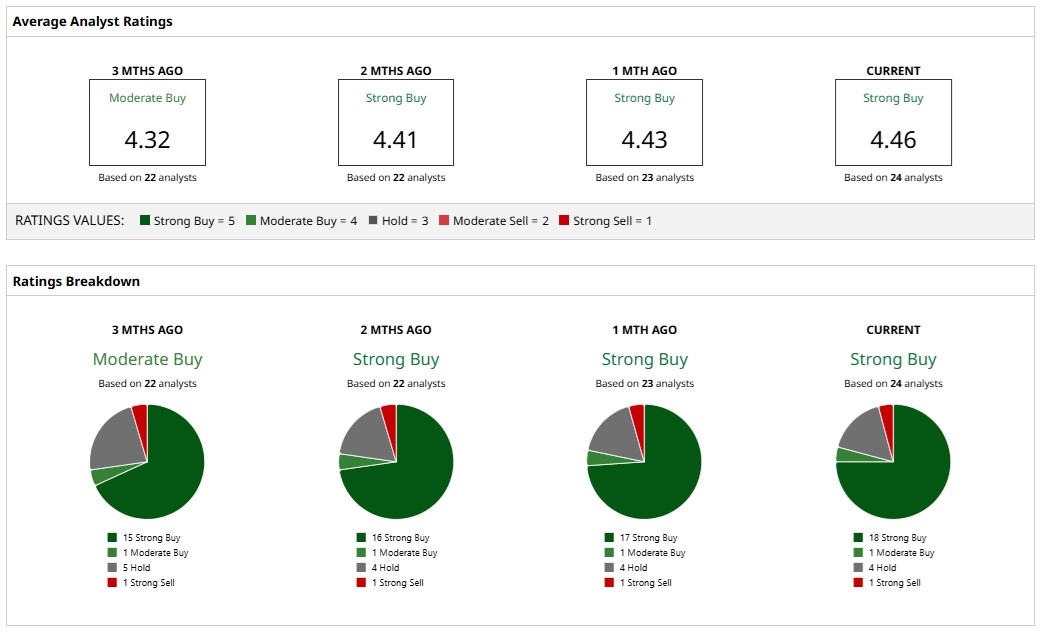

Based on the rating of 24 analysts, STX stock is a consensus “Strong Buy.”

While 18 analysts have assigned a “Strong Buy” rating, one and four analysts have a “Moderate Buy” and “Hold” rating, respectively. Additionally, one analyst believes that STX stock is a “Strong Sell.”

Based on these ratings, the analysts have a mean price target of $293.86. This would imply an upside potential of 5%. Furthermore, considering the most bullish price target of $465, the upside potential is 66%.

While Seagate stock has witnessed a significant rally, Morgan Stanley recently reiterated its “Overweight” rating. This view is backed by the forecast that Seagate is positioned to deliver an EPS of $17 for FY 2027. This is supportive of the company’s $341 bull-case price target and would imply an upside potential of 22%.

Assuming an EPS of $17, STX stock is trading at a forward (FY 2027) price-earnings ratio of 16.8. This does not indicate stretched valuations for a story with positive tailwinds.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)