/Molina%20Healthcare%20Inc%20logo%20on%20phone-by%20T_Schneider%20via%20Shutterstock.jpg)

Molina Healthcare, Inc. (MOH), headquartered in Long Beach, California, runs managed care plans for low-income families and individuals via Medicaid and Medicare programs. It delivers community-focused health services across various U.S. states. The company has a market capitalization of $7.78 billion.

Rising costs in the Medicaid and Medicare segments, alongside the Trump administration’s changes to the Affordable Care Act (ACA), have led Molina’s stock to decline. Over the past 52 weeks, the stock has dropped 48.2%, while it is down 13% year-to-date (YTD). The stock had reached a 52-week low of $121.06 on Feb. 11 but is up 24.7% from that level, having somewhat recovered, gaining 19.2% over the past five days.

On the other hand, the broader S&P 500 Index ($SPX) has gained 13% over the past 52 weeks and marginally YTD, indicating that the stock has underperformed the broader market. Next, we compare the stock with its own sector. The State Street Health Care Select Sector SPDR ETF (XLV) has increased 6.5% over the past 52 weeks and 1.3% YTD. Therefore, the stock has underperformed its sector over these periods.

On Feb. 5, Molina Healthcare reported mixed fourth-quarter results for fiscal 2025. The company’s total revenue increased 8.3% year-over-year (YOY) to $11.38 billion (topping analysts’ expectations), driven by premium revenue rising 7.3% annually to $10.72 billion.

On the other hand, Molina reported an adjusted loss per share of $2.75 (missing the analysts’ consensus estimate), a huge decline from the $5.05 EPS it reported a year earlier. Actually, the company’s bottom line was pressured by approximately $2.00 of unfavorable retroactive revenue items.

For the current year, the company expects premium revenue of about $42 billion (down 2% from 2025) and adjusted EPS of at least $5.00 on a diluted basis. Wall Street analysts expect MOH’s EPS to decrease 54.3% YOY to $5.04 on a diluted basis for fiscal 2026, followed by a 146% improvement to $12.40 in fiscal 2027. The company has missed consensus estimates in three of the four trailing quarters.

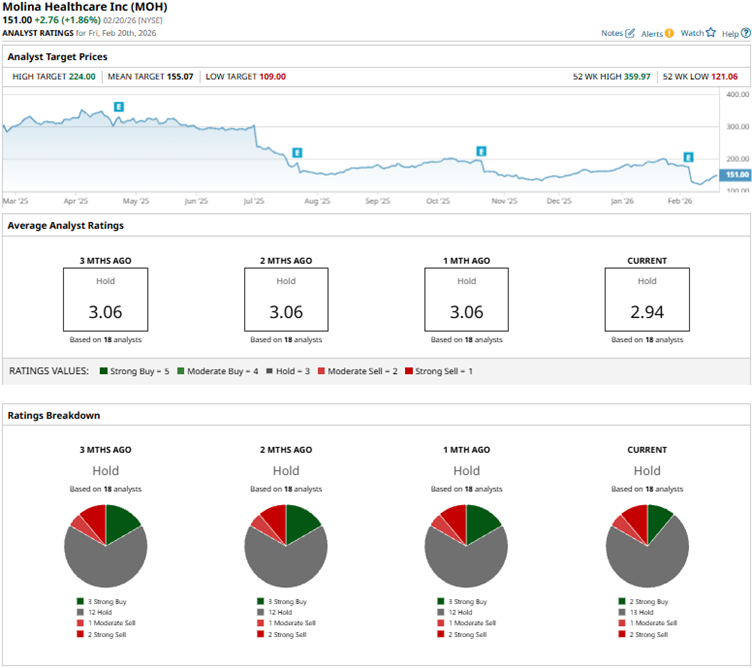

Among the 18 Wall Street analysts covering Molina Healthcare’s stock, the consensus is a “Hold.” That’s based on two “Strong Buy” ratings, 13 “Holds,” one “Moderate Sell,” and two “Strong Sells.” The ratings configuration has become less bullish than a month ago, with two “Strong Buy” ratings, down from three.

This month, analysts at Wells Fargo downgraded Molina’s stock from “Overweight” to “Equal Weight” and cut the price target from $208 to $141, citing underwhelming Q4 results and the volatility surrounding the company’s revenue stream, which exhibits reduced confidence about Molina’s ability to maintain positive Medicaid profits amid operational challenges.

MOH’s mean price target of $155.07 indicates a 2.7% upside over current market prices. The Street-high price target of $224 implies a potential upside of 48.3%.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)