/EPAM%20Systems%20Inc%20website%20and%20logo%20on%20phone-by%20T_Schneider%20via%20Shutterstock.jpg)

Headquartered in Newtown, Pennsylvania, EPAM Systems, Inc. (EPAM) engineers digital platforms and delivers software development services. With a market cap of around $7.7 billion, the company drives cloud transformation, artificial intelligence (AI) and data initiatives, cybersecurity, and experience design. EPAM also leads product development, system modernization, testing, deployment, and ongoing operational support.

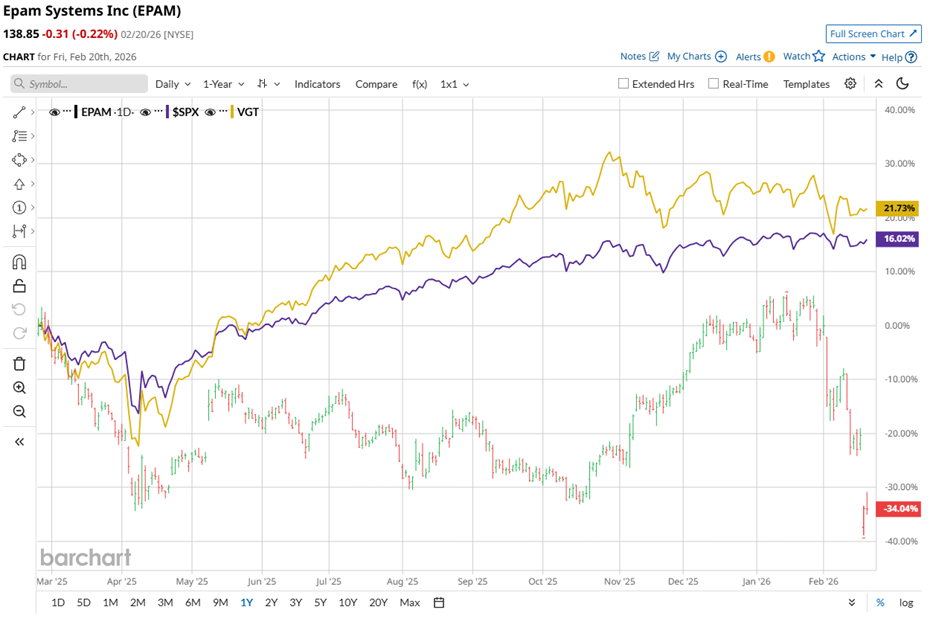

Over the past 52 weeks, EPAM stock slid 38.3%, while the S&P 500 Index ($SPX) surged roughly 13%, leaving the shares trailing broader market gains. Year-to-date (YTD), the decline continues with a 32.2% drop, as the index ekes out modest growth.

Sector comparisons reinforce the underperformance narrative. The Vanguard Information Technology Index Fund ETF Shares (VGT) gained around 15% over the same 52-week period, while YTD, it fell only 2.2%, considerably less than EPAM Systems’ steep losses.

Feb. 19 marked a defining moment for EPAM Systems as it reported Q4 fiscal 2025 earnings. Revenue surged 12.8% year over year to $1.41 billion, topping analyst expectations of $1.39 billion, while adjusted EPS climbed 14.8% to $3.26, surpassing the Street's $3.16 forecast. Yet, despite these strong results, the market reacted sharply, punishing the stock.

Shares plunged more than 17% on Feb. 19, leading S&P 500 decliners, after the company projected full-year organic revenue growth of 3% to 6%, slightly below the 6.3% consensus. Management pointed to margin pressures from higher compensation and heavier investment cycles, as the company sharpens industry-specific expertise and expands go-to-market capabilities.

Looking forward, EPAM Systems remains confident in its AI-native services, aiming for over $600 million in AI-driven revenue in fiscal 2026. While demand for advanced AI deployments and large-scale transformation projects remains strong, the company acknowledged that longer procurement cycles and more rigorous client evaluations could slow revenue conversion.

For fiscal year 2026, ending in December, analysts forecast diluted EPS growth of 9.2% to $9.85, reflecting steady momentum. Notably, EPAM has beaten EPS estimates in all four trailing quarters, signaling consistent operational execution and a knack for outperforming expectations even amid market volatility.

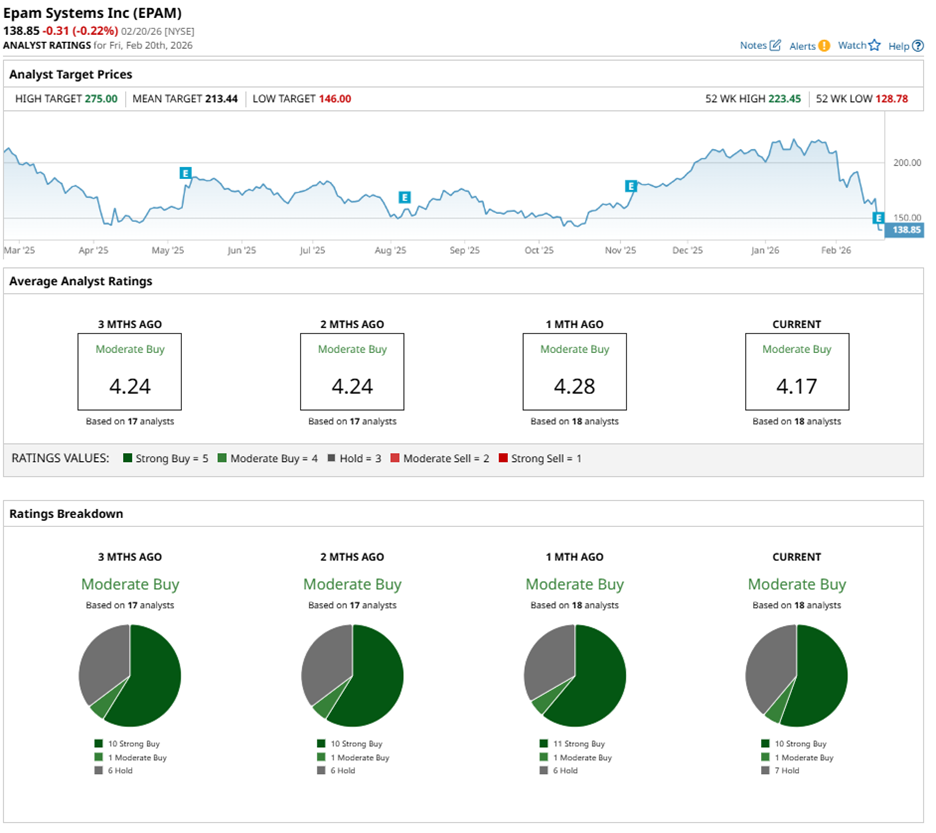

Wall Street currently assigns EPAM stock an overall rating of “Moderate Buy.” Among 18 analysts, 10 have issued a “Strong Buy” rating, one recommends “Moderate Buy,” while seven call for “Hold.”

Analyst sentiment remains steady, mirroring the stance from three months ago when 10 analysts also endorsed the stock with a “Strong Buy” rating.

On Feb. 20, The Goldman Sachs Group, Inc. (GS) analyst James Schneider trimmed EPAM’s price target to $235 from $250 but reaffirmed his “Buy” rating, noting that the market overreacted to Q4 results. He emphasized that, despite isolated client-specific headwinds, EPAM continues to see an improving business outlook, underscoring resilience in its growth trajectory.

That being said, the mean price target of $213.44 implies potential upside of 53.7%, while the Street-high target of $275 represents a gain of 98.1% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nike%2C%20Inc_%20swish%20by-%20Tartezy%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Businessman%20touching%20the%20brain%20working%20of%20Artificial%20Intelligence%20(AI)%20Automation%20by%20Suttiphong%20Chandaeng%20via%20Shutterstock.jpg)