/The%20logo%20for%20ASML%20on%20a%20corporate%20office%20by%20Skorzewiak%20via%20Shutterstock.jpg)

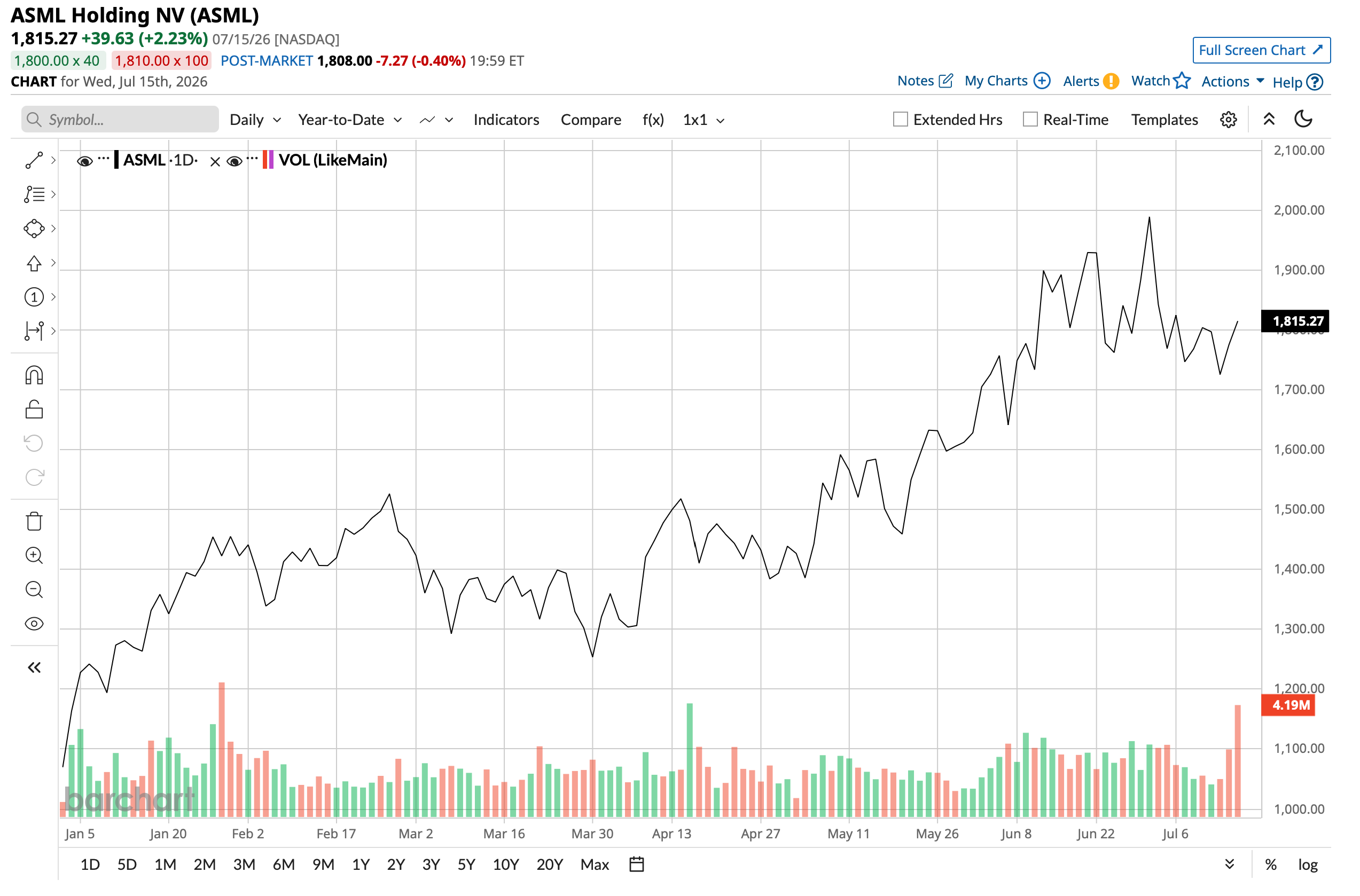

ASML (ASML), the artificial intelligence (AI) infrastructure company known for its monopoly in extreme ultraviolet lithography (EUV) systems, just reported another set of upbeat numbers for its latest quarter. Not only did ASML report a beat on both revenue and earnings, but it also raised its revenue and gross margin guidance as the unprecedented demand for memory becomes a new point of growth for the company.

Right now, the cause of all the excitement around ASML stock is due to its print for the second quarter of fiscal 2026. Could ASML be a wise investment option for the long term at current levels? Let's take a closer look.

About ASML

Based in the Netherlands and founded in 1984 as a joint venture between Philips and ASM International, ASML builds the photolithography machines that chipmakers use to print microscopic circuit patterns onto silicon wafers. In fact, ASML holds a near-monopoly in EUV lithography, the technology required to manufacture the world's most advanced chips at leading-edge process nodes.

Valued at a market capitalization of about $702 billion, ASML stock is already up 66% so far this year. Meanwhile, the stock also offers a dividend yield of 0.59%, with dividends growing consecutively for years. With a payout ratio of 23.85%, further headroom for growth remains.

ASML Keeps Rolling in Q2

ASML's recent Q2 results ticked all the boxes that an investor base craves. The period was marked by revenue and earnings growth, along with raised sales and gross margin guidance for the year.

ASML reported revenue of €9.3 billion in Q2, up 21% year-over-year (YOY). Net system sales, the core revenue segment of the company that includes the sale of EUV machines, rose more than 17% to €6.6 billion, while service and field options sales came to €2.8 billion. Gross margins improved to 54% from 53.7%.

Earnings, meanwhile, moved higher by 28% YOY to €7.58 per share. This was higher than the consensus estimate of €6.80 per share, making this the second consecutive quarter of an earnings beat from the company.

For the full year, ASML again raised its guidance, with revenue expected to be between €43 billion and €45 billion. Full-year gross margin estimates were also raised to a range of 54% to 56%.

Net cash from operating activities rose to €1.7 billion in Q2 2026, from €747.7 million in Q2 2025. Overall, ASML ended the quarter with a cash balance of €6.7 billion, with no short-term debt on its books and a long-term debt balance at a much lower level of €1.9 billion.

However, despite the company's consistent showing in terms of results, ASML stock still trades at overvalued levels. Its forward price-to-earnings (P/E) ratio, price-to-sales (P/S) multiple, and price-to-cash flow (P/CF) multiple of 49.5 times, 19.3 times, and 59.3 times are all above the respective sector medians.

Extreme Strength Derived From EUV

Before this year, from about mid-2024 to mid-2025, ASML was having a hard time. ASML stock had dwindled, and earnings growth was relatively slower. What changed in 2026? Well, other than demand for memory chips skyrocketing, nothing else really. Demand for AI chips continues to be strong, and ASML continues to remain the only company making EUV machines.

Why are these machines so important to the point that ASML's customer base is populated with venerable AI industry names like Taiwan Semiconductor (TSM), Samsung, Intel (INTC), Micron (MU), SK Hynix (SKHYV), Kioxia (KXIAY), and many other semiconductor manufacturers? For companies that want to build leading-edge logic at 3 nanometers and below or the densest DRAM, there is essentially no alternative EUV machine maker. ASML holds a 100% share of the EUV market, and each machine can cost in the hundreds of millions of dollars, containing more than 100,000 parts that must work in concert at the most precise levels.

This is understandably hard to replicate. ASML spent decades and billions of dollars in research building both its machines and the ecosystem around them. An upstart would need to replicate not just the machines but ASML's entire web of specialist vendors, accumulated patents, and field experience.

Yet, ASML is not resting on its laurels. High NA EUV is shaping up as ASML's next big lever, and the machine behind it is the TWINSCAN EXE platform. The name refers to a higher numerical aperture, which in plain terms means the optics help resolve even finer features than standard EUV. That extra resolution lets chipmakers print smaller, denser patterns in a single exposure, which cuts steps, reduces defects, and improves yield on the most demanding layers. Each of these systems carries a price tag of around $380 million, well above the roughly $200 million of a standard EUV machine, so every unit sold lifts revenue meaningfully.

The proof that this technology is moving from lab to factory arrived in July 2026, when ASML confirmed that Intel had entered high-volume manufacturing on its 18A node using High NA EUV to pattern specific layers of its Panther Lake chips. That makes Intel the first company to high-volume manufacture logic with High NA, and it puts the technology's readiness beyond doubt.

A New China Headwind for ASML

China still represents about 20% of total sales and remains a sore point. In that regard, a new headwind related to China recently emerged for ASML.

In April 2026, a bipartisan group of U.S. lawmakers introduced the Multilateral Alignment of Technology Controls on Hardware Act, better known as the MATCH Act, which is qualitatively different from earlier restrictions. ASML has never shipped an advanced EUV machine to China, and the Netherlands has cooperated with controls since 2023, so the company's frontier tools were already off limits. What the MATCH Act would do, however, is close the remaining loophole by banning the export of deep ultraviolet (DUV) immersion systems. These machines are older workhorses that Chinese fabs buy to make less advanced chips.

That said, the bill is not law yet. The MATCH Act still needs to pass both chambers of Congress and receive a presidential signature, and it carries a 150-day window for countries like the Netherlands and Japan to tighten their own controls first.

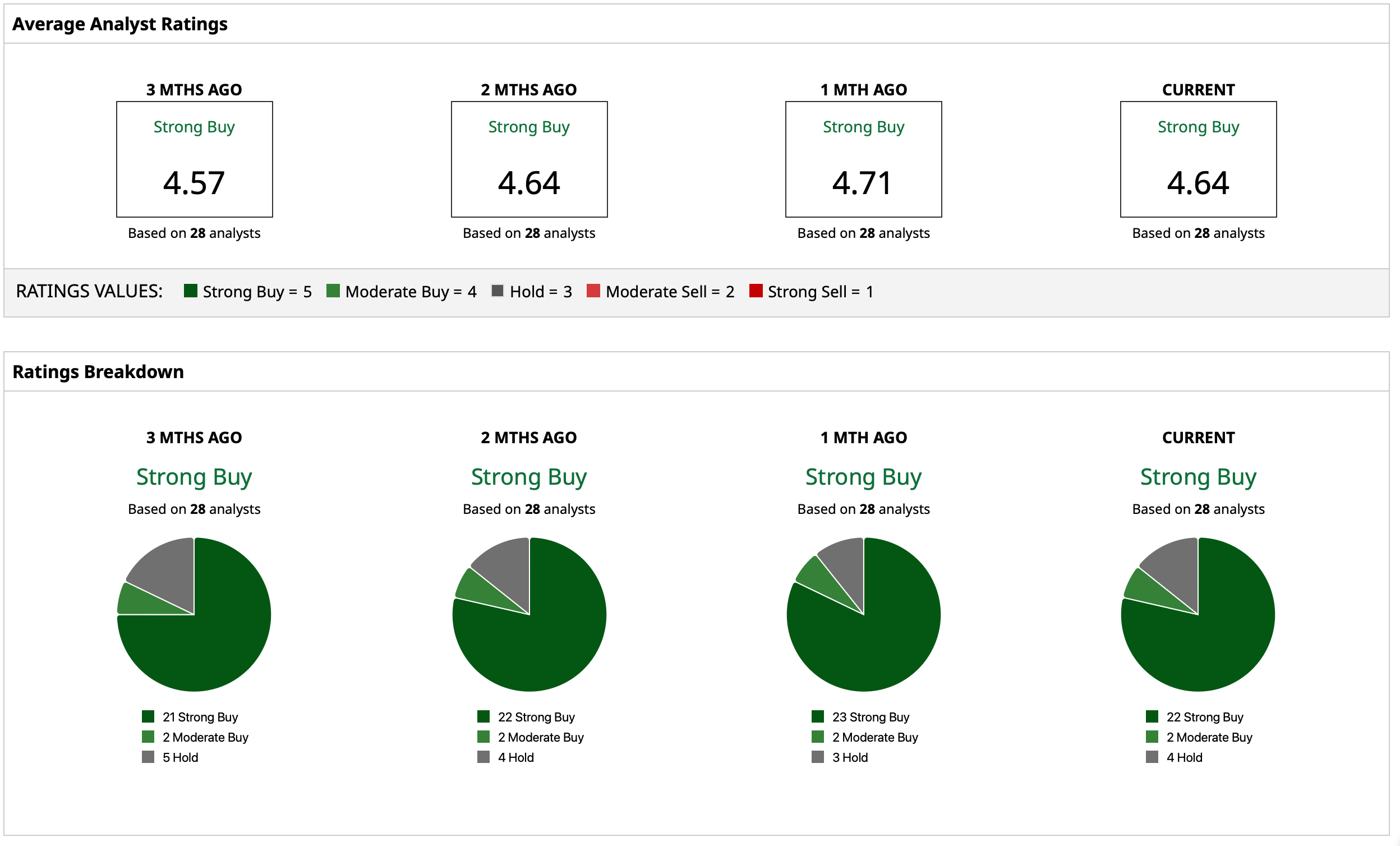

What Do Analysts Think of ASML Stock?

Overall, analysts give ASML stock a consensus “Strong Buy” rating with a mean target price of $2,102.57. This indicates potential upside of about 20% from current levels. Out of the 28 analysts covering the stock, 22 have a “Strong Buy” rating, two have a “Moderate Buy” rating, and four have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)