Data center M&A reached about $61 billion through 2025, beating the previous year as hyperscalers and big tech companies ramped up spending on AI infrastructure. The demand from these major players has been clear and consistent.

Industry forecasts now show AI infrastructure spending could climb to as much as $6.7 trillion by 2030, with nearly $3.1 trillion expected to go into AI chips and data centers. This is driving demand for materials, cooling systems, and components needed to run high-density data centers.

And that is the backdrop for 3M Company's (MMM) latest move. On July 15, 3M Company announced a strategic partnership with Microsoft Corporation (MSFT) to push deeper into AI data center infrastructure and broader enterprise transformation, using its materials science expertise. The market reacted right away, with MMM stock rising 2.5% to $160.51 the same day.

As 3M Company moves into the core of AI infrastructure, can this partnership drive a lasting re-rating for the stock?

A Closer Look at 3M Financials

3M is a broad industrial business that makes everything from safety equipment to electronics materials, healthcare products, and everyday consumer goods, with a model built on steady product innovation.

In the market, the stock has been fairly flat, up 2.44% over the past year and just 0.82% year-to-date (YTD).

It currently trades at a forward price-to-earnings of 17.91 times, below the sector average of 21.07 times, which suggests it is still valued at a discount compared to peers.

Income is still part of the story. 3M offers a 1.99% dividend yield, compared to the materials sector average of 2.82%, with a 35.12% payout ratio. The company pays $0.78 per quarter, with the most recent dividend issued on May 22, and it has now posted two straight years of dividend increases.

On the earnings side, Q1 2026 revenue came in at $6.03 billion, slightly ahead of expectations and up 4.3% year-over-year (YOY). Adjusted EPS was $2.14, beating the $1.98 estimate, showing solid cost control. Adjusted operating income was $1.40 billion, a bit below forecasts, but margins improved to 23.2% from 21.6% a year ago. Organic growth was softer at 1.2%, missing expectations, while free cash flow margin dropped to 5.8% from 8.5%, pointing to some pressure on cash flow. Even so, management kept full-year EPS guidance at $8.60.

New Infrastructure, New Growth Potential

3M Company is teaming up with Microsoft Corporation to dig further into AI data center infrastructure while also upgrading its own internal operations. The relationship brings together Microsoft’s Azure cloud scale with 3M’s strength in materials and manufacturing. A key part of the deal is Microsoft becoming the first major cloud provider to use 3M’s Expanded Beam Optical technology in its data centers, aimed at improving how fiber networks are built and managed.

Instead of traditional fiber connectors that need direct contact, this technology uses an expanded beam approach, making connections faster to install, easier to maintain, and less sensitive to dust and handling. That means fewer cleanings and inspections, while still keeping strong performance in busy data center environments. Early use has also shown it can speed up network deployment, which matters as demand for AI infrastructure keeps rising.

At the same time, 3M Company is using Microsoft’s tools to improve its own business processes. One example is “Ask 3M,” a new AI tool that helps customers find the right materials, compare options, and solve technical problems. It is built on verified data across 49 of 3M’s technology platforms and currently focuses on adhesives and tapes, with plans to expand into more product areas.

Wall Street’s View on MMM

3M Company is set to report earnings on July 21, before the market opens. Analysts expect $2.27 in EPS for the June quarter, up 5.09% from $2.16 a year ago. For the full year, estimates are at $8.74 compared to $8.06 last year, pointing to 8.44% growth and steady earnings progress.

Views on the stock are mixed but leaning positive. JPMorgan’s Chigusa Katoku kept a “Hold” rating but raised the price target to $178, suggesting about 24.6% upside at the time. The call is based on the idea that better cash flow, progress on restructuring, and rising demand tied to AI infrastructure, including the Microsoft Corporation partnership, could lead to more stable earnings and less pressure from past legal issues.

On the other hand, Bernstein started coverage with an “Underperform” rating and a $131 target. The firm flagged ongoing litigation risks, execution challenges, and a slow recovery in industrial demand as reasons the stock could lag if expectations around its AI exposure get ahead of reality.

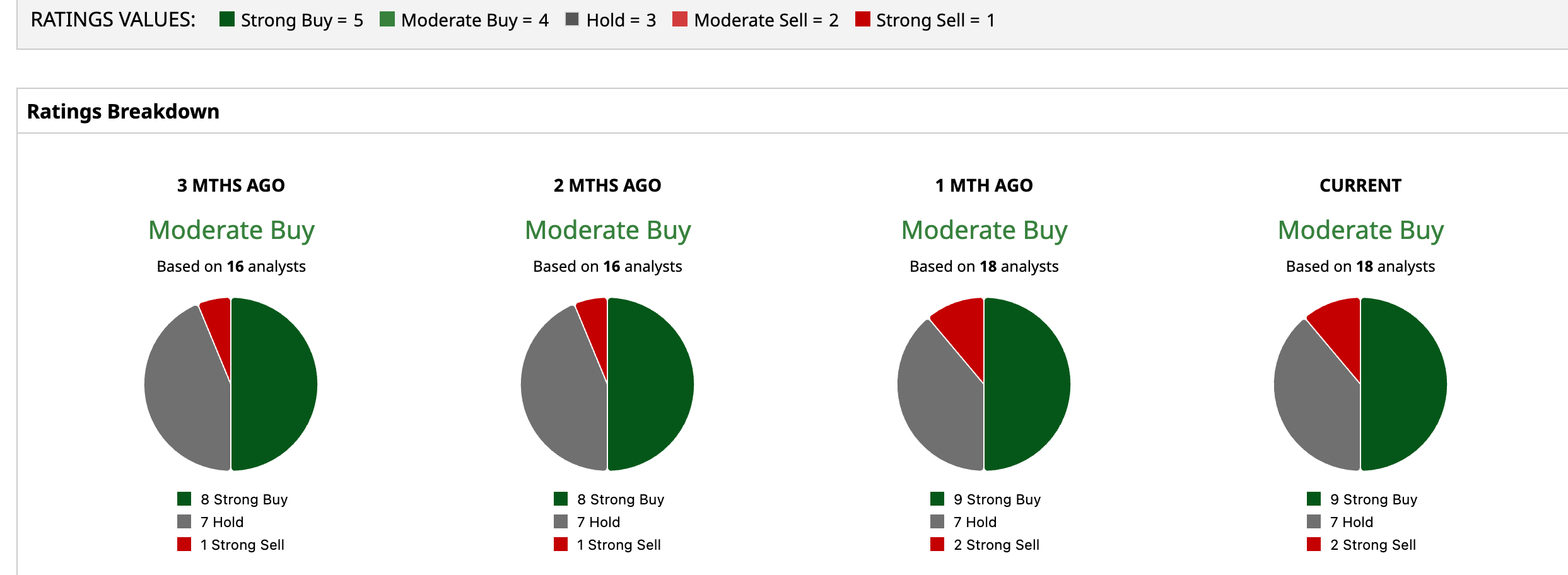

Still, the broader view remains constructive, with 18 analysts rating 3M Company a consensus “Moderate Buy” and an average price target of $174.44, implying 7.7% upside from current levels.

Conclusion

3M’s move into AI infrastructure through its Microsoft partnership looks like a credible step toward repositioning the company beyond its traditional industrial identity, but it is not a guaranteed rerating on its own. The setup here is gradual rather than explosive, with steady earnings growth, improving margins, and early traction in AI-linked demand supporting a more constructive outlook. Most likely, shares trend modestly higher from here rather than surge, as execution on restructuring, cash flow improvement, and real monetization of its AI exposure will ultimately determine the amount of upside investors are willing to price in.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)