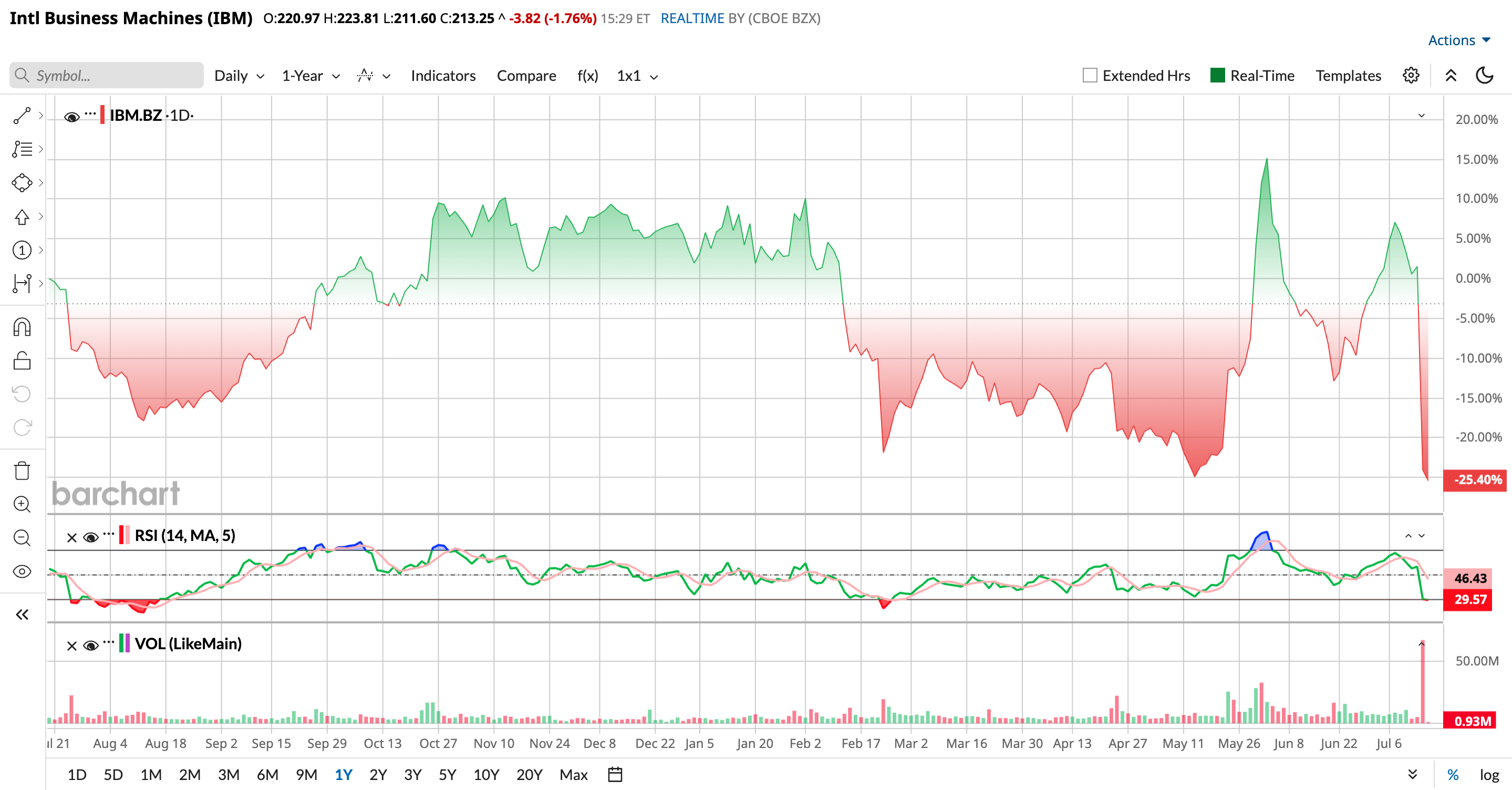

International Business Machines' (IBM) investors woke up to a nasty surprise on July 14. The technology giant released preliminary second-quarter results a week ahead of schedule, and the market's reaction was brutal. IBM shares plunged more than 25% and suffered their worst day since 1987 after the company reported missed expectations on both revenue and earnings while admitting it had failed to keep pace with changing customer spending patterns.

CEO Arvind Krishna acknowledged that IBM "faltered" as customers shifted more of their technology budgets toward AI servers, storage, and memory chips rather than traditional software and infrastructure projects.

The sell-off erased roughly $69 billion in market value in a single session. But after such a dramatic decline, is IBM finally a bargain, or does the weakness signal deeper problems?

IBM's Q2 Miss Raises New Questions

IBM has spent the past several years repositioning itself as an artificial intelligence and hybrid cloud company. While that strategy has produced steady growth in software, the latest quarter showed that execution remains a challenge.

Revenue increased just 1% year-over-year (YOY) to $17.2 billion, missing analysts' expectations. Adjusted EPS rose to $2.93, but it still fell short of Wall Street's forecast. Essentially, IBM missed estimates on both top and bottom lines, which explains the reason investors reacted so aggressively.

Looking deeper into the report, software revenue increased 5%, while consulting posted only modest growth. The biggest weakness came from the infrastructure segment, where revenue declined 7%, dragging overall results below expectations.

Krishna admitted that IBM failed to close several large customer contracts on schedule as enterprise clients redirected spending toward AI hardware ahead of expected price increases. Although IBM maintained healthy cash generation, the revenue miss overshadowed everything else.

IBM Is Still Investing for the Long Term

Despite the disappointing quarter, IBM isn't pulling back on long-term investments.

The company recently unveiled Project Lightwell, a $5 billion open-source cybersecurity initiative supported by roughly 20,000 engineers. Several major financial institutions, including Bank of America (BAC), JPMorgan Chase (JPM), Goldman Sachs (GS), and Visa (V), have already signed on as early participants.

In addition, IBM is moving aggressively into quantum computing. Management plans to invest more than $10 billion over the next five years to expand its quantum computing ecosystem and domestic chip manufacturing capabilities.

These initiatives won't repair quarterly results overnight, but they demonstrate that IBM continues to focus on technologies that could drive growth well beyond its traditional infrastructure business.

Does IBM Look Cheap After the Selloff?

A 25% decline naturally makes investors wonder whether IBM has become a bargain. The answer is a straightforward yes.

After the sharp drop, IBM trades at 22 times forward 2027 non-GAAP earnings, compared with a technology sector median of approximately 16.9 times.

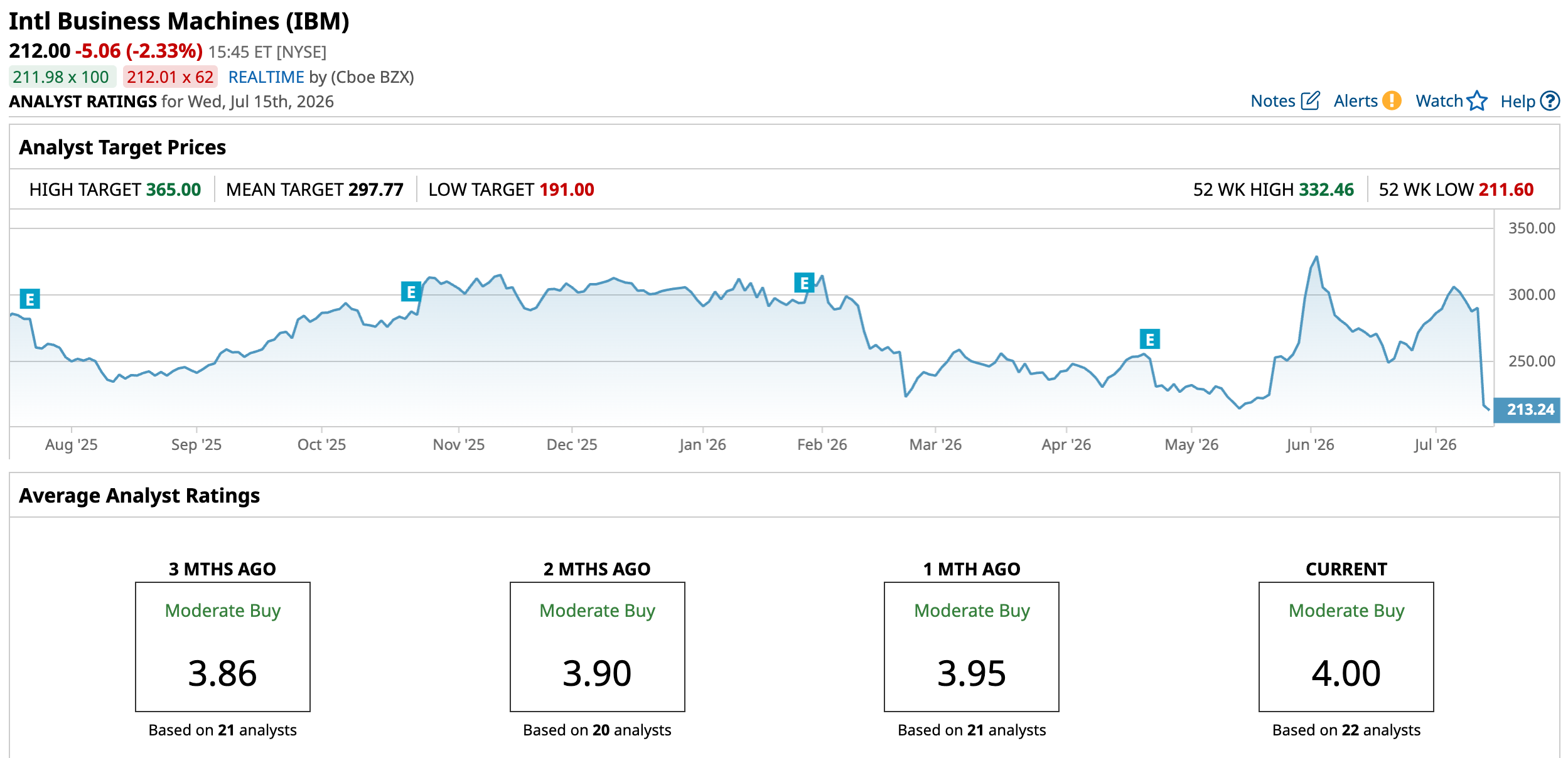

Earlier this year, optimism surrounding AI initiatives and quantum computing helped push the stock to a 52-week high of $332.46. Following the earnings warning, shares briefly traded near $214, wiping out nearly all of those gains.

What Are Analysts Saying About IBM Stock?

Wall Street remains divided on IBM's outlook. Oppenheimer continues to rate the stock “Outperform” with a $350 price target, while Evercore ISI also maintains an “Outperform” rating with a $310 target. Bank of America lowered its target from $330 to $280 but still recommends buying the shares.

Not everyone is optimistic. HSBC downgraded IBM to “Reduce” with a $191 price target, arguing that the company's premium valuation is difficult to justify given its slower growth profile. Susquehanna also maintains a more cautious “Neutral” stance.

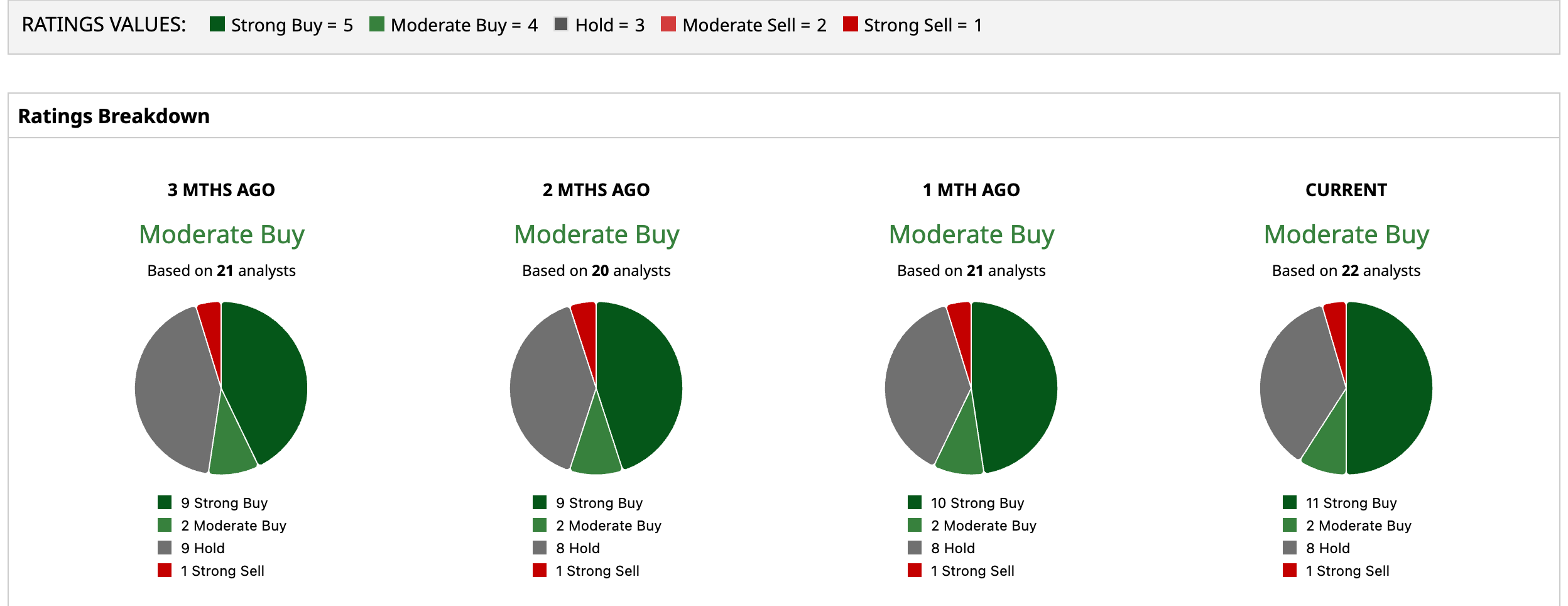

Overall, IBM still carries a “Moderate Buy” consensus among Wall Street analysts, with an average price target $297.77, suggesting meaningful upside of 40.5% if management can regain investor confidence.

Should You Buy IBM After the 25% Drop?

IBM's latest earnings warning was undeniably disappointing. The company acknowledged execution mistakes, and revealed that customer spending patterns shifted faster than management anticipated.

However, IBM also remains financially strong, continues generating billions in free cash flow, and is investing heavily in AI, cybersecurity, and quantum computing. Those businesses could become much more important over the next several years.

For long-term investors, the sell-off creates a more attractive entry point than existed just weeks ago.

The next few quarters will be critical. If IBM can prove the second-quarter weakness was temporary, and its AI strategy begins translating into stronger growth, today's decline could eventually look like an opportunity. However, if execution problems continue, the recent sell-off may not be over.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.