International Business Machines (IBM) just proved that the stock market is dangerous, and investors need a very specific type of strategy to play it.

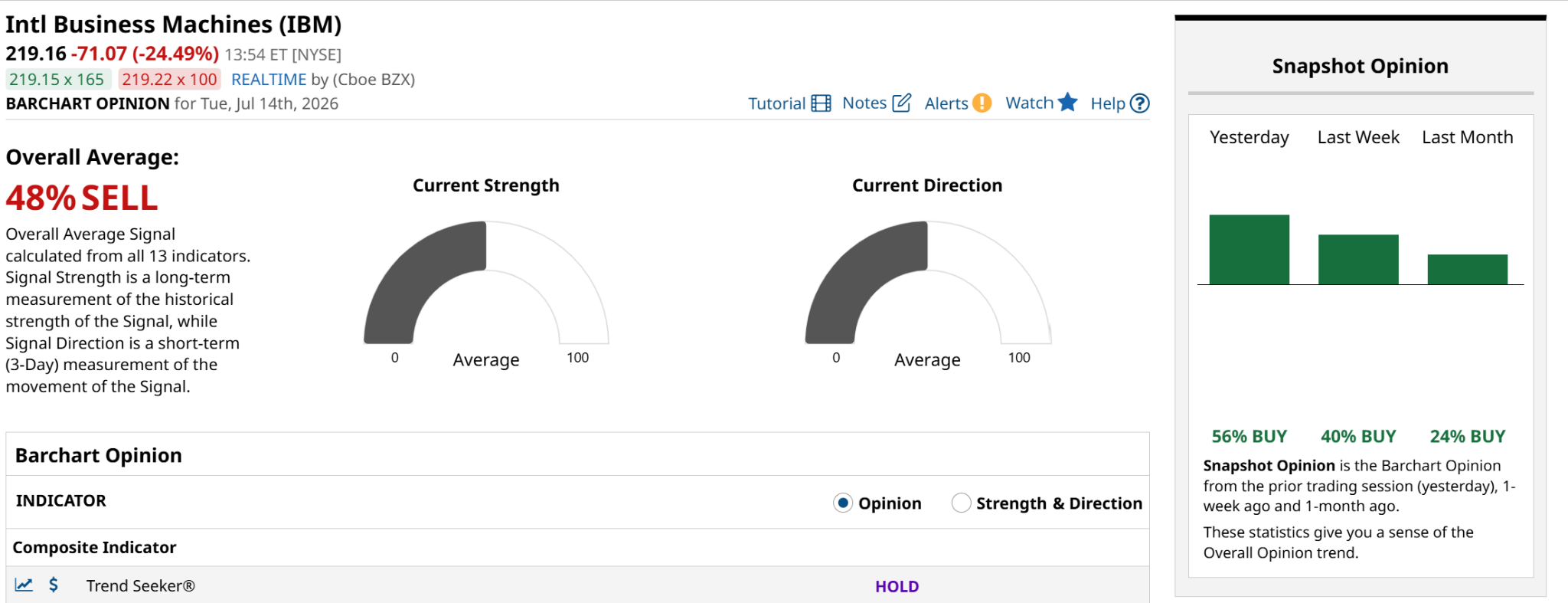

On Tuesday, IBM stock cratered by more than 23% in early trading, putting it on track for its worst single-day collapse since Black Monday in 1987. Barchart Opinion was at 56% BUY yesterday and headed in the right direction.

If I were taking a more optimistic look at IBM, I’d look at the chart above and conclude that things weren’t so bad… Tuesday’s price action wiped out “only” the last 21 months’ of stock price appreciation. The trigger was a weak preliminary second-quarter earnings report that dragged IBM back down to the $220 level, which is a potentially nice intermediate-term support level.

But this was a landmine, not a “technical correction.”

Below you see the chart from Tuesday’s disaster opening. I wrote in a single word in purple: This. What do I mean? That this is what a stop order does not do to protect you.

If the stock closes up there and opens the next day down there, your stop loss order only stops success. I have never been a fan of those for exactly that reason. Now a put option? THAT would have protected you. Whether you paid for it in part or whole with a corresponding covered call option (to complete an option collar) or not.

As I’ve said many times here, as a technician, I know that no market-valuation system, technical or fundamental, can accurately pinpoint a move like this. Sure, I can make a case that the stock’s chart was “stretched.” That alone would imply keeping position sizes on the light side.

The stock market is currently tradeable, but not investable.

That’s the biggest issue I have with this stock market. Not that it is un-tradable. But that is un-investable. That is, you can pop in and out, but do not expect SUSTAINED moves in stocks. And the bigger they rise, the harder they fall. In doing so, they ruin months or years of good investing.

Because “investing” is no longer what it was. Not with algorithmic trading and index funds dominating the landscape. The parade of leverage, options action, and inverse ETFs, all of which I use extensively in my own portfolio work, just adds fuel to the fire.

Again, I am not saying not to trade and invest. I’m more active than ever. But to me, there’s no way I’m putting serious capital at risk without at least a cheap “disaster hedge” in place. Smaller position sizes, convexity puts that are struck way out of the money, and inverse ETFs. Anything to “protect the house” is fair game to me now.

When a $272 billion enterprise titan drops nearly a quarter of its value in a single morning, it is a glaring warning sign that the plumbing underneath this AI-driven stock market is historically leaky. The reason IBM stock collapsed has everything to do with how the artificial intelligence boom is distorting corporate spending.

How to lose weight overnight (even if you’re a Dow Industrials stock)

In a letter to investors, IBM CEO Arvind Krishna explained that the company’s business software and infrastructure sales completely dried up in the final weeks of June. Why? Because IBM’s enterprise clients suddenly panicked about microchip shortages and price hikes. They aggressively redirected their tech budgets away from normal software and mainframe systems to secure expensive servers, data storage, and memory chips for their AI data centers.

IBM had anticipated some budget shifts, but the CEO admitted they completely underestimated the sheer magnitude of this capital expenditure stampede. This has exposed a harsh reality: AI is not creating a rising tide that lifts all boats. Instead, it is actively cannibalizing the rest of the technology sector. And, it is doing so despite a real-world possibility that the denouement of this era will be the opposite, where AI spend gone wild doesn’t deliver on ROI, to a level the market demands, and by when it expects it.

Corporate budgets are not infinite. To fund the endless purchase of hyper-expensive graphics cards and AI infrastructure, companies are starving their traditional software, consulting, and maintenance budgets. The very software and services that make up the backbone of the economy are being gutted to feed the AI beast. For their sake, I hope it works.

‘The Biggest Gamble in Wall Street History’

This massive budget cannibalization is exactly what prominent voices in the banking world are now calling “the biggest gamble in Wall Street history.” I plan to virtually staple that quote to my brain, and keep it on my internal mental wall until the S&P 500 Index, currently at around 7,500, is either at 10,000 or 5,000. My research leans about 2:1 to the latter being hit first.

Global technology giants and venture capital firms are projected to spend well over $1 trillion on AI infrastructure between now and 2029. Yet, the actual revenues being generated by generative AI software are a tiny fraction of that amount. The entire market is built on a circular loop of investments where tech companies buy hardware from each other, hoping that downstream corporate clients will eventually find a way to make it profitable.

IBM’s earnings warning is the first real proof that corporate customers are already tapped out. They are spending so much capital trying to build out physical AI infrastructure that they are actively failing to close normal business transactions elsewhere.

What’s the Takeaway?

Let this be a lesson to us all. This happened to IBM, but it can happen to any stock. At any time.

To me, that means smaller-than-normal position sizes, and hedging everything that is more than a “lottery ticket” in size. But above all else, manage risk. In the ways you already know, and in as many other forms as you can learn.

Rob Isbitts is a semi-retired CIO, former fiduciary investment advisor, and Barchart columnist. Check out his other work at ETFYourself.com (featuring the Fresh Charts weekly trading post), and ROAR.PiTrade.com, helping investors to better-manage their own portfolios.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)