/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

The artificial intelligence (AI) boom is reshaping corporate technology spending in unexpected ways. On Tuesday, July 14, International Business Machines Corporation (IBM) announced its preliminary Q2 FY2026 adjusted earnings of $2.93 per share on $17.2 billion in revenue, missing Wall Street estimates and sending its shares sharply lower.

The company revealed that the AI-driven memory shortage prompted enterprise customers to redirect a larger share of their technology budgets toward infrastructure, while higher cybersecurity spending weighed on its own results. These changing priorities contributed to IBM’s weaker-than-expected performance.

The shift immediately changed the market's mood. Investors interpreted IBM's comments as a positive signal for companies supplying the hardware behind AI, sending Dell Technologies (DELL) higher in early trading as analysts grew more constructive on infrastructure-focused names.

The enthusiasm was hardly surprising. Dell ranks among the world's largest server manufacturers, making it well positioned to benefit if businesses continue expanding their AI infrastructure. Its shares surged 7.1% on Tuesday following the announcement.

The single update has shifted the narrative across enterprise technology, leaving investors asking whether Dell could emerge as one of the biggest winners if hardware spending continues to outpace software budgets.

About Dell Stock

Headquartered in Round Rock, Texas, Dell has grown far beyond its personal computer roots into a company that powers modern enterprise technology. Its portfolio spans advanced servers, AI-ready data centers, enterprise storage, edge computing platforms, software, cybersecurity, cloud offerings, and managed services.

Dell's scale speaks for itself. The company commands a market cap of $296.5 billion, placing it among the biggest names in enterprise technology.

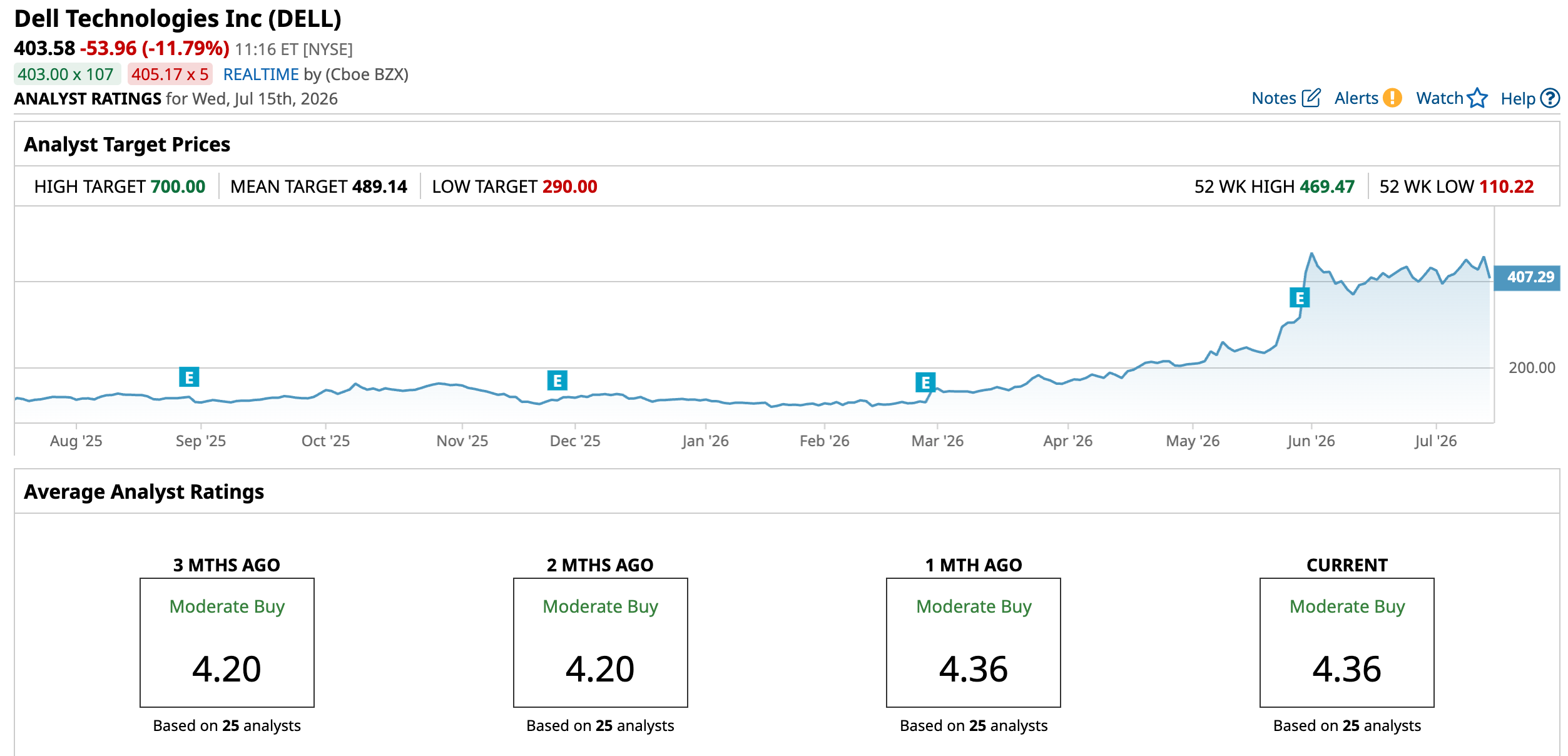

Investors have rewarded that growth story in spectacular fashion. The stock soared 219.4% over the past 52 weeks and gained 218.9% year-to-date (YTD). The stock climbed 126.4% over the past three months but has lost 1.87% over the past month.

The rally reached another milestone on Monday, June 1, when Dell touched a fresh 52-week high of $469.47. Strong optimism following the company's latest earnings release helped fuel that record run, reinforcing Wall Street's confidence in Dell's growing role at the center of the AI infrastructure buildout.

From a valuation perspective, Dell still looks reasonably priced despite its massive rally. The stock currently trades at 24.08 times forward adjusted earnings and 1.73 times sales. The figures sit below the broader industry average, offering an attractive entry point in the stock.

Additionally, Dell rewards shareholders with a steady stream of cash. The company pays an annual dividend of $2.52 per share, giving the stock a dividend yield of 0.59%. Dell is scheduled to distribute its latest quarterly dividend of $0.63 per share on July 31 to shareholders of record as of July 21.

Dell Surpasses Q1 Earnings

Dell's Q1 FY2027 results, released on May 28, gave investors plenty to cheer about. The stock rose 3.8% on the day of the announcement before surging another 32.8% in the following trading session as Wall Street welcomed a blockbuster quarter.

Revenue soared 87.5% year-over-year (YOY) to $43.8 billion, comfortably beating analysts' expectation of $36.1 billion. Adjusted EPS climbed even faster, jumping 213.5% to $4.86 from the prior year period, well ahead of Wall Street's estimate of $2.96.

Growth remained broad-based across the business. The Client Solutions Group, which includes desktop personal computers, laptops, monitors, and related products sold to consumers and businesses, generated $14.6 billion in revenue, marking a 16.8% increase from the previous year.

The Infrastructure Solutions Group, however, stole the spotlight. Revenue from the company's data center business skyrocketed 181.2% YOY to $29 billion. AI-optimized server sales proved to be the biggest growth engine, soaring 757.2% to $16.1 billion as enterprises accelerated investments in AI infrastructure.

Demand showed little sign of slowing. Dell secured $24.4 billion in AI orders during the quarter while recognizing $16.1 billion in AI server revenue. The company ended the quarter with a record AI backlog of $51.3 billion. Management said its sales pipeline remained several times larger than its existing backlog, even after converting $24.4 billion into orders.

Management delivered an upbeat outlook. For Q2 FY2027, Dell expects revenue between $44 billion and $45 billion, representing 49% growth at the midpoint of $44.5 billion. The company projects non-GAAP diluted EPS of $4.80 at the midpoint, reflecting 107% growth.

For the full FY2027, Dell expects revenue between $165 billion and $169 billion, implying 47% growth at the midpoint of $167 billion. And, management forecasts non-GAAP diluted EPS of $17.90 at the midpoint, representing a 74% increase from the prior year.

On the other hand, analysts expect Q2 FY2027 EPS to climb 120.5% YOY to $4.63. Full-year FY2027 earnings are projected to increase 91.8% to $17.74, followed by another 20.4% gain to $21.35 in FY2028.

What Do Analysts Expect for Dell Stock?

Wall Street's optimism continues to build around Dell. Evercore ISI analyst Amit Daryanani recently lifted his price target to $500 from $450 while maintaining an “Outperform” rating on the stock. The analyst expects Dell to remain a major beneficiary of the expanding AI infrastructure cycle as demand broadens across customers.

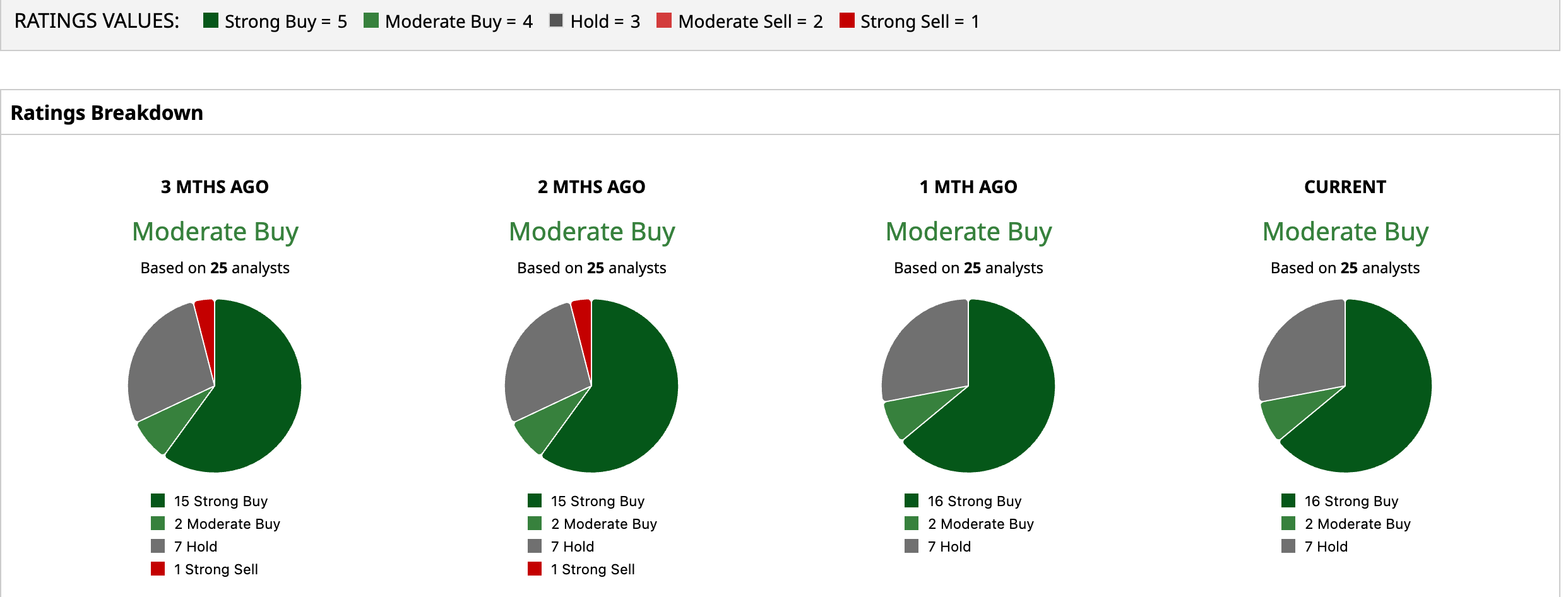

Analysts broadly share the constructive outlook. Wall Street currently gives Dell an overall “Moderate Buy” rating. Among 25 analysts covering the name, 16 recommend “Strong Buy,” two rate it “Moderate Buy,” while seven advise investors to “Hold.”

That optimism clearly shows up in price targets. The average target price of $489.14 implies an upside of 21.2% from current levels. Meanwhile, the Street-High target stands at $700, indicating a 73.5% gain.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)