While the US president continues to escalate his War on Iran over the Strait of Hormuz, Vlad in Invader is doing the same with Ukraine and the Strait of Kerch.

The latter turns the spotlight on the wheat sub-sector leading to a strong round of buying in global cash markets and futures overnight.

Corn and soybeans also rallied, though extended weather forecasts show a chance of rain across the US Midwest and Plains.

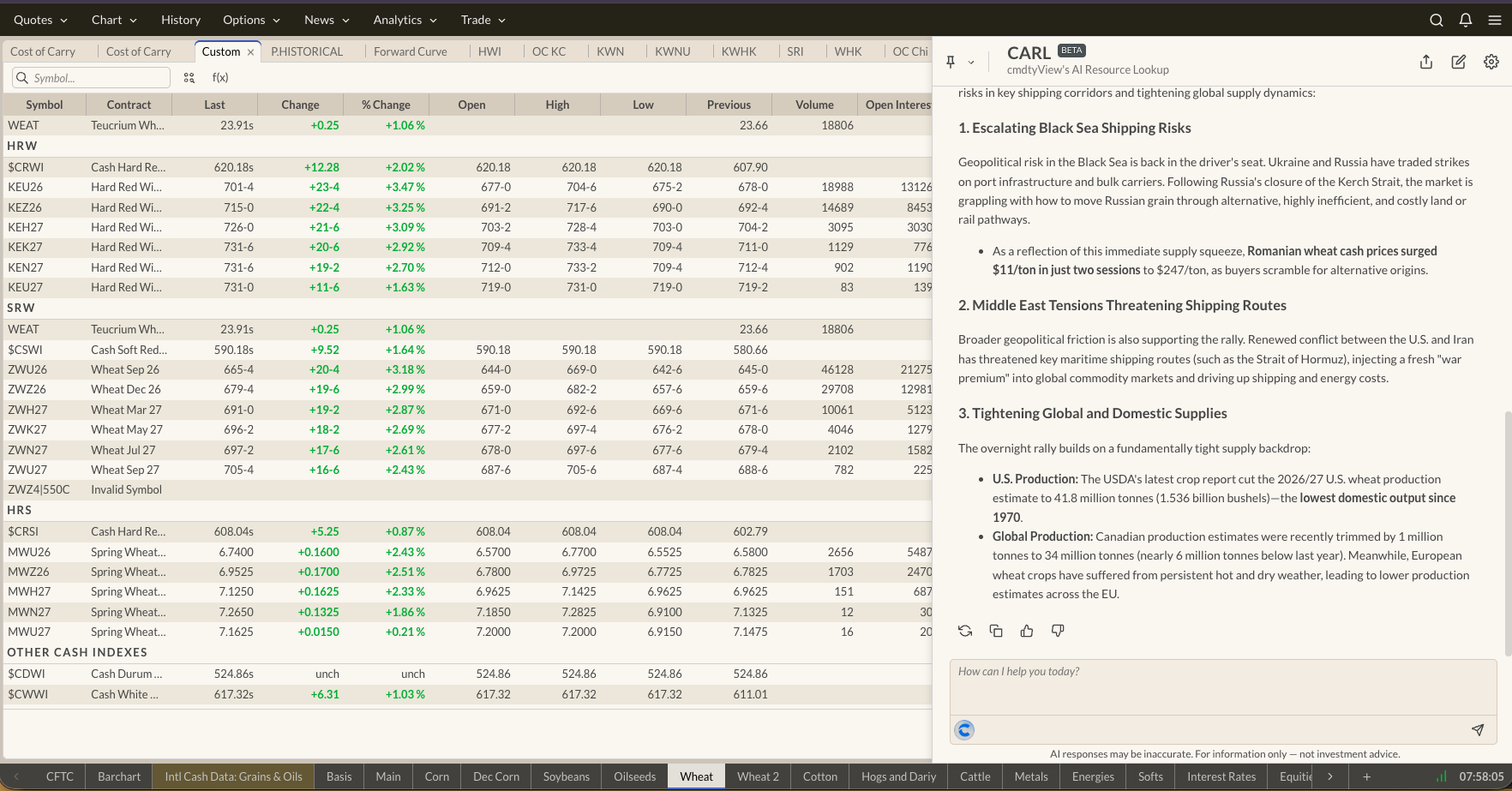

Morning Summary: There is a definite pattern that has developed over the past decade as dictators from around the world use the same playbook. A check of the quote screen early Wednesday morning shows me the Energies sector is rallying again as the US president continues to escalate the war he started over the Strait of Hormuz. However, it’s the wheat sub-sector that grabbed my attention as all three markets showed gains of 3.0% or more pre-dawn. A quick check of the news, and a question to Barchart’s AI analyst CARL, and I find out the catalyst for the rally the past two days is “Escalating Black Sea Shipping Risks”. It seems Vlad the Invader is still mired in the War he started against Ukraine more than four years ago. However, good ol’ Vlad closed the Kerch Strait meaning the market “is grappling with how to move Russian grain through alternative, highly inefficient, and costly land or rail pathways”. The third member of the trifecta, China’s President Xi, is likely facepalming is forehead with the antics of the others, reminding them again to do their homework and read Sun Tzu’s “The Art of War”. In other news, new Fed Chair Warsh has been told “inflation” is a 4-letter word that shall no longer be said. So much fun.

Wheat: I’ve moved the wheat sub-sector into the leadoff spot this morning given its strong overnight move on big trade volume. Recall the reversal winter markets showed during Tuesday’s session, a move that turned out to be more than typical Turnaround activity. Overnight through early pre-dawn Wednesday saw the September SRW (ZWU26) issue add as much as 24.0 cents (3.7%) on trade volume of 31,500 contracts and was sitting 22.5 cents higher at this writing. We can see there was solid commercial support to go along with rejuvenated noncommercial short-covering as the carry in the September-December futures spread had weakened by roughly 1.0 cent. I usually point out how we can’t read much into overnight spread trade, though this time around the clock December also registered solid trade volume of 20,000 contracts. Recall September closed yesterday’s session 9.75 cents in the green followed by the National SRW Index adding 9.5 cents last night. Yes, national average basis weakened fractionally but remains neutral in mid-July. Over in HRW we see the September issue (KEU26) up 26.5 cents, one tick off its session high and gaining 1.5 cents on December. Trade volume was showing 14,000 contracts and 11,000 contracts respectively.

Corn: The corn market was back in the green early Wednesday morning, likely on some spillover support from both the wheat and oilseed sub-sectors. The September issue (ZCU26) gained as much as 6.25 cents overnight while registering 20,000 contracts changing hands, fewer than September SRW, and was sitting 5.5 cents higher at this writing. Recall September finished Tuesday’s session 2.5 cents in the red with the National Corn Index coming in near $4.1025 last night, down roughly 2.75 cents for the day meaning national average basis weakened fractionally. We also need to keep in mind today is the first day of the new positioning week and September closed the previous Tuesday-to-Tuesday set with a loss of 5.25 cents indicating Watson decreased its net-long futures position once again. The new-crop December issue (ZCZ26) was up 5.0 cents pre-dawn after rallying as much as 6.5 cents overnight on trade volume of 33,000 contracts. Wednesday’s weather forecast calls for the US Central and Northern Plains to miss out on rain chances while it looks to be hit-or-miss across the Midwest. The latest 6-to-10-day forecast doesn’t offer much, with the Plains and Midwest expected to see “near normal” precipitation. However, the 8-to-14-day brings more moisture across the Plains.

Soybeans: The oilseed sub-sector was glowing green across the board at this writing. Recall distillates (diesel fuel) stayed strong Tuesday while soybean oil sold off. Early Wednesday morning shows the spot-month distillates contract (HOQ26) added as much as 6.3 cents (1.6%) overnight before backing off a bit. Meanwhile, the more heavily traded December soybean oil contract (ZLZ26) rallied as much as 0.58 cent (0.8%) on trade volume of 11,000 contracts and was holding within sight of its session high to start the day. The August soybean issue was up 4.5 cents after gaining as much as 7.5 cents while registering fewer than 5,000 contracts changing hands. Recall August closed 4.0 cents lower Tuesday with the November issue off 3.75 cents. The National Soybean Index came in last night 3.25 cents lower for the day meaning national average basis firmed against both contracts. Speaking of November (ZSX26), it rallied as much as 7.5 cents overnight and was sitting 6.0 cents higher to start the day. As with December corn, both commercial and noncommercial traders will be keeping an eye on short-term and longer-term weather forecasts, both for the US and Brazil. The March-May soybean futures spread covered a bullish 20% calculated full commercial carry at Tuesday’s settlement.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)