/IBM%20offices_%20Modern%20corporate%20building%20sign%20with%20a%20company%20logo%20By%20Nuria.jpeg)

Artificial intelligence spending continues to reshape corporate budgets at a pace few executives anticipated. Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOG) (GOOGL), and Meta Platforms (META) are committing hundreds of billions of dollars to AI infrastructure, while businesses across nearly every industry are racing to secure servers, networking equipment, storage, and high-bandwidth memory before supply tightens further.

That investment wave has fueled record demand for semiconductor companies, but money spent in one area often means money is unavailable elsewhere. IBM's (IBM) preliminary second-quarter results suggest investors may be seeing the first real evidence that AI's biggest winners are beginning to squeeze spending across the rest of enterprise technology.

IBM's AI Strategy Hit an Unexpected Roadblock

IBM spent the past year preparing for one of the most important product launches in its history. According to CEO Arvind Krishna's letter to investors, the company's new z17 mainframe is designed to bring artificial intelligence directly into mission-critical workloads, allowing banks, healthcare providers, insurers, and government agencies to run AI models on the same highly secure systems that process live operational data every day.

The strategy makes sense. Rather than forcing customers to move sensitive information into external AI platforms, IBM wants to bring AI to where the data already lives.

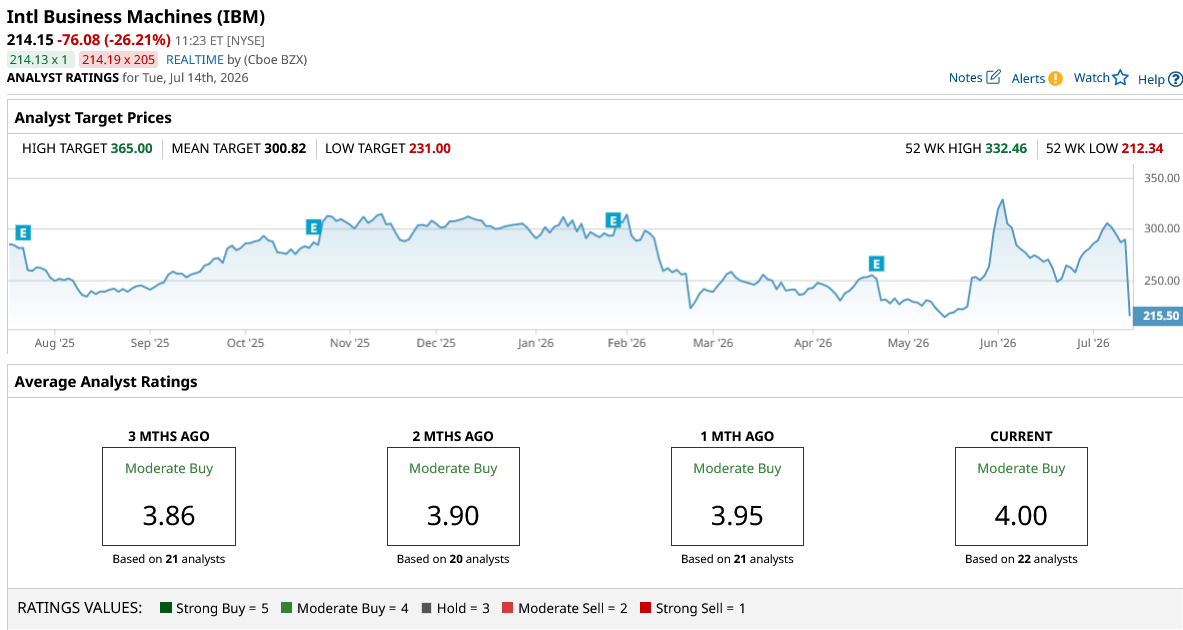

Management also warned investors that infrastructure revenue would soften ahead of the z17 rollout because customers typically delay purchases before a major hardware refresh. What management did not anticipate was the magnitude of the slowdown. IBM stock is plunging more than 25% this morning, and shares are down 26% year-to-date (YTD).

IBM's preliminary second-quarter results showed:

| Metric | Q2 Preliminary Result |

| Revenue Growth | 2% |

| Infrastructure Revenue | -7% |

| Gross Margin | Down 100 basis points |

| Adjusted EPS | $2.27 (-2%) |

The figures suggest the expected product-cycle slowdown became something much larger.

The AI Boom May Be Crowding Out Everyone Else

The companies buying IBM's enterprise systems are the same organizations scrambling to build AI infrastructure. Banks, healthcare providers, governments, and large corporations suddenly face enormous bills for AI servers, storage arrays, networking equipment, and increasingly scarce memory.

Those purchases cannot wait. Many components remain supply-constrained, particularly advanced servers and high-bandwidth memory used to power AI clusters. Higher prices mean a larger share of corporate capital expenditure budgets is devoted simply to securing available supply. The result is fewer dollars available for projects that might otherwise have moved forward.

Ironically, IBM is investing heavily in AI while some customers appear to be postponing purchases because AI spending elsewhere is consuming their budgets.

There were encouraging signs. Red Hat continued delivering steady growth, while IBM maintained investments in quantum computing, an area management believes will become another long-term competitive advantage. According to IBM's investor materials, software continues generating higher margins than infrastructure, helping cushion some of the weakness.

Still, those bright spots could not fully offset the pressure on hardware.

Why IBM Could Be the First Domino

Investors should resist viewing IBM's earnings as an isolated event. Many enterprise technology companies sell into the same customer base facing identical capital allocation decisions. If budgets are increasingly devoted to AI infrastructure, other vendors may also discover customers delaying software upgrades, consulting projects, storage purchases, or traditional data center investments.

That doesn't necessarily mean demand has disappeared. It may simply have shifted. IBM may therefore be serving as the canary in the coal mine rather than the exception.

Granted, every technology company has different exposure. Companies directly supplying AI infrastructure, such as Nvidia (NVDA), Broadcom (AVGO), Micron Technology (MU), and memory manufacturers, will likely continue to benefit from the spending surge. Conversely, companies selling adjacent enterprise products could encounter similar headwinds if customer budgets remain constrained.

Key Takeaway

In short, IBM's preliminary earnings report may be telling investors something much larger than how one company performed during the quarter. It may be revealing how AI is reshaping corporate spending priorities across the technology sector.

That said, IBM's long-term strategy remains intact. The z17 mainframe, Red Hat, and its quantum computing investments still position the company for future growth. But the numbers also suggest AI's infrastructure boom is absorbing capital that once flowed elsewhere.

Ultimately, as earnings season unfolds, smart investors should pay close attention to whether other enterprise technology companies report similar budget pressures. If IBM is the first domino rather than an outlier, the AI trade may become even more concentrated—rewarding infrastructure suppliers while leaving traditional enterprise vendors waiting for customer budgets to catch up.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)